Top savings accounts

Top easy access & fixed savings, savings tax & ways to boost your rate

You can have as many types of savings accounts as you like, so mix 'n' match to suit your needs & maximise your interest. This guide covers top easy-access & fixed accounts, specialist rate boosters, plus savings tax & ways to reduce it.

-

Top easy-access (variable) savings. The simplest type of savings. You can put cash in and take it out whenever you want, but the rate can change, so ditch & switch if it falls behind the top payers. Put all cash you don't imminently need into one of these.

Tembo Homesaver 4.55% | Cahoot 4.52% | Trading 212's 4.51% cash ISA | Saga 4.5% | Chase 4.5% -

Top fixed savings. You get a guaranteed interest rate, without needing to monitor it, but in return you usually have to lock your cash away. If you know you won't need to access your cash, put it in a fix to get rate certainty, then you can forget about it till the fix ends.

One year: Habib Bank Zurich UK 4.91% | Two years: Recognise Bank 4.86% -

Specialist ways to boost interest. These pay up to a massive 50% interest. But they limit who can open & how much you can pay in. Check if you can get them.

-

Are you going to pay tax on your savings? There are more allowances than you think. If you do (or will) pay tax, you should look at a cash ISA.

All banks that we list are fully UK-regulated & covered by the Financial Services Compensation Scheme (FSCS)

The FSCS protects 100% of the first £120,000 you have saved, per UK-regulated financial institution (not per account). So in simple terms, if your bank were to fail, the FSCS aims to get any savings up to this amount back to you within seven working days.

If your bank is part of a larger group, protection can be split between each brand – you can use our Which banks are linked? tool to check. Full info in Are your savings safe?

Martin Lewis: 3 key things to consider before saving

While building up savings, especially for emergencies, is a crucial aim for everyone, it isn't necessarily always the first thing to do…

1. Saving is investing’s poorer cousin – should you be investing? The first place to put spare money is always to build up a cash emergency fund of three to six months' worth of bills. But for money you won’t use for 5+ years, saving isn’t usually the winner. It's worth considering putting some of the rest in a broad spread of investment (eg, a global tracker fund that mirrors the performance of a huge range of companies). Do read my new Beginners guide to investing.

2. Got costly debt? It's usually best to use spare cash to clear it first, after all pay off a grand’s on a credit card at 25% APR rather than save at 5% and you’re £200 a year better off. See Should I pay debt with savings?

3. Is overpaying your mortgage a better way to save? If your mortgage rate is the same or higher than you earn in savings, check our Mortgage Overpayment Calc to see if it may be worth you overpaying. If it looks likely, read Should I overpay my mortgage? for full pros & cons.

Top easy-access savings

Rates are variable, so they move, typically in line with the Bank of England base rate. But you've the freedom to withdraw at any point, so move your cash elsewhere if your rate falls behind the top payers. Bigger savers, with multiple accounts, may find savings platforms where you can move accounts between a panel of firms with just a click, far less hassle.

Most accounts allow unlimited withdrawals, though some do limit how often you can withdraw in return for a boosted rate – we highlight if this is the case.

Notice accounts are another type of variable account, but with these you can't withdraw whenever you want, you have to give advanced notice. See top notice accounts for full info.

Easy-access accounts – what we'd go for

A quick note before we get to the best buys: if you're saving over around £20k or are a higher-rate taxpayer, you probably want a cash ISA instead, see our full explainer below.

The benchmark rate is 4.5%: on up to £20k including a 1.55% fixed newbies' bonus (you have to keep the account open with £1+ for at least a year to get the bonus). Cahoot's Simple Saver pays 4.52% on up to £500k, though only lasts a year. Saga pays 4.5%* including a 1.64% fixed 12mth newbies' bonus. The product's aimed at over 50s but anyone can open it. Chase also pays 4.5%* including a 2.25% fixed newbies' bonus. Here, you'll need to open its free, easy-to-open current account (you needn’t switch & there's only an ID check, so no impact to your credit file).

Two ways to boost your interest to 5%:

5% on up to £3k for a year. The Cahoot Sunny Day Saver (a different account to the one above) pays 5% to new & existing customers with unlimited withdrawals on a small(er) amount.

