Top Lifetime ISAs (LISAs)

How they work, who they're for and which provider pays the most

A Lifetime ISA (LISA) can be opened by anyone aged between 18 and 39. You can use one to save up to £4,000 a year, towards either a first home costing up to £450,000 or for retirement, with the state adding a bonus of up to £1,000 a year on top. This guide takes you through how LISAs work, whether they're right for you, how you get the bonus and the best buys.

Top-pick Lifetime ISAs

The Government is launching a new First Time Buyer ISA

The Government has confirmed that it will be replacing the Lifetime ISA (which replaced the Help to Buy ISA) with a new savings product which will pay a bonus to first-time buyers. You'll still be able to open a Lifetime ISA until then and you'll be able to continue to deposit into and use your LISA/Help to Buy ISA after the new product launches. See our First Time Buyer ISA guide for details of what we know so far.

What is a Lifetime ISA?

A Lifetime ISA (LISA) lets you save up to £4,000 every tax year towards a first home or your retirement, with the state adding a 25% bonus on top of what you save. That means you could get a chunky £1,000 of free cash annually. Plus you earn interest on whatever you save, and as it's an ISA (Individual Savings Account), that interest is tax-free.

-

Who can open one? Those aged 18-39 – full info below.

-

When can I use my cash and the bonus? Either when you buy your first home to use towards a deposit (see LISA for first-time buyers). Or after you hit 60 (see LISA for retirement). If you use a LISA to help buy your first home, you can retain the account and keep saving in it for your retirement.

-

How long do I need to have a LISA? You must have had a LISA for a year to be able to use it (and the government bonus) towards your first home.

Lifetime ISAs are complex products, so it's worth spending time reading our below need-to-knows in full before deciding if it's the right choice for you.

From The Martin Lewis Money Show Live on Tuesday 26 November 2024, courtesy of ITV. All rights reserved. Watch the full episode on ITVX.

Martin Lewis: LISAs have a flaw - you can be fined for buying your first home

Lifetime ISAs (LISAs) work well for many, but there's a growing hole which needs addressing.

If you try to use LISA savings to buy a home above the £450,000 threshold (which hasn't moved since LISAs launched in 2017), you're effectively fined 6.25% of your money (so £625 per £10,000 saved) to withdraw it. This is unfair, especially for many young people who've already been priced out by inflation.

Martin and MSE have been campaigning to get rid of this fine. Our latest news story has full info, including Martin's response to the recent Treasury Committee report which backed our calls for LISA reform.

How a Lifetime ISA works

Here we've general need-to-knows about how Lifetime ISAs work. As well as reading these, it's also worth reading the need-to-knows about using the LISA as a first-time buyer, or using the LISA for retirement, depending on how you plan to use it.

You get a 25% bonus each tax year on up to £4,000

You can save up to £4,000 a year in a LISA as a lump sum or by putting in cash when you can. The state will then add a 25% bonus on top. So if you save £1,000, you'll have £1,250 and if you save the full £4,000, you'll have £5,000. And that's before interest or growth.

-

The bonus is paid every year you save something in to your LISA, until you hit age 50.

-

The bonus is paid monthly (if you've contributed that month) and takes between four and nine weeks to arrive.

-

You only get the bonus on contributions, not cash interest or investment growth.

-

Once in your account the bonus is counted just like the rest of your savings, so you'll get interest on it too (or investment growth/loss).

-

The maximum bonus is £33,000 if you open it at 18, and max it out until you hit 50 (unless you're born on 6 April, when the max is £32,000).

You must be aged 18 or over but under 40 when you open a Lifetime ISA

Anyone aged 18 to 39 can open a LISA.

For (grand)parents wanting to help their (grand)kids buy a home, giving them cash to put in a LISA is a great way to do it – though they'll need to open the LISA account themselves as you can't do it for them.

If you're pushing 40, make sure you open one before you hit the cut-off age. You can continue to put money into the LISA until the day before your 50th birthday (once you're 50 or over you'll continue to get interest or investment growth/losses but you won't be able to pay in any more).

If you want to transfer it to a new provider, for example to get a better interest rate, this is allowed – and you can add to it then. You just can't open another for new money only.

