How to stop spending

The MoneySavingExpert.com Demotivator

Sometimes waving a magic MoneySaving wand and changing all your providers isn’t enough to really improve your finances. Two simple words are needed... STOP SPENDING. Whether you need scaring into it, or tips on cutting back, this guide and the frightening Demotivator tool will help tackle those spending demons.

Do you spend more than you earn?

There’s no need to stop spending for the sake of it. If you enjoy a cappuccino, can afford it, aren’t in debt and aren’t overpaying, sip away.

Yet as Mr Micawber says in David Copperfield:

Annual income £20, annual expenditure £19.96, result happiness.

Annual income £20, annual expenditure £20.06, result misery.

There are two ways to check if you’re spending more than you earn.

The BIG danger signal. Are you in debt?

If you are, and can’t answer the question 'what are your debts from?' there’s a problem. If you didn’t buy, for example, a car or a conservatory, but you've used cards or loans to fill gaps, an ear-piercing alarm should ring.

Debt is fine if it is planned, rational, budgeted for and as cheap as possible. But if you consistently need to use the credit cards to supplement your monthly spend, you have a problem. Do that, and it can have life-destroying consequences.

No debt problems are unsolvable. It might not be easy or quick to resolve, but there's always a route. The earlier you tackle them, the easier they are to deal with. Our free debt advice guide talks you through where to start.

If you're struggling with debt and mental health problems, we also have a free mental health and debt booklet to help.

Do a budget to work out where you're WASTING cash

If you are spending more than you earn, there’s a simple way to accurately check. The specially designed Budget Planner calculates your genuine annual income and then tells you exactly how much more you spend than you earn.

Most people are shocked by the result, as many of those who think they’re within budget month-by-month aren’t when it’s done over a year. This is the start point of sorting out your cash. If possible, sit down and spend the time to do the budget. The planner also then helps you prioritise your spending.

Of course, even if you’re not spending more than you earn, if your aim is to save up for something specific, the techniques below will help too.

25 quick tips to help you stop spending

For the real top tricks to cut back, you need to ask those who live it. The Debt-free wannabe section of the MSE Forum is a community that works together to clear often-heavy debts at speed.

We asked regulars on there – many are the kings and queens of personal budgeting – for their top tips in the Great "Self-Discipline" Hunt. Here are some of the best...

-

Check if you're leaking money via unused subscriptions & payments

Many have costly subscriptions for gyms, streaming services, magazines, packaged bank accounts and more, yet rarely or never use them – or with time and home moves, forget about them altogether.

First, check for regular payments going out of your bank account for services you no longer use – then CANCEL them. You may even be able to get a refund. See how to do it in Cancel direct debits.

-

Then take it up a notch and ask yourself if you REALLY need it

Even if you DO occasionally use that pricey gym/Spotify/Netflix subscription, if you're overspending right now, it may be a luxury you can't afford. Look for cheap alternatives – see Free gym passes, Free music streaming and TV MoneySaving tricks.

-

Block notifications and emails from shops, takeaway services and more

Ever been tempted to get a takeaway after an offer pops up on your phone? The best way to avoid temptation is to block notifications from delivery services and retailers – you can do this on your phone by going to 'Settings'.

It's also worth unsubscribing from marketing emails, if you find yourself tempted by sales and discounts. It's worth noting this may mean you miss out on the odd exclusive discount code for a planned purchase. An alternative is to set up a separate email account, just for marketing emails... provided you have the self-control to avoid scrolling through these until you need them.

-

Stop spending so much on food – plan, plan, plan

Set a budget, write a food plan and take a calculator with you when you go food shopping. And never go when hungry – it's too tempting to overbuy. By going just once a month you’ll be less likely to buy on impulse and for convenience. Top up with milk and bread in between (also see the Supermarket shopping tips guide).

-

Leave debit/credit cards at home

Only take the cash you absolutely need with you and don't have a cash card with you to take extra out of the hole in the wall. That way, however tempted you are, you have to walk away in the end.

-

Work out what it costs in work time

If you’re tempted by an impulse buy, work out how long it would take you to earn that money in hours worked.

So if you get paid £10 an hour and it costs £150, that’s an extra 20 hours you’ll need to work to fund it, taking into account tax (our Demotivator will do this for you).

-

Focus on your debt/savings

Work out how much longer it will take you to pay off your debt or increase your savings if you give in. To put it into perspective, if you’re saving for a holiday, think "that costs one day in Miami"...

-

Sleep on it

If you really want something, sleep on it for a night. You may find it doesn’t seem as attractive the next day.

