Martin Lewis: The Augar report heralds the end of student 'loans'

The student finance system has long been broken. Today the Government-commissioned Augar report on further and higher education is released, including detailed recommendations to change student finance in England. During the consultation process, I twice met Philip Augar to push for fairness and transparency in the system, and MSE's Campaigns team submitted a formal response.

This is an editorial comment from MSE founder Martin Lewis. Read the full Augar report on the Gov.uk website.

Augar's student finance changes in a nutshell…

Thankfully, unlike most politicians, Augar and his committee do actually understand how student finance works, and he's produced a cohesive plan based on his and the Government's set aims.

I'm happy that a few of his proposals are specifically based and sometimes attributed to my and MSE's suggestions. These include the fact that there won't be any retrospective changes – all will apply to new starters in the 2021/22 academic year; that the parental contribution should be explicit, not hidden; and crucially, Augar has accepted that we should stop using the divisive, damaging and disingenuous language of debt, and rename this a 'student contribution system'. Yet that doesn't mean I agree with all the panel's recommendations.

The irony is that what'll likely be his two most popular proposals – to cut tuition fees and reintroduce student grants from 2021/22 – counter-intuitively actually make the system more regressive than the current one.

That's because they both disproportionately help higher-earning graduates – who are the only ones who repay what they borrowed in full. For most students from lower-income families, the benefit will be primarily psychological as it's based on widespread misunderstandings – yet reducing the psychological deterrent is important in its own right.

Two really big changes may well slip under the radar. The proposal to lower the repayment threshold (the income level at which repayments begin) will increase what graduates pay each month. Combined with the substantial elongation of the repayment period from 30 to 40 years, this means many graduates will repay more, for far longer, substantially increasing the total cost.

Ultimately, this is all happening because one of Augar's aims is to rebalance the cost of education back toward the individual and away from the taxpayer, and his notes suggest the changes will do that.

Yet a brief summary doesn't do this justice. So if you've time, below I've bashed out a quick analysis of the Augur report's main changes and the personal finance consequences (rather than the cost to the state/taxpayer).

I'll lead on those which are a direct response to our (MSE and my) work. Though these are still proposals, with the UK's current political disarray, who knows whether they'll be put into place.

Student loans should be renamed a 'student contribution system'

Student loans are a misnomer. So it's with relief that the Augar report notes our call to change the name (see my Student loans are misnamed blog) and recommends the change happens.

The suggested new name of a 'student contribution system' is far more descriptive of the practical reality than the current language of debt.

Calling it a debt is mostly misleading, often dangerous and leads to people making the wrong decisions as we explained in our recent redesign of the student loan statement with the Russell Group.

In reality, what you repay both each year and in total depends far more on what you earn after university (currently 9% of everything over £25,725 for 30 years) than your initial borrowing. In fact, as is acknowledged in the report, most people currently pay that for the whole 30 years. This means for most it works more akin to a limited-term graduate tax.

The exact picture of how Augur's proposed new system will work when all the other changes are put in place remains to be seen. It's certain that more people will repay within the new 40-year term, but regardless, for most it will still act like a very long-term increased tax on income.

For clarity, as the renaming hasn't happened, I will still refer to this as a loan for the rest of the piece.

The parental contribution should be explicit

I've long campaigned to raise awareness of the hidden parental contribution system involved for university maintenance (living costs) loans for the under 25s. When giving evidence to Augar I argued that if the system must be kept, at the very least these contributions should be overt (see my Hidden parental contribution blog).

Maintenance loans are means-tested based upon family income – for most, a proxy for parental income. Yet parents are not told that their children's loans will be smaller as a result of this, nor that the system implicitly expects them to fill the gap.

The result, according to the report, is that only 15% of parents actually do give their offspring the expected amount or more. While some of this will be due to affordability issues, much will be due to the terrible way this contribution is communicated. This results in a far bigger practical issue for many students than tuition fees – and leads to many family arguments.

Thankfully, Augar has supported our suggestion that the Student Loans Company starts making this contribution explicit. While it won't make the contribution easier for parents to afford, it should aid transparency and hopefully reduce strife.