Ends 11.59pm TONIGHT 5% until 4 December on up to £25k + an easy £25 cashback (which isn't ending). App-only to newbies until 4 Dec, with unlimited withdrawals, via its free, easy-to-open current account. Plus, go via our link for a £25 cashback deal which isn't ending (click link for full info).

Get 4.51% on up to £20k with a top cash ISA. A cash ISA is just a savings account where the interest isn't ever taxable. But even if you don’t need the tax benefit, cash ISA rates are high right now, so just open one & use it for normal savings.

Via our link, to newbies for a year on new money paid into it (ie, not ISA transfers), with unlimited withdrawals. Many more options in Top cash ISAs.

Top 'no fuss' option. Oxbury Bank pays 4.33% (min £1, max £120k) with unlimited withdrawals and no short-term bonus included in the rate.

|

Top easy-access savings accounts |

|

|---|---|

Top 'normal' savings accounts(In rate order – see what we'd go for above) |

Top rates from 'big names'(As we know some prefer to save with these) |

|

5% on small amounts - Account lasts 1yr (but rate is variable)

- Min. £1,

Max. £3,000

- Open online

- Interest paid: monthly or annually

- Sole or joint accounts |

- Account lasts 1yr (but rate is variable)

- Min. £1,

Max. £500,000

- Open online

- Interest paid: monthly or annually

- Sole or joint accounts |

|

4.55% on up to £20k

, 4.55%

- 3% variable + 1yr 1.55% bonus (account must be open 1yr to get the bonus, so if rate falls, move your cash but keep a min £1 saved)

- Min. £10,

Max. £20,000

- Open via app

- Interest paid: monthly (bonus paid after 1yr)

- No joint accounts |

Post Office, 4.31%

- 0.9% variable + 1yr 3.41% bonus

- Min. £1,

Max. £2m

- Open online

- Interest paid: monthly or annually

- Sole or joint accounts |

|

Top cash ISA, interest isn't taxable

, 4.51%

- 3.6% variable + 1yr 0.91% bonus

- Min. £1,

Max. £20,000 each tax year

- Open online or via app

- Interest paid: monthly

- Is a |

- 1.55% variable + 1yr 2.75% bonus

- Min. £5,000,

Max. £3m

- Open online or via app

- Interest paid: monthly

- No joint accounts |

|

The minimum you should be getting

, 4.5%

- 2.86% variable + 1yr 1.64% bonus

- Min. £1,

Max. £1m

- Open online

- Interest paid: monthly

- No joint accounts |

Tesco Bank, 4.21%

- 1.05% variable + 1yr 3.16% bonus

- Min. £1,

Max. £1m

- Open online

- Interest paid: annually

- Sole or joint accounts |

|

The minimum you should be getting

, 4.5%

- 2.25% variable + 12mth 2.25% bonus

- Min. £1,

Max. £3m

- Open via app

- Interest paid: monthly

- No joint accounts |

|

|

Top fuss-free option

Oxbury Bank - newbies only, 4.33%

- Min. £1,000,

Max. £120,000

- Open online or via app (need app to manage)

- Interest paid: monthly

- No joint accounts |

|

Ways to boost your interest.Some non-standard accounts pay higher rates. |

|

|

Must actively use its £3/mth current account

, 6%

- Requires its current account (click for info)

- Min. £1,

Max. £4,000

- Open online, via app or in branch

- Interest paid: monthly

- No joint accounts |

Ends 11.59pm TONIGHT 5% for short time + £25 cashback

, 5%

- 2.9% variable + 2.1% bonus until 4 Dec

- Min. £1,

Max. £25,000

- Open via app

- Interest paid: daily

- No joint accounts |

|

All rates are AER. Santander and Cahoot, and Tesco Bank and Barclays Bank, and NatWest, Ulster Bank and Saga share FSCS protection. |

|

Top fixed-term savings accounts

Fixed rates are set based on predictions of future UK interest rates. The advantages are that you know the rate, and it sticks even if UK rates were to drop. The disadvantages are that money is (usually) locked away, and if rates rise elsewhere you're stuck until the fix ends.