-

Avoid temptation – don’t go shopping

If you don’t go to the shops, you can’t be lured by nice things. Stay at home – simple as that. Of course, you may also need to stay off your phone, laptop or computer so you aren't tempted to shop online. If you like to while away your leisure time by going shopping, do something else instead. Keep busy and you won’t be tempted to get out your wallet.

-

For every new thing you buy, try to get rid of an old thing

If you really want to buy something new, see if you can sell something you don’t use any more to cover the cost.

Check out our guides to eBay selling, Facebook selling and Vinted selling for tips. There's also Flog your rubbish for cash and Nine ways to sell clothes.

-

Make a list and stick to it

Always make a shopping list before you go to the stores and see tempting goodies. Then once you’re out – don’t stray from it.

-

Try online grocery shopping

If you can’t stick to a shopping list, try ordering your shopping online. It’s easier to stick to a budget as you get a running total, plus you won’t be tempted by the sights and sounds in the shop (see the Cheap online shopping guide).

-

Keep a list of your debts/savings targets in your wallet

Every time you open your wallet for a potential purchase you’ll be reminded of why you shouldn’t be spending money.

-

Get free sofas, coffee machines, baby clothes & more on Freecycle/Freegle

If you really need to replace something, try giveaway sites Freecycle and Freegle, or take up offers of hand-me-downs from friends and family.

-

Challenge yourself

Make it a challenge to come up with creative nights out or in on a budget. It could be a picnic in the park or a movie night at home. Or if there’s something particular you want to buy, see how quickly you can raise the funds through extra means.

-

Take a packed lunch to work – keeps you out of harm's way

It’s an old one but a good one. Making a packed lunch doesn’t just stop you being tempted by expensive sandwich shops, it also keeps you from the pub or easy trips out with friends where money flows out.

-

Start a new hobby

Spend time on a new (free) activity like running or do some volunteer work. This leaves less time for spending. We also have a guide of free ways you can learn something new, such as a language, Open University courses, history through virtual museum tours and more.

-

Create magical holiday memories with the kids for FREE

You don't need to shell out a load of cash to give your kids the perfect summer hols or Christmas experience. We have plenty of tips and tricks to help you create magical family memories for free (or very cheap):

-

Pay yourself pocket money

Set up another account for bills and use this to make sure all your bills are paid. With the money left over you can pay yourself a set amount which is yours to spend as you like.

-

Stash your shrapnel to save

Stick loose change in a savings jar. You’ll be less likely to break a note to spend and once the change has built up, pay it into your account or off a credit card (see the MSE Forum £2 savers club).

-

Keep a debt diary

Write a note of when you’re likely to overspend. If you can identify trends that lead to overspending you might be able to prevent them or vent in some other way.

-

Think of your credit card as a debt card

Remember until you pay it off, you're spending the bank’s money not yours. Think of it as a debt card and you might not be so hasty reaching for your wallet.

Also ensure the debt is as cheap as possible – see our Credit cards and Loans guides for full help.

-

Make your own at home

Whatever your vice is, whether it’s pizza, beer or frothy cappuccinos, try making it at home for a fraction of the cost.

-

Take the 'No-Spend Day' challenge

Once or twice a week have a day where you spend nothing other than budgeted-for things. Quite often just spending once can break the cycle for the rest of the day.

For inspiration, check out MSE Molly's blog I challenged myself to spend NOTHING for 15 days – here's what happened.

-

Stop wasting food

Are you always throwing out food that’s gone off? It's been claimed that storing food correctly could save shoppers £1 billion a year by prolonging the lifespan of food and stopping edible items being thrown out. So if you're prone to emptying your fridge into the bin, see our 12 ways to STOP wasting food and drink.

How to stick within your means

One of the big problems is asking the wrong questions. People often ask Martin something like:

How do I get the shiny new car / glamorous holiday / amazing Christmas / designer clothes I want on my paltry salary?

It's thinking this way that leads people to constantly overspend, because you're totally ignoring the financial reality. Instead the real question is:

On my paltry salary, what’s the best lifestyle I can possibly have?

You have to start letting your finances rule your lifestyle, not vice-versa.

Be clinical when assessing yourself

Sit down for a brutally frank financial self-assessment. We don’t mean a quick budget looking at just one month’s expenditure. That omits the cost of Christmas, birthdays, summer holidays, MOT tests and more.

We mean scrutinise EVERYTHING, big and small, over a year, to prioritise what’s important and cutting anything that pushes your spending beyond your income. Use the free Budget Planner tool to do it for you. But be warned, it’s the real deal, so set aside two hours and prepare for a sinking feeling when pressing the “Do I spend more than I earn?” button.