Tuition fees to drop to £7,500 – the primary beneficiaries are the highest-earning graduates

The report proposes maximum tuition fees should be dropped from £9,250/yr to £7,500/yr. Universities will then be able to apply for a direct Government grant for the rest, for courses deemed to be ones worth state support.

This will have psychological benefits as it lowers the debt. But if you lower tuition fees within the current system, only those who'd clear their debt before it wipes will benefit. And as repayments depend on earnings, that usually means the highest-earning graduates.

For more explanation, see my past Why cutting tuition fees only helps rich graduates blog (though the bit in there about it hurting poorer students is mitigated by the additional Government grant suggestion).

Maintenance grants to be reintroduced for those from lower-income households – a psychological aid

Those from families with incomes under about £43,000 will see some of their maintenance (living costs) loan replaced by a non-repayable grant. A rough suggestion is the maximum grant will be for those from homes with incomes under £25,000, who will get £3,000. It's also proposed loans and grants will also be available to those in further education, not just higher education.

While I don't object to the change in its own right, the prime practical beneficiaries of this policy will be higher-earning graduates from lower-earning backgrounds.

In reality, this policy is targeted to fix a perception problem (as explained when grants were cut) due to the constant myths about student finance. Many from non-traditional university families worry greatly about the level of 'debt'. Indeed the 'debt' is greatest for those from low-income families as they get larger maintenance loans. So switching to a grant will look like a big change.

Yet in terms of the practical impact on people's pockets, you only gain from the switch from loan to grant if you'd have repaid all, or nearly all, of your loan before it wipes. And again, those who'll do so are primarily higher-earning graduates.

As this won't lower costs for that many people, it is likely to be a rather cheap change for the Government (coupled with the fact that the proposal involves marginally reducing the maximum maintenance loan too), so on balance it may be that's a price worth paying to change perceptions.

Repayments to be increased by £180/yr, as the repayment threshold is dropped

Current students in England and Wales (on what's called Plan 2 loans) will repay 9% of everything they earn above £25,725. That threshold is set to rise with average earnings.

Augar proposes new starters in 2021/22 will be on what I guess will be called 'Plan 3' loans, with a lower repayment threshold based on average (median) earnings. If done today the report says the threshold would be £23,000, though by the time it is in place it will likely have risen to around £25,000 (however, by then the Plan 2 threshold will have further risen too).

The change means both that people will start repaying with lower earnings, and that all those who are repaying will contribute an extra £15 a month – so £180 a year – year after year.

The loan will wipe after 40, not 30, years – substantially increasing the total repayment for many

For current students, the loan is wiped after 30 years. The Augar report proposes extending that to 40 years. As most people don't clear their loan in full within the current 30 years, extending the life of the loan means repaying for far longer, and a substantially increased total repayment.

While more people will clear the loan in full due to the new, longer repayment period (and lower tuition fees), if implemented the majority of students will need to come to terms with the fact that they will now have their income reduced by 9% for all but the tail end of their working lives.

The total repayment is to be capped at 1.2 times the original loan (in real terms)

This is an innovative proposal. In effect it means for every £10,000 of loan, the most you will have to pay back is £12,000 in real terms. 'Real terms' means inflation is factored out, so while the cash amount you repay may be far higher than 20% more, you won't pay more than that in current prices.

One of the reasons for doing this is that a current quirk of the system means that while in general the more you earn, the more you repay, there is an exception for extremely high earners. They can end up repaying substantially less because they repay so quickly that less interest accrues. The cap on total repayments means it is less likely that high-earning graduates repay more than extremely high-earning graduates.

This isn't just about those at the top end though. Anyone who borrows less, on shorter and cheaper courses with lower maintenance, is protected too. Currently, mid-earners with lower borrowing can end up paying quite a bit more than they borrowed because they are clearing the loan slowly.

The interest while studying will be cut to the rate of inflation – a principled change even if the impact isn't huge

Currently, the interest rate while studying is set at inflation (RPI) + 3% – the same rate as higher earners after graduation. The proposal is to lower it to just the rate of inflation – the same as the lowest earners after graduation.

