How the starting rate for savings works

How to get tax-free interest if you earn under £18,570

If you earn less than £18,570 a year from earned income and savings combined, then all your interest from those savings could be tax-free. This is primarily due to what’s called the 'starting rate for savings' which you get on top of your 'personal savings allowance'. It can be complex, so let us take you through it.

There are three tax-free allowances for those on lower incomes...

If you earn a decent amount of interest on your savings, and you have a low income from work or from your pension, there are three allowances you need to understand to see how you’re taxed...

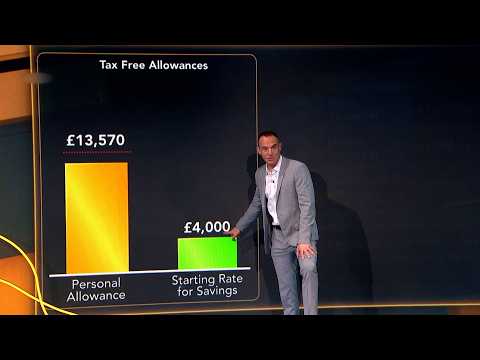

Your personal allowance. This is the amount you can earn, whether from work or savings interest or owt else, and not have to pay income tax.

For most people this allowance is £12,570 (for 2026/27), though it can be higher or lower.

Whatever it is, this is the base point for the other allowances. For example, if yours is higher because you get the additional personal allowance for being blind, then everything else is on top of that (though we’re going to stick with the typical £12,570 in our examples).

A £5,000 starting rate for savings. Here those on lower incomes get an extra tax-free allowance of up to £5,000 for their savings.

- If your income from pension or work is under the personal allowance (£12,570), you get the full £5,000, meaning you can earn up to five grand in savings interest without being taxed.

- If your income from pension or work is above the personal allowance (£12,570), you lose £1 of the £5,000 starting rate for savings for each £1 you earn above the personal allowance.

- If your income from pension or work is £17,570 or more. You don’t get any of the £5,000 starting rate for savings.

Your personal savings allowance. This is worth up to £1,000. The personal savings allowance (PSA) means everyone who pays basic 20% rate tax (so those who earn more than the £12,570 personal tax allowance but less than the £50,270/year limit for the higher rate of tax) can earn £1,000/year in savings interest before paying any tax on it.

This is added on top of the £5,000 starting savings rate. So, if you're on a low income, you're able to earn up to £5,000 savings interest without paying tax but you'll also pay no tax on the next £1,000 of savings interest – using up your personal savings allowance.

Watch: Martin Lewis explains the starting rate for savings

If you earn less than £18,570 a year from earned income and savings combined, then all your interest from those savings could be tax-free. This Martin Lewis explains how it all works.

From The Martin Lewis Money Show Live on Tuesday 10 March 2026, courtesy of ITV. All rights reserved. Watch the full episode on ITVX.

So some can have up to £18,570 tax free...

That's because you get your personal allowance before you start to pay income tax (£12,570), plus the starting rate for savings (up to £5,000) and the personal savings allowance (£1,000) all in combination.

How this might work in practice...

Chris: Earns £14,500 from work, has £2,500 of savings income

Chris will pay £386 in tax, all on his income from work. This is because he earns £1,930 more than his personal tax allowance of £12,570.

However, all his savings interest will be tax-free, as it's covered by the starting savings rate.

As Chris earns more than £12,570, his income from work starts to eat in to his £5,000 starting savings rate allowance. He loses £1 of starting savings allowance for every £1 he earns over his personal allowance, so he's left with £3,070 (£5,000 to £1,930) of his starting savings allowance.

As this £3,070 more than covers his £2,500 interest, he doesn't owe any tax on it.

Cheryl: No income from work, has £20,000 of savings income

In this scenario, Cheryl will need to pay tax of just £286. As she has no earned income, the savings interest is mostly covered by a combination of allowances:

Personal allowance – the first £12,570 is tax-free

Starting savings rate – the next £5,000 is tax-free, so now £17,570 of the interest income is taxed at 0%

Personal savings allowance – means the next £1,000 is tax-free, so £18,570 is taxed at 0%.

This leaves Cheryl with £1,430 of savings income which she will need to pay tax on. As she has no other income, this will be charged at the basic 20% rate, so she'll pay £286 in tax.

Hannah: Earns £35,000 from work, has £5,000 of savings income

Hannah will pay tax of £800 on her savings interest.

The first £12,570 of her income from work is tax free, but she'll pay basic-rate 20% tax on the amount above that. As she earns more than £17,570, there's no starting rate for savings available to her.

However, as a basic-rate taxpayer, she does get a personal savings allowance of £1,000, which covers some of her interest. However, the remaining interest of £4,000 will be taxed at 20%, meaning she'll pay £800 to HMRC, on top of the tax she pays on her salary (though, as we're MSE, we'd suggest she shelters some of her savings in an ISA, legally cutting her tax bill).

How do I pay tax I owe on savings interest?

Your bank or building society will pay all savings interest due to you gross (without tax taken off the amount). It'll then report the amount it's paid you to HM Revenue & Customs each year.

HMRC says that if you do self-assessment, you need to report any interest that's eligible to be taxed on that form each year. It'll then work out if you owe it any tax.

If you don't do self-assessment, any tax you owe on interest will be paid through changes to your tax code. So you'll get a lower personal allowance for income tax to pay it. HMRC will look at how much you got in savings interest last year and base your tax code next year on that if you went over your personal savings allowance.

If you've had a tax code change in the past and are now earning less interest than your PSA, you'll need to contact HMRC as it will need to adjust your 2026/27 tax code to be correct.

You can call it on 0300 200 3300 or go online to your personal tax account – go to 'check your income tax' and then 'tell us about a change'.

If you've paid too much tax on savings interest in previous years, you can reclaim it. Either fill in an R40 form to send to HM Revenue & Customs, or you can reclaim through the self-assessment tax system if you fill that in anyway.

Coming in April 2027: Savings tax rates will rise

Savings aren't taxed, but the interest on them is. If you do pay tax on your savings interest (ie, you’ve used up your allowances), the rate you pay will increase by 2% from April 2027. Here's the new rates:

Basic-rate taxpayers: Savings 22% (up from 20%)

Higher-rate taxpayers: Savings 42% (up from 40%)

Top-rate taxpayers: Savings 47% (up from 45%)

This doesn’t change the value of the personal allowance, starting rate for savings, or personal savings allowance – but anything you earn above those allowances will be taxed slightly more heavily from April 2027. Read more about on how tax on savings works.

Share this guide?