Fixed-rate savings accounts – what we'd go for

Top one-year fixed rate: Habib Bank Zurich UK pays 4.91% and can be opened with £1,000+.

Fix for longer at up to 5%: Investec pays 5% for its three-year fix while app-based Atom Bank* pays the same for five years.

Government-backed NS&I pays decent rates. Here deposits are guaranteed by HM Treasury up to £1m and rates are only a little lower than the very top payers. It has separate products where interest is paid back into the fix each year OR where interest is paid out to a bank account each month – so you can choose whichever suits you best.

Want to be able to access your cash if needed? Fixed-rate cash ISAs by law must allow you to access your cash early by closing the account in exchange for an interest penalty. Rates tend to be around 0.2% below top normal fixed savings, but can be worth it if you think you might need access to your cash before the term ends.

Want a short-term rate guarantee? While our focus is on one, two, three and five-year fixes, below those we've also included fixes of less than a year, as well as notice accounts, which can both give short-term rate security, if that's what you're after.

Top one-year fixed savings

| Provider | Rate (AER) | When can I access interest? | Min/max deposit | How to open? |

|---|---|---|---|---|

Top one-year fixes. |

||||

| Habib Bank Zurich UK | 4.91% | At maturity | £5,000 / £1m | Online |

| OakNorth Bank | 4.86% | At maturity | £1 / £500,000 | Online / app (joint accounts online only) |

| Recognise Bank | 4.86% | Monthly or at maturity | £1,000 / £250,000 | Online |

Top rates from big names. As we know some prefer to save with bigger brands. |

||||

| MBNA (part of Lloyds) | 4.85% | At maturity | £1,000 / £750,000 | Online (manage via phone only, no joint accounts) |

| NS&I | 4.72% | Monthly (paid away) or annually (paid into the account) | £500 / £1m | Online |

Top two-year fixed savings

| Provider | Rate (AER) | When can I access interest? | Min/max deposit | How to open? |

|---|---|---|---|---|

Top two-year fixes. In rate order. |

||||

| Recognise Bank | 4.86% | Monthly, annually or at maturity | £1,000 / £250,000 | Online |

| GB Bank | 4.85% | Monthly, annually or at maturity | £1,000 / £100,000 | Online |

| Close Brothers | 4.83% | Annually, paid away | £10,000 / £2m | Online |

Top rates from big names. As we know some prefer to save with these. |

||||

| NS&I | 4.7% | Monthly (paid away) or annually (paid into the account) | £500 / £1m | Online |

Ways to boost your interest. Beat the rates above with cashback via an online savings platform. |

||||

| 4.7% + possible £150 cashback | At maturity | £15,000 / £120,000 | Online (no joint accounts) | |

Top three-year fixed savings

| Provider | Rate (AER) | When can I access interest? | Min/max deposit | How to open? |

|---|---|---|---|---|

Top three-year fixes. In rate order. |

||||

| Investec | 5% | Annually, paid away | £5,000 / £250,000 | Online (new customers need smartphone, no joint accounts) |

| Close Brothers | 4.88% | Annually, paid away | £10,000 / £2m | Online |

| GB Bank | 4.87% | Monthly, annually or at maturity | £1,000 / £100,000 | Online |

Top rates from big names. As we know some prefer to save with these. |

||||

| NS&I | 4.68% | Monthly (paid away) or annually (paid into the account) | £500 / £1m | Online |

Top five-year fixed savings

| Provider | Rate (AER) | When can I access interest? | Min/max deposit | How to open? |

|---|---|---|---|---|

Top five-year fixes. In rate order. |

||||

| Atom Bank* | 5% | Monthly, annually or at maturity | £50 / £100,000 | App (no joint accounts) |

| Close Brothers | 5% | Annually, paid away | £10,000 / £2m | Online |

| GB Bank | 4.98% | Monthly, annually or at maturity | £1,000 / £100,000 | Online |

Top rates from big names. As we know some prefer to save with these. |

||||

| NS&I | 4.75% | Monthly (paid away) or annually (paid into the account) | £500 / £1m | Online |

Top shorter fixes & notice accounts

We've two options if you're after shorter-term rate security...