In practice, for most people who take many years to repay, the impact is either non-existent, as not all the interest is cleared, or pretty small.

However, the principle here that students should not be charged any real interest (ie, above inflation interest) while they are studying is decent.

It also has the advantage that it means people who are debating whether to take a loan can take it at no real cost while studying, then decide whether they should pay it off after studying.

Eg, some parents use their emergency savings – or worse, even take commercial loans to pay their offspring's tuition fees. Some of this could be wasted cash if the student isn't a high earner and wouldn't need to repay. Under the new system, there's less cost to a 'take the loan and wait and see what you'll start earning afterwards' attitude.

None of these changes are retrospective – current students/graduates will remain on the current system

Those who have watched my previous explosive reactions to student loans, especially those adding costs to graduates, (eg, hiring lawyers to investigate a judicial review) may be surprised at my relatively calm reaction to these changes.

The reason is simple. I've repeatedly made it plain, both in this consultation and before, that changes to a future system are a legitimate political choice, even if I disagree with them. Yet negative retrospective changes, which would in any other circumstances be a contract breach, go against natural justice – so I would fight that tooth and nail. We pushed hard for no retrospective change and the Augar commission has agreed to that, so all these changes are proposed for new starters from 2021/22.

The only exception is the total cap on repayments, which Augar suggests should come in sooner. As the only possible effect of that is to reduce the amount some pay, that's not something I see as a negative change.

While the system will still be progressive, the proposals make it more regressive, ie, they benefit higher-earning graduates more

Overall, the student finance system is progressive – a no-win, no-fee system – meaning those who earn more after university will repay more. But these changes – compared to the current system – are regressive, meaning they disproportionately help higher-earning graduates. This is due to a number of reasons (explained in detail above).

-

Lower fees in the main only help cut repayments for higher-earning graduates.

-

Giving maintenance grants instead of loans only reduces the repayments for higher earners.

-

The total cost cap of 1.2 times the original loan mostly helps higher earners.

-

The reduction in the repayment threshold means everyone pays more in by an equal amount, and means more lower earners have to repay.

-

Increasing the term of the loan to 40 years means lower earners repay for longer, while the highest earners have already paid off their loans.

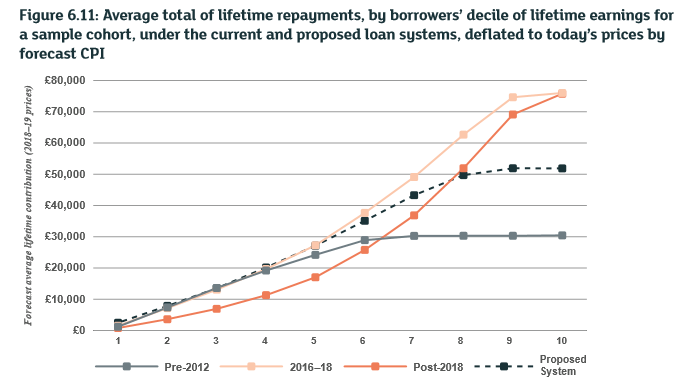

This is a symptom of trying to ensure more graduates repay their loans in full. In fact, the report itself shows the impact of this, which you can see in graph 6.11 from page 180 of the report (pictured below). However, the report's charts do indicate that the burden is more similar to earlier versions of the student finance system.

A warning to future prime ministers – cherry picking is dangerous

While the report is not what I would've suggested, Philip Augar has shown he understands the system. He has constructed a holistic, cohesive plan that changes the student loan landscape to achieve a set of aims.

This report was written for Theresa May. Yet she won't be in office to enact it. One danger is that a future PM cherry picks some recommendations without realising they are interconnected (eg, cutting tuition fees without giving universities the extra grant – which would hit the quality of education). That could result in substantial unintended consequences.

Martin Lewis is the founder of MoneySavingExpert.com.

Share this guide?

Latest weekly email

Latest weekly email

Clever ways to calculate your finances