As always when there's an age limit, some will miss out. For the many people who have asked us "Isn't this age discrimination?", the answer is yes, it is. However, it is not illegal age discrimination; no more than setting a state pension age is. If it's not right for you, see our Top savings, Top cash ISAs and Pension savings guides.

Already own a home? A LISA can still work as a retirement booster (if you’re under 40)

If you’re aged 18 to 39 and already own a home, you can still open a Lifetime ISA. You just can’t use it to buy property – instead, it becomes a long-term, tax-free retirement savings pot.

That can still make it well worth having:

-

You get a 25% state bonus on anything you put in (up to £4,000 a year), until age 50

-

All money taken out from age 60 is tax-free

-

It can sit alongside other retirement savings like your pensions, giving you an extra pot that isn’t taxed when you withdraw it

Even £1 now could be a smart move

If you’re under 40 and you might want to use a LISA for retirement one day, it can be worth opening one with as little as £1 just to get the clock ticking now.

You won’t be able to access the money penalty-free until age 60, so it’s not for short-term savings. But as a set-and-forget option for future you, it’s one of the few products where the Government still hands you a guaranteed bonus.

Your interest (or investment growth) is tax-free in a Lifetime ISA

The Lifetime ISA is, well, an ISA – an individual savings banking account – which is a place to save where the interest you make is tax-free.

You can put up to £20,000 in ISAs in this tax year – and the money you put in your LISA will count towards that. So if you put £4,000 in the LISA this tax year – on top of which you'll get a 25% state bonus – you'll be able to put £16,000 into other ISAs. The bonus you get doesn't count towards the year's ISA allowance.

How the tax works depends on whether you're saving in cash or investing...

Cash LISAs

Interest is paid tax-free on the amount you contribute and on any state bonus that's already in the account when the interest is paid. You get to keep all of this interest, and the next year you'll earn interest on that too – this is known as 'compound interest'.

Also, the interest earned doesn't count towards your personal savings allowance, so there's no impact on your ability to earn £1,000 a year of interest tax-free as a basic-rate taxpayer from other savings (£500 if you're a higher-rate taxpayer).

Investment LISAs

This is more complex as investment gains come in three main types: dividends, capital gains and bond interest. You might pay tax on these outside a LISA, but within a stocks & shares LISA you don't pay tax on any of them.

You can open and contribute to a cash ISA and a Lifetime ISA in the same tax year

The overall ISA limit is £20,000 in the 2026/27 tax year. You are allowed to split this between one LISA (up to the maximum £4,000) and put the remainder in cash ISAs, stocks & shares ISAs and/or innovative finance ISAs (for peer-to-peer investing) in the same tax year.

You're also allowed to hold a Help to Buy ISA and a LISA at the same time, though you can't get the first-time buyers' bonus on both (see Help to Buy ISA vs LISA info below). But you could get the Help to Buy ISA bonus for a home and then use the LISA and its bonuses for retirement.

For full info on the different types of ISA available, see our Full ISA guide.

Can I transfer cash from other ISAs in to my Lifetime ISA?

If you already have an ISA, some providers let you transfer money from that into your Lifetime ISA (even if your other ISA isn't a Lifetime ISA). Even then though, you can only transfer £4,000 from other ISAs into the LISA in any one tax year (this includes Help to Buy ISAs).

As with any ISA transfer, anything you've moved from previous years' ISAs does not affect your overall current tax year's contribution.

For instance, if you transfer £4,000 into a LISA from a previous year's ISA in the 2026/27 tax year, you'd still be able to deposit £20,000 into a cash ISA, stocks & shares ISA or an innovative finance ISA (or a split between two or three of these) within the same tax year, but you'll have used up your £4,000 LISA allowance for 2026/27.

You'll pay a penalty if you withdraw the cash and don't use it for a first home or retirement

Under the normal LISA rules, you can take some or all of your cash out of a LISA before age 60 even if you're not buying a property – but you're charged 25% of the amount withdrawn, so it's best to try to only use the LISA if you're sure the cash is for one of the two defined purposes: buying a first-home costing £450,000 or less, or retirement.

