What is the base rate?

How it affects mortgages, savings and more

Last year the UK base rate increased for just the second time in a DECADE - rising in August from 0.5% to 0.75%. While even this rate is historically low, it is important to understand what impact a further increase could have.

What does the base rate mean?

The base rate is the Bank of England's official borrowing rate, which influences what borrowers pay and savers earn. Its Monetary Policy Committee (MPC) meets eight times a year to decide what happens to the rate.

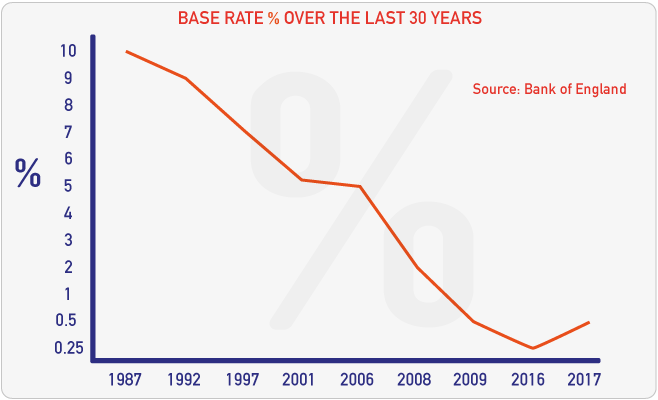

During the 2008 credit crunch the rate (which stood at 5%) was slashed substantially and has remained low ever since. As recently as August 2016 the rate languished at just 0.25%, but from that time it has risen twice - to 0.5% in November 2017 and then to 0.75% in August 2018.

While these latest increases may be relatively small – for now – the fact the Bank is willing to change it after such a long period of record low rates is almost more important than the margin of the change. And it will have had an immediate impact on households.

You may wonder why it would increase interest rates at all. Well, increasing interest rates discourages spending, and encourages saving, cooling the economy, which helps squash inflation.

It's worth bearing in mind too, these rises could be just the beginning – though industry commentators predict any further increases to be slow and gradual.

Here's a quick video explanation of the base rate...

What has the base rate historically been?

Recent interest rates have limboed way below historic norms. To put it in context, the last time rates went up – over 10 years ago, in July 2007 – they increased from 5.5% to 5.75%.

At this time the top easy-access savings account was paying about 6%, compared with today's measly 1.5%.

Meanwhile, those who had a mortgage in the high interest-rate period of the 1980s – where rates of 15% were possible – would argue that mortgage holders today have never had it so good.

In fact, financial service firm Hargreaves Lansdown estimates eight million Britons have never seen an interest rate rise in their adult lives.

Now, no one knows what's going to happen to interest rates in future, but if this is just the beginning and interest rates were to creep up closer to 5% again – even though nowhere near the historic highs of the past – this would have a massive impact on mortgage holders.

For example, this would affect those on a tracker rate mortgage, whose rate tracks, or follows, the base rate, and adds 1%.

Someone currently on a tracker on a £150,000 mortgage over 25 years would pay £617 a month and £185,218 for the full term.

However, if interest rates were to go up to 5% and the tracker was still base rate plus 1%, that same person would see their monthly payments soar to £943 and they'd have to stump up a whopping £282,994 over the mortgage term – nearly twice the amount.

I've got a mortgage – do I need to worry about the base rate?

The impact of interest rates on mortgages will depend on the type of mortgage you've got, the amount you've borrowed and how long you've taken it out for.

Fixed-rate mortgages

Good news if you've got a fixed-rate mortgage – which account for about half of mortgage products – as the name suggests, rates WON'T change during the fixed period.

A fix is normally for two or five years (but can be up to 10). And while you won't see any immediate change to your mortgage if you're on a fix now, the impact will come when the fix ends.

That's because the base rate rise (with the possibility of more to come) could mean the beginning of the end of very cheap mortgages. Before the announcement, new fixes were already a tad costlier in anticipation, meaning by the time you next come to fix, they could be even more expensive.

If you're on a fix you probably have the ability to overpay on your mortgage. If you have spare cash to do this, you could use the fact you've got a lower rate now to overpay, before you have to fix onto what could be a higher rate in future – but only do this if it's affordable for you.