1. Fixing for six or nine months. Though rates here are lower than all the longer fixes above, and also lower than the top easy-access rates. So, they're not currently very compelling.

2. Notice accounts. Like easy-access, notice accounts have variable rates that move with the Bank of England base rate, but with these you can't withdraw at will, you must give advanced notice (usually 30 to 180 days). Historically, the lack of flexibility was in return for a rate boost above easy-access, but right now rates are lower, so they're not worth it for most.

But some notice accounts will give you at least the full notice period before any rate cuts kick in, so should UK interest rates fall, you'd benefit from a higher savings rate for longer compared to an easy-access account. We only include notice accounts that work like this.

| Provider | Rate (AER) | When can I access interest? | Min/max deposit | How to open? |

|---|---|---|---|---|

Top shorter-term fixes. In rate order. |

||||

| Atom Bank | 4.55% for nine months | Monthly or at maturity | £50 / £100,000 | App (no joint accounts) |

| Zopa | 4.5% for six months (must open its Smart Saver first) | At maturity | £1 / £250,000 | App (no joint accounts) |

Top notice accounts. Here you'll have to give notice before you withdraw. |

||||

| Secure Trust Bank | 4.21% for 90 days' notice | Quarterly, paid into the account or paid away | £1 / £1m | Online |

| Castle Trust Bank | 4.2% for 120 days' notice | Annually, paid into the account | £1,000 / £500,000 | Online |

Ways to boost your interest. Beat the rates above via an online 'savings marketplace'. |

||||

| 4.66% for a six-month fix | At maturity | £10,000 / £1m | App (no joint accounts) | |

| 4.17% to 4.21% for various notice accounts | Daily, paid into the account and annually, paid away | £10,000 / £120,000 OR £1m | App (no joint accounts) | |

Is now a good time to fix? How long should I fix for?

Fixed rates normally get stronger the longer you fix. That's not really the case right now, which shows the market's long-term view is interest rates will be pretty stable. So if you want to save, you can comfortably lock money away, and you strongly value certainty, then fixing – and fixing for longer – looks a decent option at the moment.

But remember, if you go for a longer fix and rates rise in the meantime, your money's locked away, so you can't move it to up the rate (except in a long fix cash ISA). Yet don't think you need to pick just one fix length. You can hedge your bets with several fixes of different lengths.

If you can lock away money for a longer period, say 5+yrs, and you've already got a cash emergency fund, savings may not be right for you. Give Martin's beginner's guide to investing a read - you're in the sweet spot for that, and done right, it could be far more lucrative.

How interest is paid can impact how much tax you'll pay

Interest crystalises for tax the moment you can access it. For fixes longer than a year, choosing to receive your interest monthly or annually, rather than at the end of the fix, can massively reduce your tax bill by spreading your interest over multiple tax years.

Though if the interest is paid out of the fix, it won't compound, so you'll not earn interest on the interest. If you leave it in, it will. Full info in our fixed interest explainer.

SPECIALIST rate boosters

If you can get these they're far more lucrative than other types of savings accounts. But they either limit who can get them, or how much you can put in. In order of maximum returns...

-

Help to Save: A 50% boost on what you save, if you work & are on Universal Credit. Here you can save up to £50/month, and after two years, you get a 50% bonus based on the highest balance you reached – even if you’d withdrawn the money. You can then repeat it for another two years for a second 50% boost. Full info in Help to Save.

-

Lifetime ISAs: A 25% boost for (wannabe) first-time buyers aged 18 to 39. A tax-free savings or investment account anyone aged 18 to 39 can open (once open, you can keep it going even after you're 40). Its primary use is to help first-time buyers build a deposit, though it can also be used to save towards older age. Full info in Top Lifetime ISAs.

The Government's also confirmed it'll launch a new first-time buyer product, likely in April 2027. Details are still sparse, but read what we know so far in our First Time Buyer ISA guide. -

Regular savings: Earn up to 8% on smaller amounts. These pay higher rates but limit how much you can pay in each month. The best rates are usually linked to current accounts (ie, you must have a provider's current account to open it). You can drip-feed lump sums into these to max your interest. Full info in Regular savings.