The rules are the same for partial and full withdrawals – here's how they work in practice...

-

Withdrawals have a 25% penalty, equivalent to a loss of just over 6%. At first glance the fact you've had a 25% bonus added and then a 25% penalty would seem to leave you back where you started. Yet unfortunately the maths doesn't work like that...

Imagine you saved £1,000 and so got a £250 bonus, you'll have £1,250 total (ignoring interest, for ease). If you then withdrew it and closed the account, the 25% penalty would be £312.50. So you'd get £937.50 back.

In effect, the maths means that withdrawing for reasons other than buying your first home or retirement loses you 6.25% of what you contributed.

-

You don't pay the withdrawal charge if you die or are terminally ill. The LISA rules state that if you have less than 12 months to live, you retain the bonus with no penalties. If you die, any LISA money including interest and bonuses is passed on to your beneficiaries without penalty, though it'll no longer be in an ISA 'wrapper', and will form part of the estate for inheritance tax purposes.

Once it's opened, you're not locked in – you're free to transfer it to another provider

Once you've got the LISA open you don't have to stick with the provider you pick at the start.

As with normal ISAs, interest rates on cash LISAs will go up and down – so you'll need to keep an eye on your account, and be ready to transfer between different LISA providers to up the rate if you see a better deal.

The same is true with stocks & shares LISAs: you may decide to change your investment priorities, or seek out lower fees, in which case you'll be allowed to move it.

You can only open and subscribe to one LISA per tax year. If you want to transfer your current year's subscription you must transfer it in full.

However, many providers only accept transfers if you're aged 18 to 39 – options can be limited if you're 40 or older. Although interest rates on LISAs are variable – and so can change at any time – watch out for rates which include fixed-term bonuses, as the rate falls (often considerably) after the bonus period ends. It may be worth avoiding these if you're approaching 40 – so that you're not locked in at the lower rate once the bonus period ends.

Lifetime ISA need-to-knows for first-time buyers

If you're a first-time buyer, or you might be in the future, you need to read these need-to-knows, as the Lifetime ISA isn't a straightforward savings account, and it won't be right for everyone.

Plus, if you've come here without reading the general need-to-knows above, it's worth going back and reading those, as there's important information about how the accounts work, and the withdrawal penalties you could face if you need to get the money out.

A first-time buyer is someone who's NEVER owned a property anywhere in the world before

If you've owned a property before – whether inside or outside the UK – you can't use a LISA towards a home purchase.

This includes owning a property (or a share of one) that you inherited, even if it was sold straightaway and you didn't live there. If you owned a company or had a trust that owned residential property that you are (or were) able to live in, you're also not considered a first-time buyer.

You must be buying a residential UK property to live in that costs £450,000 or less

To get the bonus you'll need to buy a property that costs £450,000 or less with any residential mortgage (so you can't be a cash buyer and the mortgage can't be a buy-to-let deal).

While this will be enough for most, some buying in expensive areas have fallen foul of this rule. MoneySavingExpert has called for reform to this threshold to allow those who end up buying a property costing more than the maximum property price to get their money out of a LISA without penalty, and in the longer term to raise this maximum property price in line with house price inflation.

But, if you don't yet have a LISA, don't count on any changes - make sure it's right for you BEFORE opening an account.

You can use the Lifetime ISA with other Government schemes including Right to Buy, shared ownership and Help to Buy loans. You can even use it if you're doing a self-build.

You can get the money in time for exchange on your property, meaning you can use it towards the deposit requested by the person you're buying from (the exchange deposit), as well as the deposit the mortgage company will want on the property at completion. See the difference between these.

The LISA is intended to help you buy your first home, so you're not supposed to rent it out immediately after buying it (though you can if your circumstances change down the line).

QUICK QUESTIONS

Can I use an ISA for a self-build property?

Yes. You'll be able to put LISA savings, including the bonus, towards the purchase of the land for a self-build property, provided you still meet the other criteria (for instance, the land's in the UK, you're buying it with a mortgage, it costs £450,000 or less and you complete within 90 days of withdrawal, and that the home you intend to build is your first home and you intend to live in it).