Once you know what you've got and what you can spend it on, then you need to find a way to stick to it. An easy way to do this is to use the Piggybanking technique which uses different bank accounts to control your cash flow (if you're in severe debt, also see the the Problem Debts article).

Work out your priorities

If you haven't got enough income to pay for everything you want to, then you've got to work out what's most important to you.

First should come all necessary bills, rent, mortgage, food and clothing, but after that there's wriggle-room for making your own spending decisions.

The Demotivator – frightening but fun

The Demotivator is a special fun tool designed to complement the full Budget Planner that shows you the real impact of discretionary spending.

Simply enter items such as cigarettes, daily sandwiches, or newspapers and it’ll tell you how much you spend a year, and how long you worked to buy them. Then print out the results and stick it to your wall or fridge as a constant demotivating reminder.

Here's an example from someone who buys a daily £3 coffee, and has an annual salary of £25,000:

Easy ways to cut back

There are two ways to cut your expenditure:

Pain-free saving

This means being a better consumer and getting better deals on everything you do. It’s what this site’s all about. Use the Money Makeover article to see all the areas where you can save.

If you’re asking why it’s called ‘pain-free’ – the answer's simple – these changes shouldn’t impact your lifestyle. So maximise the pain-free savings and then re-budget to see if you still need the next step.

Painful saving

After all the pain-free saving, the next step is to curtail your lifestyle, and stop spending on the things you commonly spend on. It’s all about self-discipline. Small changes on things you do regularly, for example cutting from two takeaways a week to one, can save you £250 a year.

Again, to help, we asked forum users to suggest their ideas in the Great Ways to Cut Back Hunt – below are some of their suggestions.

Entertainment and lifestyle

Cancel unused digital/satellite television channels See TV MoneySaving tricks for ways to watch for free.

If you buy a magazine every month, take out a subscription

It is cheaper and many magazines offer a free gift.

Organise nights in with your friends and family

Avoid expensive taxi journeys home from town, just get them to bring a bottle.

Try camping or house swapping with friends

take a break from the norm for a different type of holiday.

See if your local catering college has a restaurant attached

Good food at cheap prices.

Health and beauty

Try for student night haircuts at top salons

The students are supervised by a fully trained hairdresser.

Visit your local beauty college for cut price treatments

Most of the students will be coming to the end of their training and need to be examined.

Quit smoking

For tips and help, see the NHS's stop smoking services.

Use a sponge or buff puff in the shower

To reduce the amount of shower gel required.

Don’t buy shaving foam/cream for your legs

Hair conditioner works just as well and softens up the skin too.

Food and home

Use your phone's calendar (or a real one) to record when bills need to be paid

And when library books need to be returned etc.

Grow your own veg

You don’t need a garden, you can grow lettuce in a window box or potatoes in a old dustbin.

Bake your own bread

You don’t need a bread maker, you can do it by hand.

Start a compost heap

Any food scraps can be added to fertilize flowers or your home grown veg.

Brew your own beer

Read How to start homebrewing?

If you hire any equipment then do it over a bank holiday

You usually get an extra day's hire for free.

Car boot or eBay unwanted possessions

Makes you money and declutters your house. Read the eBay selling guide.

Use white vinegar instead of numerous cleaning products

It works and it’s cheap.

Only use half a dishwasher tablet per wash

If you are just cleaning glasses and lightly soiled dinner plates, you don’t need a whole tablet.

Keep old perfume bottles in your underwear drawer

The drawer will always smell fresh without using liners.

Buy cheap cola to flush down the toilet

It’ll keep it sparkling clean, and works just as well as the expensive toilet cleaners.

Retain your mobile phone box and instruction manual

You can often get money back or sell as second hand.

Saving energy

Don’t leave electrical goods on standby

It's estimated that a typical UK household could save £50 - £90 per year on electricity bills if they always fully switched home appliances off rather than leaving them on standby.

Turn it all off when you go on holiday

There is no reason to have them on, and if you are away for two weeks or more that’s a lot of money being spent.

Turn off lights when you are not in the room

Simple but will save you money on your electricity bill.

Go to bed 30 minutes earlier than usual

Get more rest AND save on electricity.

Don’t have the heating on and a window open

Just turn the heating down if it gets too warm in the house.

Turn your central heating thermostat down by one degree

You’re unlikely to notice the difference in the heat, but you will notice the difference in the bill.

Use a water saving device if you have a water meter

You can use a water filled coke bottle instead of an expensive purpose made device.

Use a shelf in your airing cupboard to dry clothes

Rather than putting the heating on.

Use rechargeable batteries

A one-off cost.

If the oven is on, use it well

Cook multiple meals/cakes and freeze them.

