Credit card rewards

Earn cashback, points & more

Spend on one of these cards and it pays you – either in pure cashback or points that convert into vouchers for shops, airlines, hotels and more. If you're debt-free and pay off your card every month, you can earn goodies worth £100s each year. Plus our Reward Credit Card Eligibility Calculator will show cards you've the best odds of getting.

First, a quick overview of reward credit and debit cards...

Reward credit and debit cards allow you to earn cashback, points or vouchers for your everyday spending. If you're debt-free and pay off your card IN FULL each month, these cards can help you earn £100's worth of rewards each year.

Don't just apply – go via an eligibility calc. Our Reward Credit Card Eligibility Checker speedily shows acceptance odds for top cards (some are 'pre-approved'), without affecting your creditworthiness.

Choose the right rewards for your spending habits. Whether you prefer cashback, points, or vouchers, pick a card that aligns with your lifestyle and spending patterns.

Always pay off your balance IN FULL every month. To maximise rewards and avoid interest, always clear your balance on time.

Credit Card | Main rewards & key info |

|---|---|

Lloyds Ultra (1) | 1% cashback for a year (0.25% after) |

Amex Everyday | 5% cashback for 5 months (max £125) |

Amex Gold | Intro points worth £115 at Amazon, M&S etc |

These are our top few cards – see our full review for more options. Links go via our eligibility calculator.

(1) Lloyds Ultra is only available direct, the link takes you to its site where you can check your eligibility before applying.

If you do get a card, ALWAYS follow these Reward Credit Card rules:

a) Set up a Direct Debit to repay credit cards IN FULL each month

b) Only use the card for all NORMAL spending to max rewards

c) Don't borrow or withdraw cash on these credit cards

Now we've given you a brief overview and you understand the basics, let's take you through reward credit and debit cards in more detail...

How do reward credit & debit cards work?

Reward cards are simple in principle: do your everyday spending on the card, and in return, you earn cashback or reward points, which can usually be turned into vouchers or money off at various shops. Done right, reward cards can net you £100s in bonuses or cashback.

It sounds great – everyone loves something for nothing. But get it wrong and it's nothing for something: interest wipes out rewards if you don’t repay in full every month.

Some credit cards also impose a minimum spend to unlock rewards – so always read the terms before applying.

What types of reward cards are there?

Most reward cards are credit cards, though a few debit cards also offer rewards. It’s important to understand the difference in protection: credit cards give Section 75 protection, which makes the card provider jointly liable with the retailer if something goes wrong with purchases over £100. Debit cards have the lesser chargeback protection, which can help you reclaim money in some cases.

Main types of reward cards:

-

Cashback credit cards. Earn a percentage back on spending, usually credited monthly or annually. Some pay a flat rate, others vary by retailer or category. Earnings are often capped

-

Points credit cards. Collect points for each pound spent, which you can redeem for vouchers, perks, or goods and services.

-

Supermarket and department store cards. These work on similar principles, but their points usually only have value with the retailer’s own loyalty scheme. Examples include supermarket reward schemes or big retail brands offering store vouchers, for example Tesco Clubcard or John Lewis vouchers.

-

Travel and air miles cards. Offer perks for frequent flyers such as free flights, upgrades and hotel discounts – see our best air miles credit cards guide.

Are reward credit cards worth it?