The Treasury advises that if you're in any doubt about whether a LISA can be used, your solicitor should be able to help.

Can I use the LISA to 'staircase up' if I have a shared ownership property?

If it's just you wanting to 'staircase up' the amount you own, you can't use a LISA as you already own a share of a property.

Yet if you have a partner who's a first-time buyer, and meets all the other requirements above, they will be able to use the LISA and bonus to help you staircase up. Note that your partner will need to be named on the title deeds of the property to show they have used their LISA and bonus towards the purchase.

Is there a minimum mortgage amount to be able to use the LISA?

No, the only criteria is that you buy with a residential mortgage (so not buy to let). However, if you could be a cash buyer, and are just getting a mortgage to be able to use the LISA, do the maths to make sure it's worth it.

Most lenders have a minimum lending amount, often £20,000 or £25,000, so you'd need to borrow that much. You'd also need to pay for a lender's valuation and legal work when purchasing the property, and the mortgage you get may have early repayment penalties if you plan to pay off the entirety of the mortgage in the first months of it.

If you plan to do this, always ensure that the amount you get from the state bonus is more than the mortgage will add to your purchasing costs over being a cash buyer.

You need to have opened your first LISA for a year or more to be able to use it for a home

You need to have held a LISA for at least 12 months to be able to use it (and the bonus) towards your first home WITHOUT paying a penalty – use it before and you'll pay a withdrawal charge, which wipes out the bonus and a bit more on top.

You're free to transfer an existing LISA elsewhere at any point (for example, to get a higher interest rate) – it'll be the same LISA, just with a different provider, so the clock doesn't reset. For example, open a brand new LISA and switch it after six months and you'll only have to wait another six months before being able to use it penalty-free.

It's also possible to open new LISAs alongside existing ones IF they're opened in different tax years – but while it's possible to hold multiple LISAs, you can only pay in to one LISA each tax year. If you've multiple LISAs, you can withdraw from each of them penalty-free when you purchase your first-time property, providing that each LISA has been open for at least a year. You can also transfer them all into one LISA if you wish.

If you haven't started a LISA and need to buy within a year, then you'll need to save elsewhere, and won't be able to use this scheme.

Wannabe first-time buyer? Even if you've no savings, you can open a LISA with £1 to start the clock

As you must have had a LISA open for a year to be able to use it for a first home, most people with even an inkling of being a first-time buyer should open a LISA with the bare minimum (can be just £1) just to get the clock ticking – in case you want to add to it later. Watch Martin's video explainer below for full details...

So, if you then don't end up buying a property, or you buy one that's over £450,000or overseas, for example, you can withdraw the £1 and you'll only have lost out by about 6p.

Yet if you do want to use it, even if you've just had £1 in it for a year, you can then put £4,000 in (the annual maximum) and within a month or so you'll get the bonus, so you'll then have £5,000 in it ready to put towards your deposit.