Try our new Savings Picker

Answer seven questions & our Savings Picker will show you which types of savings accounts suit you best, then the latest rates. Do share feedback on the MSE Forum.

How savings tax works and ways to reduce it

Savings aren't taxed, but interest earned is. Yet even then, many needn't pay it, as there are tax-free allowances & products you can use where the interest isn’t taxable...

1. Your three key savings tax allowances

Start by watching Martin's video explainer on how most people miss out on using savings tax allowances, which is an easy way to understand this topic quickly.

There's full info in our How savings tax works guide, but in brief these allowances are...

-

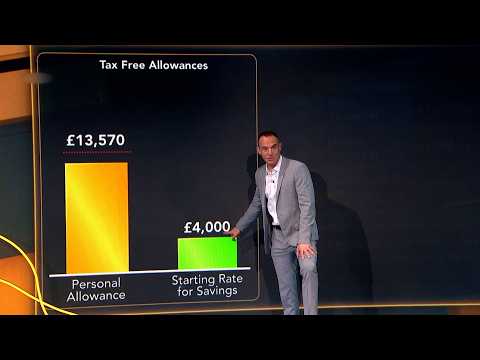

Personal Allowance: most can earn up to £12,570 tax-free. This is how much you can earn from any source (eg, work, pension, interest) before paying Income Tax. If your total earnings are less than that, all your interest is tax-free. Full info in Personal Allowance.

-

Starting Rate for Savings: for those with low other (including work) earnings but bigger savings interest. This means some can earn up to £18,570 of earnings & interest combined without paying tax. Full info in Savings Starting Rate.

-

Personal Savings Allowance: you can earn up to £1,000 interest tax-free each year. This is on top of the allowances above – it's the amount of interest you can earn from ANY & ALL SAVINGS without paying tax on it. Full info in Personal Savings Allowance.

- Basic 20% rate taxpayers can earn £1,000 interest a tax year.

- Higher 40% rate taxpayers can earn £500 interest a tax year.

- Top 45% rate taxpayers do not get a PSA.

Saving less than around £20,000? You likely won't pay tax. At today's top easy-access rates you'd need over £20,000 to generate £1,000 interest, so only basic-rate taxpayers with more would pay tax (for higher-rate taxpayers, it's half that). This, combined with cash ISAs below, means all but bigger savers or earners needn't pay any tax.

How you pay tax on savings if you need to. If you're sent a self-assessment tax form to do each year, you do it via that. If not, and your interest is under £10,000/year, you don't need to do anything – HMRC will simply change your tax code. If you get more than £10,000 interest, you'll need to do a tax return. See more on how to pay tax on savings interest.

2. You can save £20,000 tax-free each year in an ISA

Cash ISAs are just savings accounts where the interest:

- isn't ever taxable

- doesn't have to be reported to HMRC

- doesn't count towards the interest in the allowances above (eg, the £1,000 PSA for basic-rate taxpayers doesn’t include cash ISA interest).

All this makes ISAs a crucial extra allowance – on top of the allowances above – which anyone who earns or saves enough to pay tax on savings interest (or thinks they may do in future) should take advantage of. You can save £20,000 in a cash ISA this tax year, though from April 2027 this limit is set to fall to £12,000 for under 65s (to 'encourage young people to invest').

Though if you both save and invest, a shares ISA's tax benefits can far outweigh a cash ISA.

3. Maxed your ISA? You can put £50k tax-free in Premium Bonds

Premium Bonds aren't worth it for most people, though they can be useful if you pay tax on savings & have used up your ISA allowance, provided you put in a larger amount. For a full explanation, see Are Premium Bonds worth it? and our Premium Bond Prediction Calculator.

What are savings platforms and how do they work?

Savings platforms offer accounts from various banks that they partner with – often at higher rates than are available direct with that bank. Essentially, it's a way to easily switch between accounts, though rates are not always as good as those we've mentioned above.

The idea is, you open a single account with the platform, which then allows you to open multiple accounts with its partner banks in just a few clicks. You add money to your platform's holding account, then deposit in your chosen account from there.