If you're on a fix, that doesn't mean you should do nothing. Use our Ditch your fix? tool to check if you can save by switching from a pricey fix, or if you're near the end of yours, if it's worth leaving early (though watch out for hefty early redemption fees).

Variable – including anyone on a lender's standard variable rate – and tracker mortgages

If you're on a variable or tracker mortgage – where what you pay is linked to the base rate – rate rises mean your mortgage becoming more expensive. The latest 0.25% rise means roughly £200 a year more per £100,000 of outstanding mortgage.

When your fixed-rate deal comes to an end, if you don't remortgage onto another deal it reverts to your lender's standard variable rate (SVR). Around two million people are estimated to be on their lender's SVR.

Normally an SVR is a much higher rate than you could get if you remortgaged (although in the current low interest-rate environment, SVR rates have been pretty low). The rises in the base rate do not automatically mean a rise in the SVR as it does with a variable or tracker; the lender can alter it at its discretion, but invariably the rise will get passed onto borrowers eventually.

If you're on a variable rate or tracker, your lender should get in touch to let you know how much the rate rise will affect your monthly repayments.

I'm a saver – is a change in the base rate good or bad for me?

In contrast to mortgage holders, a base rate rise is a positive for savers. Low interest rates have punished savers over recent years, especially older people who'd worked and saved hard and planned to live off the interest.

While some banks have passed on the benefits to savers, not all have and there's no certainty that they will in the event of future base rate rises. However, even though a modest rise may not make a huge difference, it's still a step in the right direction.

Fixed-rate savings

Just like with fixed-rate mortgages, with fixed-rate savings (often referred to as bonds), you fix into a rate for a set period of time, for one, two, three or even five years. Normally you're offered a slightly higher rate for fixing than you would with an easy-access rate product, with the longest fix paying the most.

So if you're already in a fixed-rate savings account you'll need to wait until your fix ends until you can benefit from the interest rate rise on any potential new products.

If fixing again, take into consideration that if interest rates were to continue rising, it might be wise not to fix for too long so you can keep taking advantage of higher rates.

Easy-access savings

With easy-access savings products, where you can withdraw the cash whenever you want, interest rates are variable, meaning lenders could pass on a rise in the form of better rates. This depends on the bank though, and unless you have a savings account that tracks the base rate, an increase isn't guaranteed.

Anyone with savings should check now what rate they get, as it could be they're on a bad deal. Less than 1%? It's a rip-off – move it. Full info, including top current account saving rates, can be found in our Top Savings guide.

Does the base rate affect credit card and loan rates?

If you've got an existing credit card or loan, unfortunately you're in the same boat as mortgage holders – an interest rate rise isn't a positive for you.

Loans

If you've got an existing loan, it's almost certainly a fixed rate, meaning you're not impacted by any base rate rise.

Though if you're hoping to get a loan, rates are very likely to rise from current all-time lows, because of the interest rate rise, and due to pressure on lenders to reduce the UK's personal borrowing. See the Bank of England's warning MSE News story for more.

To find your cheapest loan, use our Top Loans Quick Eligibility Calculator and it'll tell you which you've the best chance of getting, without hitting your creditworthiness.

Credit cards

Of course, with credit card APRs already often over 18%, the latest 0.25% increase won't make much odds. Yet after years of ever-better 'best-ever' 0% deals, things are now moving the other way.

The Bank of England has warned about irresponsible lending and the rate rise will add to that mood music. As above, see the Bank of England warning news story for more.

Two years ago you could shift debt to a balance transfer card with a 0% period lasting up to 43 months. Now it's just 28 months, so if you're paying interest, sort it ASAP, as it's possible deals will continue to get worse.

Use our Balance Transfer 0% Eligibility Calculator which shows which 0% deal you're most likely to get.

This is a general explainer about what the base rate is. For specifics on what the rise to 0.75% means for you, we've published a full briefing on how it affects your mortgage, savings, cards etc, plus we've a separate story on How banks are updating their mortgage and savings rates.

Share this guide?