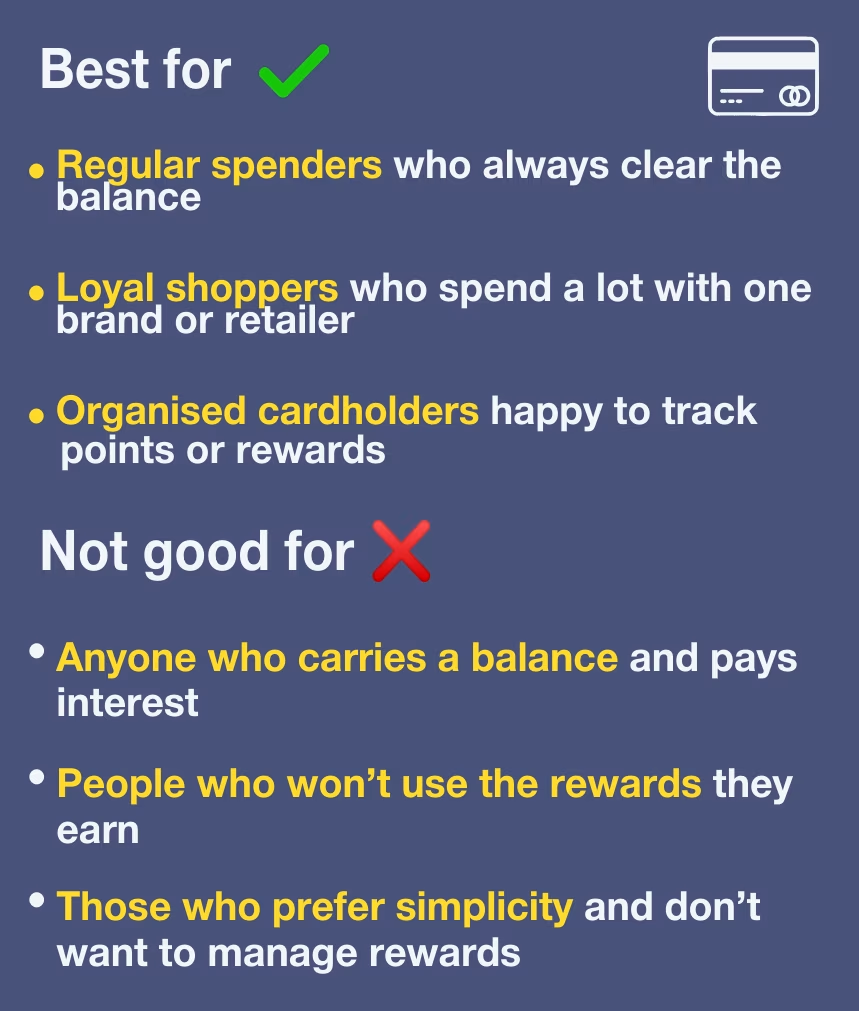

For the right person – yes. If you always repay the balance in full every month and only use the card for spending you’d do anyway, rewards can effectively be a free bonus.

However, if you carry a balance, overspend chasing points or pay fees you can’t offset, those rewards will quickly be wiped out by interest and charges. In those cases, a 0% spending credit card is usually a far better option.

Six golden rules to actually make reward cards pay

Get it wrong and you could be out of pocket. Follow these six rules to make reward cards work for you – and once you’ve got the basics right, see our top reward credit cards below.

1. Set up a direct debit to repay IN FULL every month

Getting charged interest almost always scuppers even the best reward schemes. Set up a Direct Debit to repay the card IN FULL each month, so interest doesn’t wipe out the gain.

Do that and you’ve effectively turned your credit card into a debit card that pays you every time you spend.

No ‘repay in full’ option when setting up the DD? Call the lender to get it sorted.

If you can't always repay in full, don’t get a reward card – go for a 0% interest-free spending credit card instead.

2. Use it for ALL normal spending – don’t overspend

Use it for everyday spending – food, bills, travel – to max rewards, replacing cash and debit cards. But never spend more just to earn points; overspend and you wipe out the gain.

Got work expenses you reclaim? That can be a powerful way to earn rewards at no cost – if it's allowed.

3. Extra cardholders can boost rewards – but the debt's yours

Adding someone else can boost your points, but there’s no such thing as a joint credit card. It's your card and all spending is your responsibility.

4. Check rewards suit you and what they’re REALLY worth

Some schemes look generous, but payouts are tiny.

-

Cashback: simplest – earn a set % for every £1 you spend (for example, 1%). But watch the small print: cashback’s usually paid annually as statement credit, and some cards have a minimum spend.

-

Reward schemes: earn points for perks such as days out, flights, holidays and more – but always check what a point is really worth. Often 0.5p to 1p.

5. Don’t apply if you’ve big borrowing coming

All credit card applications have a small short-term negative impact on your ability to get credit. So if a mortgage or big loan’s on the horizon, weigh up if getting a reward card is worth it right now (see Credit score boosting).