We go through how these platforms work in detail in our Online savings platforms guide, including the best rates on offer and rundowns of how the main providers work. Some big names include Raisin, Hargreaves Lansdown Active Savings and Flagstone, though recently we've seen decent rates from Prosper and Meteor too.

Savings Q&A

What is the top account for joint savings?

This is a commonly asked question, but most savings accounts can be held by two people – so actually the question should just be: "What is the best savings account?", which this guide is set up to answer.

Except where noted, each of the accounts above can be set up as a joint account – so if you're looking to save with someone else, just head to our top easy-access accounts and top fixed-rate accounts.

Should I choose monthly or annual interest?

For some accounts you can choose for interest to be paid out to an external account (for example, your bank account), while others pay the interest back into the account itself.

You can often choose how often interest is paid too, for example monthly or annually, or for a fixed-term account, even at the end of the fixed term (at maturity).

Your choice can have a significant impact, as it's when you can ACCESS the interest that matters for tax reasons, which is not necessarily the same time as when the bank pays interest.

Here's an example to help explain...

Imagine you save £10,000 in a five-year fix which pays 4.5%.

-

Option 1: Interest is paid out of the savings account to your bank account each year, meaning you can access it when it's paid.

Here, you'd earn £450 each year for five years. As you'd be earning less interest than the basic- and higher-rate personal savings allowance (PSA) limits (£1,000/year and £500/year respectively), you'd pay no tax on the interest.

After the five years, you'd have earned a total of £2,250. -

Option 2: Interest is paid back into the fixed account each year, and you can't access it till the account matures.

Here, you'd earn interest on your interest, meaning that after five years you'd have earned £2,460 – about £200 more than with the first option. However, because you can't access the interest until the end of the five-year fixed term, all the interest counts towards the fifth year's PSA, and far exceeds both the basic- and higher-rate limits. This means you'd have to pay tax – about £292 for basic-rate taxpayers, £784 for higher-rate.

This means that, overall, basic-rate taxpayers would be £80 worse off than with the first option, higher-rate taxpayers a massive £570 worse off.

When is it beneficial to choose monthly or annual interest?

So some may want to have interest paid out to a bank account monthly or annually, so it's spread out over multiple tax years. This can be a particularly good idea if your annual earnings are near an income tax band, where receiving a lump sum interest payment would push you up into a higher band. If this happened, two things happen simultaneously, which would mean you'd be significantly worse off...

-

Your PSA would plummet (from £1,000 to £500 if you moved from a basic-rate taxpayer to higher-rate, or from £500 to £0 if you moved from higher to additional). So you'll pay tax on much more of your interest.

-

The tax rate you do pay on (a portion of) your interest increases. It'll double from 20% to 40% if you move from a basic-rate taxpayer to a higher-rate, or from 40% to 45% if you moved from higher to additional).

However, there are times where it could be advantageous to have all your interest paid at the end of a fix, for example, if you're retiring and would then become a lower taxpayer when you receive the interest.

How do I know when my interest is accessible?

It's complex, so check with your savings provider about when you can access the cash, then call HM Revenue & Customs on 0300 200 3300 (call charges may apply) so it can help you declare the income for tax purposes in the right year, if you need to.

It's also a good idea to get independent tax advice, as there are so many variables and what you do and don't pay tax on will depend on other savings and income you have. See how to find a financial adviser.

How much interest will I earn?

Use our nifty Savings Calculator to find out. Simply put in the rate, how much you'll save and how long for and it'll tell you how much you'll earn.

We also have a Regular Savings Calculator – it'll tell you how much you'll earn by drip-feeding into a top regular saver.

Do you pay tax on introductory cash bonuses?

Cashback bonuses are not treated as savings interest income, so are not subject to the same tax. This means if you receive a cash bonus (eg, via a savings platform), it won't count towards your personal savings allowance, and if you've already exceeded your allowance or are an additional rate taxpayer, it won't be taxed.

How do I complain about my savings provider?

If your savings provider has given you the incorrect interest rate, or you haven't received your interest at all, then you don't have to suffer in silence. It's always worth trying to call your provider first to see if it can help, but if not... you can use free complaints tool Resolver.

The tool helps you manage your complaint, and if the company doesn't play ball, it also helps you escalate your complaint to the free Financial Ombudsman Service.