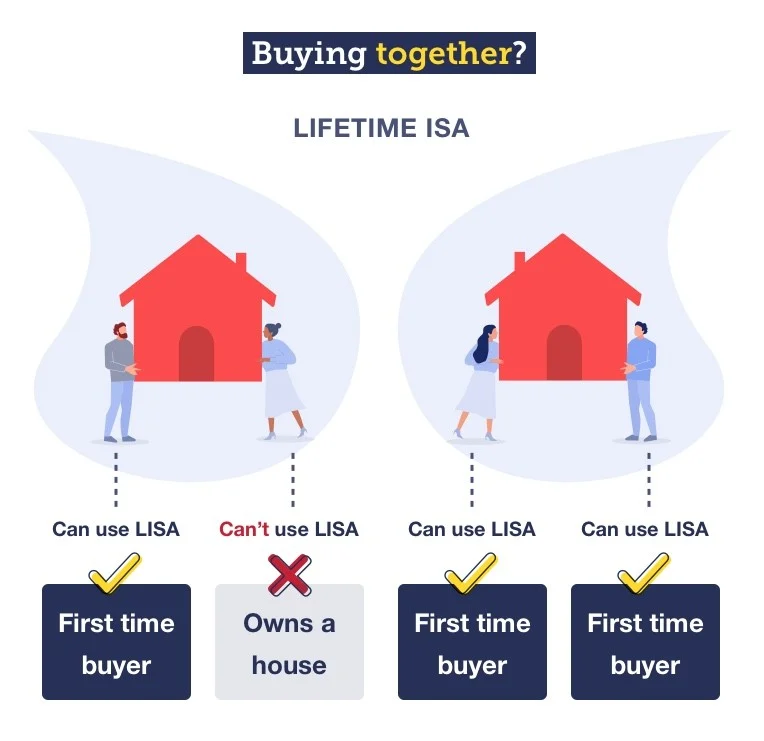

Each person has their own LISA, so couples can have one each

If you're planning to buy a home together, it's important to understand that there's no such thing as a joint LISA: you and your partner/spouse need to open separate ones. Here's how it works:

-

If you're a first-time buyer making a purchase with someone who's owned before, you can still open one and use it towards a home purchase together, but the partner who's previously owned a property can't open one.

-

If you're both first-time buyers buying a property together costing £450,000 or less – you can both open one and save in it, essentially doubling the bonus. Note: even if you're both using the LISA, the £450,000 limit is strict. It doesn't double because you're both using the LISA cash

Got a Help to Buy ISA? You can transfer it to a Lifetime ISA, but you'll need to time it right to make it work

Martin sums up the differences between the Help to buy ISA and the LISA best in his Should I move my Help to Buy ISA into a Lifetime ISA? blog. He also weighed up the pros and cons on his show, which you can watch in the video below.

From The Martin Lewis Money Show Live on Tuesday 26 November 2024, courtesy of ITV. All rights reserved. Watch the full episode on ITVX.

The Help to Buy ISA (H2B ISA) is closed to new applicants. If you already have one you can open a LISA as well (if you're aged 18 to 39).

Important: you can only use the bonus from ONE of them towards buying a home. So, unless you want to use the LISA and its bonus for retirement savings, the main decision is whether or not to keep the H2B ISA, or transfer it to a LISA.

In brief: you should stick with your H2B ISA if...

-

You'll be buying a qualifying property very soon. A LISA has to be open at least a year to use it for a first home.

-

You're not sure you'll be buying at all. You'll pay a penalty to withdraw cash from a LISA, unless used for your first home or retirement. Unlike the H2B ISA, where you can withdraw your cash whenever you like (without the bonus).

-

You've more than £4,000 saved in a H2B ISA, and you're buying a qualifying property soon. Because transfers count towards your LISA allowance, you can only transfer over £4,000 each tax year from a H2B ISA to a LISA. So if you have £12,000 in a H2B ISA, it'd take three tax years to transfer it to a LISA. If you're going to transfer, make sure you have ample time before you're planning to buy to move your cash.

Consider transferring to a LISA if...

-

You've more to save each year. You can save up to £4,000/year in a LISA, versus £2,400/year in a H2B ISA. Plus, there's a cap on H2B bonuses of £3,000 total – so £12,000 saved. If you can save more than that, you'll be better off with a LISA which has a maximum bonus of £33,000 (if you saved £4,000/year from age 18 to 49).

-

The home you want to buy costs more than £250,000. The H2B ISA can be used for a property costing up to £250,000, or £450,000 in London. The LISA has a flat £450,000 anywhere.

-

You won't use your bonus in the next few years. You can only pay in to an H2B ISA until November 2029 and can only use your bonus until November 2030.

Below is our full LISA vs H2B ISA comparison...