Got debts? Cut interest before chasing points – that’s usually worth far more. See Best balance transfers for the top credit card debt-cutting cards and Debt problems for full step-by-step help.

6. Never withdraw cash or borrow on these cards

These cards are for paying like a debit card and clearing in full. Borrow or take cash and interest + fees whack away the gain.

Cashback vs points: which is best?

Reward cards fall into two camps: cashback cards and points cards. Cashback is usually best for most, as it’s simple and predictable, but points cards can deliver bigger perks for frequent travellers. We've our top reward card picks below, but first, here’s how to decide which type is right for you:

Choose a cashback credit card if you want...

-

Simplicity: easy to manage and redeem, unlike points cards which need more tracking.

-

Predictable value: cashback is usually paid at a fixed rate – for example, 1% on all spending.

-

Lower or no fees: many cashback cards have no annual fee (though some high-return options charge one).

Best for: those who want straightforward, reliable rewards with minimal effort.

Choose a points credit card if you want...

-

Potentially higher-value rewards: points can deliver more than cashback if used smartly, such as converting to vouchers worth £100s.

-

Travel perks: with some schemes – for example, Avios – points can be used for flights, hotels, car hire and more.

-

Big welcome bonuses and perks: such as airport lounge passes, statement credits or bonus points.

Important: Points need managing. They can expire, be devalued, and vary in worth depending on how you use them.

Best for: frequent travellers, those loyal to certain airlines or hotels, or anyone willing to put in the effort to maximise rewards.

Top reward credit & debit cards

The top reward cards are often dominated by American Express because of its strong intro bonuses and high ongoing rewards. However, our current top pick is from Lloyds, and we also include other cards where flexibility or no fees make them a better choice than Amex for many.

Remember, American Express isn’t as widely accepted as Mastercard or Visa, and you won’t get the intro bonuses listed if you’ve had a personal (not business) Amex card within the past two years.

Top reward credit and debit cards – what we'd go for

All of our top pick credit cards offer cashback or points for everyday spending. The key point is that to benefit from the cashback, you'll need to pay them off IN FULL each month or the interest will outstrip the gain. The Amex intro bonuses are only available to new cardholders who haven't had an Amex personal card in the last two years.

Top for everyday and overseas spending. Lloyds Ultra is great if you prefer cashback to points – the card pays 1% for a year on most purchases worldwide with no cap on how much you can earn and no fees for overseas spending (though don't use this as an excuse to overspend). The cashback is paid in Jan each year and after 12 months the cashback rate reverts to an ongoing 0.25%.

You can only apply for this card direct with Lloyds (it's not in our eligibility calculator), though you can check your likelihood of acceptance on Lloyds' site before you apply without impacting your credit file.

Top Amex cashback pick. Amex's Cashback Everyday currently gives 5% cashback on most purchases for the first five months (max £125). The cashback's paid after a year, provided you spend £3,000+ a year on it. After the five months, it's a decent 0.5% cashback on spending up to £10,000 a year and 1% above. Overall, it's a strong option for bigger spenders.

Top for 'free cash' & perks. Amex's Preferred Rewards Gold gives you 20,000 bonus intro points if you spend £3,000+ within three months. The total points you'll have when you hit the spending trigger are worth £115 in vouchers for Amazon, M&S, Sainsbury's & more. Other ongoing perks include one Amex point per £1 spent (worth 0.5p), extra cashback with Deliveroo and airport lounge access.

The card is free in the first year, but from year two there's a hefty £195/year fee, so diarise to cancel if you don't want to pay.

Easy FREE £40 Uber vouchers with Santander Rewards.

Santander newbies opening its fee-free Santander Rewards credit card can get £40 in Uber Eats/rides. Just add it to your digital wallet and spend on the (physical or virtual) card 10+ times in month one. You're then sent a £20 voucher within 60 days and another 30 days after claiming the first, as long as you've kept the card open. Pay it off in full each month and you're £40 up. The card also comes with a year's 3% cashback on petrol, diesel, train travel, EV charging (not at home), eating out & takeaways (0.25% on other normal spending). After a year, it's 0.25% on most normal spending.