Can I open an account through Power of Attorney?

Not all providers will let you open a new account on another person's behalf through Power of Attorney. For those that do, in most cases, you will need to contact the provider's customer support line to open a new Power of Attorney account as well as provide relevant documentation.

We have listed below some providers who consistently appear on our savings guides who explicitly allow new accounts through Power of Attorney. Take a look at some of these providers and compare the rates to the ones in the tables above to get as close to a competitive rate as possible.

If you found an account you would like to open on someone else's behalf, try searching the FAQs for a specific Power of Attorney page or ring the provider's customer support line. Note that some providers have stipulations such as requiring sole signatories.

These providers DO let you open a new account through Power of Attorney:

For full information on registering a Power of Attorney with your bank, or opening new accounts on behalf of a donor, see our guide Which bank is best if you have Power of Attorney?

What are green savings? Are they any good?

Green savings do exist, though you'll usually need to accept a much lower rate of interest, so there's usually a trade-off between interest and green credentials.

As a MoneySaving website, the most important thing for us is rate, so we always include accounts with the highest interest rates in each category in this guide, regardless of which bank or building society offers them.

In some cases, the best buys can change several times a day, and we don't have the resources to forensically check each savings provider to see what it is (and isn't) invested in, or what lending it uses savings balances to fund.

Yet if green savings are important to you, we have a separate Green savings guide, where we do look at the banks and building societies that promise to help the environment or to use your savings to help fund green initiatives.

We also have a broader Ethical banking guide, which provides a good starting point if you're looking for an account that backs good causes, or at least avoids 'bad' ones

Are there savings accounts designed for my business?

If you have a business current account, the chances are it pays no (or very little) interest. So any businesses with cash stored, even just to pay the tax bill, are missing out on interest.

If you're a sole trader, you'll likely to be able to save the business's cash in a personal savings account. It's best to do this, as you get the best rates. But if you've a limited company, then you'll need to use a specially designed business savings account.

How do savings providers make money?

Deposited cash can provide banks with a variety of pathways for making money, including generating interest by holding reserves with the Bank of England, through partnerships and by offering loans at higher interest rates than those they give to savers. For more info, we've a full guide on How savings providers make money.

Does inflation matter?

To really know how well your savings are doing, you have to look at it compared to the rate of inflation. Inflation is the measure of the rate at which prices increase, so if savings don't beat inflation after tax, they're losing you money.

Are your savings 'losings'? (Spoiler: for many, yes)

A savings account that pays less than the rate of inflation is eroding your wealth. Big banks often pay no (or very little) interest on their standard savings accounts, which many linger on, thinking it's not worth the hassle of moving their savings elsewhere. In which case your savings are 'losings'.

Inflation has been volatile in recent years, though it's come down massively from the highs of 2021-2023, so it's now absolutely possible to find savings that beat inflation.

Here's an example using simple numbers of how inflation and interest interact...

-

Imagine inflation is 10%. Things costing £1 this year will then cost £1.10 next year.

-

You have £1 in a savings account at 5% interest. By next year, it will have grown to £1.05.

-

So, saving has reduced your spending power by 5p per £1. It's a 'losings' account, not a savings account.

What about deflation?

Of course, sometimes prices drop – as happened in 2009 – and you get negative inflation, known as deflation. This can sometimes be a positive for savers.

-

Imagine inflation is minus 2%. Things costing £1 this year will then cost 98p next year.

-

You have £1 in a savings account. The interest rate has fallen to 1%. Despite the lower rate, by next year your savings will have grown to £1.01.

-

So, saving has increased your spending power by 3p per £1. Even though the interest rate has plummeted, you're actually better off.

This has remarkable consequences. Far too many have a concrete savings mindset that shouts: "Don't spend your capital!" Yet in a deflationary environment that's too rigid, anyone living off savings interest would face huge cuts in their income, and not spending capital would actually be penalising yourself.

Personal rates of inflation do vary, yet if you're experiencing deflation and need to spend from your savings pot, you can do so without hurting your savings pile. Take the capital out at the rate of deflation and you're not losing anything, as your purchasing power is retained.

Share this guide?