LIFETIME ISA (FOR HOME PURCHASE) | HELP TO BUY ISA | |

Max contribution? | £4,000/year | £2,400/year (£3,400 in year one) |

Lump sums? | Yes | No, need to save monthly |

Max bonus? | £33,000 (assumes max contribution every year from age 18-49) | £3,000 (assumes max contribution over four years and eight months) |

When's the bonus paid? | Monthly | On completion when you buy a home |

Investment option too? | Yes, via stocks & shares LISAs | No. Cash savings only |

Max property price? | £450,000 | £250,000 (£450,000 in London) |

How quickly can you use it? | After the LISA's been open 12mths | Once you've £1,600+ saved (can be done in min 3mths) |

Who can open it? | Anyone aged 18 to 39 | No one. Applications closed in Dec 2019 |

What can it be used for? | The home deposit and mortgage deposit | Just the mortgage deposit |

Can I withdraw money if not buying a home? | Yes, at age 60+; if earlier you don't get the bonus and will pay a penalty | Yes, at any time, you just don't get the bonus |

How to transfer your Help to Buy ISA savings into a Lifetime ISA

If a LISA wins for you, you just need to open one and move the money across. You can only transfer up to £4,000 this tax year (less if you've already paid in to the LISA) as any money transferred from a H2B ISA to a LISA counts towards the allowance. Here's how to transfer the money:

-

If the LISA provider allows transfers from a H2B, fill in its transfer form as you apply. This then won't reduce your overall £20,000 ISA limit. The transfer should take two to four weeks.

-

If it doesn't accept transfers, you'll have to just withdraw the money. You should be able to find a top payer that accepts transfers in, but if you can't or want to go with a provider that doesn't, you'll have to just withdraw the cash from the Help to Buy ISA and pay it in to the LISA.

This will mean your overall £20,000 ISA limit is reduced for the tax-year in which you make the deposit, though if you're unlikely to use this anyway, it's not a huge deal.

If you have more than £4,000 in your H2B ISA, you'll need to move £4,000 now and then ask to transfer the rest when the next tax year starts. Some H2B ISAs may close your account when you transfer some of the money out, in which case you'll need to close it down, take the money out and save it elsewhere (see top savings) until you can put it in a LISA.

Ready to buy? Ask the LISA provider to transfer money to your solicitor – don't withdraw cash yourself

When you're ready to buy, ask your LISA provider to transfer the cash directly to your conveyancer/solicitor, not to you. If you do withdraw it to an account in your name, you'll pay the 25% withdrawal charge. All your savings, including the bonus, will be available to use at exchange.

Yet don't be too hasty – the property purchase needs to complete within 90 days of you sending savings from the LISA to your solicitor (see how buying a home works for likely timelines). If your purchase is going to take longer, either delay taking the money out of your LISA, or ask your solicitor/conveyancer to write to HM Revenue & Customs to get an extension on the 90-day limit.

Don't worry if your purchase ends up falling through – you won't lose out. In this case, the funds will go back to the LISA account they came from. This won't affect your annual contribution; you'll still be able to contribute up to £4,000 that tax year (unless you already have).

Lifetime ISA need-to-knows for retirement savers

If you're planning to use the Lifetime ISA for retirement, this section tells you what you need to know to decide if it's right for you. If you've not read the general need-to-knows above, it's worth going back and reading them, as there's important information about how the accounts work, and the withdrawal penalties you could face if you need to get the money out before you're 60.

You can only access your LISA funds at age 60 – so you need to be in for the long haul

Even for the oldest people who can get a LISA, 60 is two decades away. The rules could be changed within that time, for good or bad – like any form of retirement savings. Here's how they stand now...

-

You can access the cash on or after your 60th birthday. Then use it for whatever you like.

-

You don't have to take it all at once. You can make partial withdrawals.

-

If you leave it in the LISA it will still continue to get interest or investment growth/loss.

The LISA doesn't simply stop at age 60; it'll still be an active product.

-

You don't pay tax on the cash. All money taken out of a LISA for retirement is tax-free.

-

LISA savings will affect your eligibility for benefits. Unlike a pension, which isn't counted as savings for means-tested benefits, the LISA will affect your eligibility for them. So you could have to pay to withdraw your LISA retirement savings and live off those until your savings are down below the means-testing threshold. Similarly, they count as assets in bankruptcy or divorce cases.

Pensions usually come first – but a LISA can still play a useful supporting role

The LISA is designed as a way to save for retirement, much like a pension. You don’t have to choose one or the other – you can have both, and many people use a LISA alongside a pension, rather than instead of one.

That said, they work in very different ways, and which suits you best depends on your circumstances.