Lloyds Ultra

No fee

14.9% rep APR

Top for everyday and overseas spending. Pays 1% cashback for first year on spending in the UK and overseas (0.25% after). Unlike with most other cards, the cashback isn't capped and is paid each Jan. It’s also available to both new and existing Lloyds customers. You can only apply for this card direct with Lloyds (it's not in our eligibility calculator), though you can check your likelihood of acceptance on Lloyds' site before you apply without impacting your credit file.

Ongoing rewards:

1% cashback in first year on worldwide spending (0.25% after)

Other perks:

Fee-free for overseas spending & ATM withdrawals (if you pay off IN FULL each month)

Amex Cashback Everyday

No fee

29.1% rep APR

Top Amex cashback card. This card gives 5% cashback, usually only for purchases in the first three months (max £100), but right now it's boosted this to five months (max £125). The cashback's paid after a year, provided you spend £3,000+ a year on it. You won't be eligible if you've had an American Express card in the last two years.

Ongoing rewards:

0.5% cashback on first £10,000 spend, 1% above

Amex Preferred Rewards Gold

Free for first year, £195/yr after

29.1% annual interest

Top for 'free cash' & perks. Open this card and spend £3,000+ in the first three months and you'll get a boosted 23,000 points, worth £115 in vouchers for Amazon, M&S, Sainsbury's & more. You won't be eligible if you've had an American Express card in the last two years.

Ongoing rewards:

One Amex point per £1 spent (worth 0.5p)

Other perks:

2 x £5 cashback on Deliveroo orders a month & 4 airport lounge passes

Next-best credit & debit reward cards

We've more choice below if none of the above suit. We've ranked by ongoing cashback, but if you've a short-term high-spend period, many of the cards have initial cashback boosts, which could make them winners for you. And some of the cards have fees, so do keep an eye out.

Unlimited 3% cashback on travel costs for a year & £40 Uber vouchers – a top card for commuters. Includes petrol, diesel, EV charging (not at home), trains, buses and taxis. You also get 3% on dining out and takeaways, plus 0.25% on most other normal spending. After a year it's 0.25% on everything (with the usual exclusions, like gambling).

There are no fees or interest on overseas spending – provided you repay IN FULL each month – and Santander says the 3% cashback applies overseas too, though we're unsure how well it'll be tracked (so you may get 0.25% instead). Don't use the card at cash machines (you'll be charged hefty fees & interest).

Plus if you're a Santander newbie (ie, you don't have ANY of its products, including a current account, savings account or mortgage) you also get two sets of £20 Uber vouchers, which can be used on Uber Rides and Uber Eats (including groceries but excluding alcohol).

To get the bonus vouchers, within the first 30 days, activate the card, add it to your digital wallet (eg, Apple Pay, Google Pay) and spend on the physical or virtual card 10+ times. Keep the card open and you’ll get an email with the first £20 voucher within your first 60 days (you must then claim it within 60 days).

You’ll then automatically receive a second £20 voucher 30 days after you claim the first one (provided you continue to keep the card open). You must use the vouchers within three months of adding them to your Uber account.

Ongoing rewards:

3% cashback worldwide on most travel, fuel and dining in/out purchases for 1yr (0.25% after)

Other perks:

Ongoing 0.25% cashback on all other puchases

Amex Cashback

£25/yr fee

29.1% annual interest

Strong cashback, particularly for bigger spenders. Pays the joint-top intro cashback at 5% for the first three months (max £125) with no min spend required, plus decent cashback after. If you won't spend £10,000+ each year, the Amex Everyday card above works out better, as it has no annual fee.

Ongoing rewards:

5% cashback for 3mths (after it's 0.75% cashback on first £10,000/yr spend, 1.25% above)

Amazon Barclaycard

No fee

28.9% rep APR

Good for Amazon shoppers. Decent cashback on Amazon purchases, plus a £20 Amazon voucher if accepted, and an extra £10 voucher when you activate the card in the Barclays/Barclaycard app. You can only apply for this card direct with Amazon (it's not in our eligibility calculator), though you can check your likelihood of acceptance on Amazon's site before you apply without impacting your credit file.