Invest in a slowcooker

It’s MoneySaving and timesaving all rolled into one.

When making tea or coffee, don't overfill the kettle

Or you can buy kettles that only heat the required amount of water.

Keep your fridge/freezer free of ice

It works more economically and holds more.

Shopping

Visit the supermarket late at night

This is when they have more reduced items on offer.

Never go shopping when you are hungry

You only end up buying overpriced junk food. Read the Supermarket shopping guide.

Never take your children to the supermarket with you

"I want" doesn’t save you money.

Use free/open source software on your PC

It’s usually just as good as the costly equivalents. See what's available in the Free office software guide

Buy remanufactured ink cartridges rather than new

They work out sometimes at nearly half the price of new branded cartridges.

Don’t buy gifts

Give vouchers for your time or be arty and make something. Read the Festive Fivers guide for ideas.

Organise a clothes-swapping party with your friends

One person’s trash is another treasure.

Use money-off coupons, online and offline

Save the money in a piggybank, don’t spend it. See the latest updated Supermarket coupons

Ensure your current tax code is correct

You could be paying more than necessary.

Use a council MOT test centre

They’ve no vested interest in prescribing repairs for your car so it’s more likely to pass. Read the Cheap MOTs guide.

Walk/cycle instead of taking the car on shorter journeys

Saves you money on petrol and keeps you fit.

Start a car share scheme at work

It’s MoneySaving and environmentally friendly.

Need scaring into this?

Martin met a family for a money makeover. First, they admitted shame at £60,000 credit-card debt, a sum that mathematically would take them two years of after-tax income to repay even if they’d no bills to pay or food to buy.

Yet what they initially hid from Martin, and themselves, was that a further jaw-dropping £120,000 of their mortgage had originally been splurged on plastic then shifted onto the home loan.

That’s £180,000 overspending in less than a decade, yet these weren’t obviously profligate folk. They’d simply stumbled into the trap of wrongly believing they were wealthy and tried to give their family the best. Solving such gargantuan financial indiscipline just takes two simple words....

STOP SPENDING

That’s easy to say and a nightmare to do. To get back on track, they needed to vow not to lay out for anything barring food, heat and essential bills. For most, that's unnecessary, but get it wrong and things can get that bad.

Surely it's only a little debt?

Putting a little debt on cards may not seem too bad, yet if it's unplanned and not budgeted for, it's simply willy-nilly overspending, and you’re setting yourself up for a disaster, and not just financially. Debt crisis can impact homes, family, mental health and relationships.

You may feel this is over-dramatising. Yet when there’s no money left, you can’t borrow more, and the creditors are asking for money back which you’ve no ability to repay, it touches every element of your life.

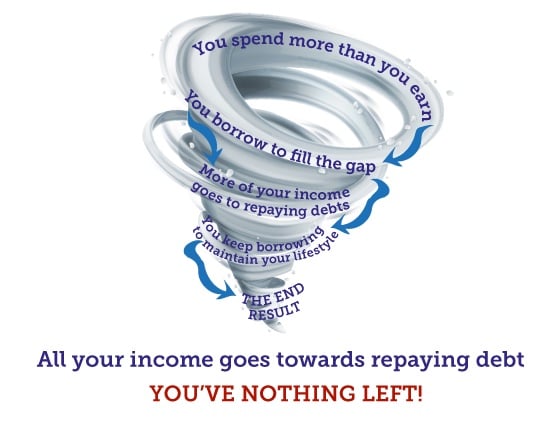

The danger is what’s called a ‘debt spiral’. It works like this:

Use Martin's Money Mantras

Whether you're skint or not skint, there are a couple of questions to ask yourself before you buy anything, as Martin explains in this short video...

As a reminder, print out a free Money Mantra Card similar to the image below and pop it into your purse, wallet or phone case so you see it before you spend.

Perhaps the most difficult question to self-assess is 'will I use it?' which examines what economists call 'opportunity cost' – in other words, could you get better use or pleasure out of the same cash buying something else? So is a stunning £300 dress that’ll be used once worth it, if the same money could buy other items used more often?

A story from Martin...

My favourite example of this is shopping with a friend, who hates me telling this story. She’d spotted two pairs of leather boots and was deliberating between them. I checked prices – one £40, the other £110 – yet she was only concerned with preferred style.

So I whipped £70 cash out and held it up with the £40 pair to show the real decision was one pair of boots plus the cash, or just the rival boots alone. She paused and with genuine interest said 'wow, I’ve never thought of it like that before'.

Five mins later she bought the more expensive boots anyway – you can’t win ‘em all!

Share this guide?