With a pension, you save from gross (pre-tax) income. So, as a basic-rate taxpayer, saving £100 only costs you £80 from your pay packet, as that’s all you would have received.

With a LISA, you save from net (after-tax) income. So putting in £80 costs you £80, but the Government then adds a 25% bonus – meaning you again end up with £100.

On the surface, that looks similar for basic-rate taxpayers, but the differences below can be important.

Where a pension usually has the edge

-

If you’re employed, auto-enrolment means your employer contributes to your pension; they don’t contribute to a LISA. For many, this is the single biggest advantage.

-

If your employer offers salary sacrifice, you can also save on national insurance.

-

Higher- and additional-rate taxpayers get more generous tax relief through pensions than the LISA bonus.

-

Pension savings don’t count towards means-tested benefits, while LISA savings do.

-

Pensions are usually protected in bankruptcy, while LISA savings can be taken by creditors.

-

You can normally access pensions earlier (currently from age 55, rising gradually to 58), while LISAs can only be accessed penalty-free from age 60.

Where a Lifetime ISA can add something extra

-

All withdrawals from a LISA at age 60+ are tax-free, unlike pensions where most withdrawals are taxed. See how LISA withdrawals work.

-

You can access LISA savings early if needed (though you’ll take a withdrawal penalty).

-

For some – particularly basic-rate taxpayers and the self-employed a LISA can be a useful additional retirement pot.

Using a LISA alongside a pension

For most people in work, a pension is likely to be the main foundation of retirement saving. But that doesn’t mean a LISA has no role.

If you’re under 40, opening a Lifetime ISA – even with just £1 – keeps the option open to use it as a tax-free retirement top-up later on. You can then decide over time whether and when to add more, up to age 50, while continuing to save into a pension as well.

As this is a complex area, the table below sets out the differences side-by-side to help you decide what’s right for you.

LIFETIME ISA | PENSION – BASIC-RATE TAXPAYER | PENSION – HIGHER-RATE TAXPAYER | |

Employer contribution | None | Yes – 3%+ of salary (see auto-enrolment) | Yes – 3%+ of salary (see auto-enrolment) |

State contribution | 25% | 25% (20% tax relief) | 66% (40% tax relief) |

Max amount you can you save/yr? | £4,000 | £60,000 (max amount with tax relief) (1) | £60,000 (max amount with tax relief) (1) |

When is bonus/tax relief paid? | Monthly | Immediately (2) | 25% paid immediately, rest must be claimed (2) |

Who can open one? | Anyone aged 18-39 | Anyone aged 16+; parents can open one for you from birth | Anyone aged 16+; parents can open one for you from birth |

When can you access it? | Age 60 (accessible before for a penalty) | Age 55 (rising to 57 from 2028) | Age 55 (rising to 57 from 2028) |

Do I pay in from pre or post-tax income? | Post-tax income | Pre-tax income | Pre-tax income |

What tax will I pay on withdrawal? | Tax-free | 25% tax-free, rest taxed at your income tax rate | 25% tax-free, rest taxed at your income tax rate |

Liable for inheritance tax? | Yes | No (yes from April 2027) | No (yes from April 2027) |

Affects pre-pension-age benefits entitlement? | Yes | No | No |

Can be taken to pay creditors in bankruptcy? | Yes | No | No |

(1) You can carry unused allowances over from previous years, meaning that technically you could contribute up to £180,000 in the 2026/27 tax year. However, you'd need to earn at least this to get this much tax relief. For a fuller explanation of the annual allowance, see pension need-to-knows. (2) Unless you contribute by salary sacrifice in which case the saving's made by paying in from pre-tax income.

Top-pick Lifetime ISAs

Below are the top cash Lifetime ISAs, as well as some stocks & shares Lifetime ISAs to try.

Cash Lifetime ISAs – what we'd go for

App-based Moneybox's 4.45% is top, including a 1.65% fixed 12-month bonus. Just note that the bonus interest is paid after the first year and you must keep the account open for at least 12 months to get it. You can transfer in from other LISAs, provided you've never held a Moneybox LISA before. Or for an online account there's Paragon Bank at a lower 3.51%.