Ongoing rewards:

1% cashback at Amazon, 0.5% elsewhere for 1yr (Prime members get a boosted 2% on 'shopping day' events, eg Prime Day)

Other perks:

£30 of Amazon vouchers

Barclaycard Rewards

No fee

28.9% rep APR

Strong overseas card with decent, but beatable, cashback. Pays 0.25% cashback on spending in the UK and overseas, and unlike with most other cards, the cashback isn't capped.

Ongoing rewards:

0.25% cashback on worldwide spending

Other perks:

Fee-free & interest-free overseas spending & ATM withdrawals (if you pay off IN FULL each month)

MBNA Cashback

No fee

12.9% rep APR

Cashback guaranteed for three years. In the first three years it pays 0.25% cashback on spending in the UK and overseas, and unlike with most other cards, the cashback isn't capped. There's no cashback after the three years is up and the overseas spending moves from being fee-free to a charge of 2.95%.

Ongoing rewards:

0.25% cashback for 3yrs on worldwide spending

Other perks:

Fee-free for overseas spending (if you pay off IN FULL each month)

Chase

No fee

Easy to get & decent cashback. Pays 2% cashback on most UK supermarket, transport & dining spending (max £20/mth). From July you need to spend 15+ times a month on the card and have £1,000+ in Chase savings accounts to qualify. Only requires a soft credit check to open, so it's easier to get than the credit cards above.

Ongoing rewards:

2% cashback on most UK supermarket, transport & fuel spending (max £20/mth)

Other perks:

Fee-free for overseas spending & ATM withdrawals (& linked 4.5% easy-access savings account)

How to boost your rewards

Once you’ve nailed the basics (repay in full and use it for normal spending), here’s how to maximise what you earn…

-

Add an extra cardholder (carefully). Some providers let you add an additional cardholder, meaning their spending earns rewards too. This can quickly boost your points or cashback – but remember, it’s your debt, not theirs. You’re responsible for the full balance every month.

-

Stack rewards where possible. You can often 'double dip' by combining your reward card with other savings tools such as cashback sites, retail loyalty schemes and card‑specific shop offers. Done right, this can seriously increase the value you get from the same purchase – without extra spending.

-

Use rewards quickly and deliberately. Points and vouchers aren’t always stable. Schemes can devalue rewards, change redemption rates and expire unused points. So, once you’ve earned a meaningful amount, use it rather than hoarding – especially for airline or hotel rewards.

-

Track your real reward rate. Work out how much you’re genuinely making in rewards against any fees or interest. If you’re only earning a few pounds a year, a simpler, fee‑free cashback card could be better value.

-

Use reclaimable work expenses. If your employer allows, putting work expenses on a reward card can be a powerful way to rack up points or cashback at no personal cost – as long as you’re reimbursed and repay in full.

Hidden reward card costs and pitfalls to watch for

Reward cards can be lucrative – but only if you use them right. Watch out for these common pitfalls...

Late or missed payments wipe out rewards fast. Reward cards often have higher interest rates than standard credit cards, as lenders expect you to repay in full to earn rewards.

If you carry a balance even briefly, the interest can easily beat what you earn in points or cashback. For example, £10 to £15 of rewards in a month means nothing if you’re hit with £20+ in interest.

Even one late or missed payment can mean losing promotional rates, account restrictions, and damage to your credit file. That’s a heavy price for chasing a few pounds in perks – so only get a reward card if you’re sure you can pay on time.Annual fees can wipe out your rewards. Some of the highest-paying reward cards charge annual fees – only worth it if you earn more in rewards than the fee costs.

If you spend lightly or use the card occasionally, you could pay more than you get backSpending extra just for rewards can cost you. Many cards tempt you to splash out to hit thresholds or unlock bonuses. If that means buying what you wouldn’t normally get, the “reward” could just be a discount on unnecessary spending – or no saving at all.

Points can expire or lose value. Points and vouchers don’t last forever. Depending on the scheme, points may expire if you don’t use the card regularly, reward values can be cut with little notice and some airline or hotel points devalue over time. So don’t hoard points “for later” – it’s risky.