Both of these allow you to transfer in from existing LISAs. If you want to transfer in from another type of ISA (eg Stocks & Shares), you'll have to sacrifice on rate considerably with Skipton Building Society at a paltry 2.05%.

| Provider | Rate (AER variable) | How to open/manage/transfer? | When is interest paid? | |

|---|---|---|---|---|

Top Lifetime ISAs. Here are the highest paying fee-free Cash Lifetime ISAs for new customers. |

||||

| Moneybox | 4.45% (min £1) | App. Transfers allowed, only if you've not had a Moneybox LISA before. | Monthly (1) | £120,000, shared with |

| Plum | 4.4% (4.01% on transfers in, min £1) | App. Transfers allowed from existing LISAs only | Monthly (1) | £120,000, shared with Lloyds Bank and Citibank |

| Tembo | 4% (min £1) | App. Transfers allowed from existing LISAs only. | Monthly | £120,000, shared with |

| Paragon Bank | 3.51% (min £1) | Online. Transfers allowed from existing LISAs only. | Annually | £120,000 |

| Bath Building Society | 2.6% (min £1) | Online / branch. No transfers in. | Annually | £120,000 |

| Skipton Building Society | 2.05% (min £1) | Online. Transfers allowed. | Annually | £120,000 |

|

(1) Interest from the bonus portion of the rates are paid after a year. |

||||

Stocks & shares Lifetime ISAs to try

Investing isn't MoneySavingExpert's area of expertise - we're not financial advisors. So we don't tell you here what the 'best' stocks & shares Lifetime ISA platform for you is, or tell you what funds or shares to put your money in once you've chosen a platform. What we've done is pull out some of the more well-known platforms so you have somewhere to start your own research.

While returns from investing generally beat savings interest over the longer term, there are no guarantees – the value of your investments could go down. If you're new to this, we suggest you at least read our Investing for Beginners guide so you understand a little more before jumping in.

There are two main types of investment LISA – those where you make your own investment decisions from a wide range, and those that will help you choose your investments.

Upcoming changes to Stocks & Shares ISA rules

From April 2027, you will be taxed at 22% on interest earned on cash held in a non-cash ISA, such as a stocks and shares ISA or innovative finance ISA. Read our full story here.

'Do-it-yourself' Lifetime ISAs

The three LISA providers below allow you to choose from tens of thousands of investment options, from shares to funds and more. While you can opt for simple, fully-managed funds where you put your money in and investment decisions are made for you by a financial advisor, these platforms may be more suitable for experienced investors.

If you're not sure, or overwhelmed by choice, the two 'simpler' LISAs below may be more suitable, as they come with a limited range of funds you can invest in, and tend to be fully managed as standard.

Platform + min deposit | Management fee | Fee to buy/sell funds | Fee to buy/sell shares (1) | How to manage |

|---|---|---|---|---|

Dodl | 0.15% per year (min £1/mth) | None | None | App |

AJ Bell* | 0.25% per year (£3.50/mth max for shares) | £1.50 | £5 | Online / app |

Hargreaves Lansdown* | 0.25% per year (£45/yr max for shares) | £1.95 | £6.95 | Online / app |

(1) Fees based on up to 10 trades of UK shares per month, providers offer discounted rates for more frequent trades. You can trade overseas shares but expect to pay a currency exchange fee of up to 1%.

Simpler Lifetime ISAs with a limited choice of funds

The three Lifetime ISAs above are for those happy to take a hands-on approach to managing their stocks & shares LISA. The LISAs below are likely to be more suitable if you want a simpler investment choice, as they tend to have limited numbers of funds designed for different risk profiles – though be aware they tend to charge higher fees than the 'DIY' options above.

Platform + min deposit | Management fee | Average fund costs (incl. market spread) | How to manage |

|---|---|---|---|

Moneybox | £1/mth (free for first three months) + 0.45% per year | 0.07% to 0.69% per year | App |

JPMorgan Personal Investing* | 0.45%-0.75%/yr | 0.18% to 0.43% per year | Online / app |

Last updated: 02 June 2026.

Share this guide?