Some reward cards aren't accepted everywhere. American Express cards often offer higher rewards, but aren’t accepted everywhere. If many of your regular shops don’t take Amex, your real-world return could be far lower than it looks.

Overseas use can be expensive. Using a reward card abroad can trigger non‑sterling fees (typically around 3%), plus likely charges for cash withdrawals. These can wipe out the perk, so always check before you travel.

Minimum spend targets aren’t always easy. Some sign-up bonuses or boosted earn rates require you to hit a spending target within a set period. Miss it and you get no bonus – but you still keep the card and any fees.

Cashback sites may pay you for signing up

As an extra boon, members of specialist cashback websites can be paid when they sign up to some financial products. Do check that it's exactly the same deal though, as terms can be different. And remember the cashback is never 100% guaranteed until it's in your account.

For full help to take advantage of this and the pros and cons, see our Top cashback sites guide.

Other MSE credit card guides... 0% balance transfers | What is a balance transfer credit card? | 0% credit card for spending | 0% money transfer cards | All-rounder 0% cards | Travel credit cards | Air miles credit cards | How does a credit card work | Full credit cards section | Student credit cards | How to pay off credit card debt more quickly | Prepaid cards

Reward cards FAQs

Do I get Section 75 protection on these cards?

Yes. Credit cards come with Section 75 protection – if you buy something costing between £100 and £30,000 and something goes wrong (for instance, the retailer goes bust), the card firm is jointly liable. Debit and prepaid cards don’t have this.

Note: only the main cardholder’s purchases are covered, and paying via PayPal usually cancels this protection. Read the full guide to using PayPal to pay on a credit card.

How do card companies make money if I always repay?

Credit card providers don't make money from interest alone. Every time you pay by card, the retailer pays a small fee to the card company – this often funds cashback. Amex charges retailers more than Visa or Mastercard, which is why some shops don’t accept it.

How many reward cards can I have?

As many as you're accepted for – there's no limit. Though of course, every credit card application has a small impact on your credit score. So the more you have, the less likely you are to be accepted for more cards. It's best not to apply for lots of cards if you may need credit for something important, such as a mortgage or a balance transfer card. Full info in our Credit rating guide.

Is it worth going for a card that gives bigger rewards in one store?

If you spend a substantial amount of money in a store then it certainly is. But don't let this blind you for the rest of your spending – make sure you maximise what you get elsewhere too (it may be worth having two cards).

Also remember that lots of cards use a 'double earn' promise, so it looks like you get more points using your credit card in the linked store, but actually you would've got the same just using its normal loyalty card. See our Loyalty points guide for a full explanation.

Which reward card is best for me?

This largely comes down to two things – which rewards you value and which cards will accept you. Generally speaking, reward credit either offer cashback on spending or award you loyalty points as you spend, which you can typically convert into vouchers or air miles.

Take a look at our top-pick cards above to compare the rewards on offer, and decide which you would make use of the most. Our Reward Credit Card Eligibility Calculator will then show you the acceptance odds for most of the top cards before applying.

What can I use my Amex points for?

Amex points give you a choice of rewards (with varying values), so what to go for will come down to both your preferences, and how best to maximise the value. You should receive points within a couple of days after spending, though they can take up to 30 days.

See the full list of ways to redeem your points on the Amex Membership Rewards site – some options include cashing in for gift cards, using them to spend on Amazon and transferring them to Nectar points.

Do reward cards affect your credit score?

Yes – reward cards can affect your credit score, but the impact depends on how you use them. Applying for a card usually causes a small, temporary dip due to a hard credit check. However, if used well, a reward card can actually help your score by showing reliable, on‑time repayments and responsible credit management.

That said, missing payments, repaying late, carrying high balances or using most of your available credit can all harm your score. Applying for several cards in a short time can also reduce your chances of being accepted for future credit.

Why can you trust MoneySavingExpert?

MoneySavingExpert.com is the UK’s biggest consumer finance website, founded by Martin Lewis, offering impartial, research-based tips.

The site's dedicated to cutting your bills and fighting your corner with journalistic research, cutting-edge tools and a massive community – all focused on finding deals, saving cash and campaigning for financial justice.

Share this guide?