We've all been failed. Mortgages across the country are being overpriced – a ticking time bomb ready to blight the finances of millions. And whether it's lack of political will or clout, nowt's being done to stop it.Subtract base rate and lenders are effectively charging 4 percentage points more than a year ago creating a £300-a-MONTH cost per £100,000 of mortgage.

While many don't realise there have been rate rises – given 5% mortgages still sound pretty cheap – look at the bigger picture.

To say UK interest rates are low right now is a bit like saying expenses caused MPs a small PR issue. Interest rates aren't low, they're currently limboing 1.5 percentage points beneath the recorded 200-year historic low. The Bank of England's reason for slashing rates was to stimulate the economy, yet lenders' puckish response is clogging our nation's financial arteries. While, as I'll explain later, you can improve matter for yourself, it's approaching time for action from Westminster. The Evidence I must admit a wee glee of nerdish frisson here, as it's time to play with the stats.

-

October 2008. Base rate: 5%. Cheapest 5-year fix: 5.49%

-

October 2009. Base rate: 0.5%. Cheapest 5-year fix: 4.99%

Stark reading! While base rates plunged by 4.5 percentage points, mortgage rates have barely wobbled, dropping just half a point. So while the margin over base rate was 0.5% points it's now a staggering 4.5. Or phrasing the numbers more viciously, mortgages were 10% higher than the base rate; now they're 900% higher and fees are higher now too. Yet I'm being slightly disingenuous; I suspect any mortgage brokers reading this will be yelling that fixed rates don't actually follow base rates. Their funding's more closely associated with swap rates which, in simple terms, are the City's view on interest rates over a set period.For variety, now let's switch to two year fixes. A year ago they were 6.3% while typical 2-year swap rates stood at 5.3%, a decent but probably fair-ish margin. Now the gap's become a yawning gulf: typical fixes are 5.1% while swaps are at 2.1%.

The table (provided by Moneyfacts) highlights this:

Part of the reason for margins this wide is the huge drop in the volume of mortgages, a classic lack of demand – due to more stringent criteria and the slowing remortgage market. Yet it's still a massive hidden rate rise. Of course, there are some winners: the few with pre-base rate nosedive trackers are probably still gleefully dancing around their homes.

However, new mortgage hunters can't snoop out such glory rates. Trackers now average 3 percentage points above base rates, where once it was half a point.

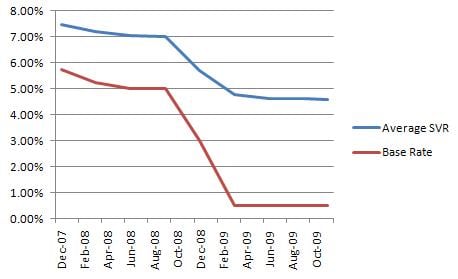

Evaporating equity Perhaps the biggest scandal, though, isn't special-offer discount or trackers; it's the standard variable rates (SVR) you automatically flick to when these end as they are also extremely high in relation to base rate. Once the default 'flee from' option as they were exorbitantly expensive, it's not just those in negative equity who now have nowhere cheaper to go and are forced to stick with their SVR. Now the spectre of what I call evaporating equity is hitting many.This affliction means you can't get a new mortgage deal due to a double-whammy…

-

Tougher LTV limits. Pre-credit crunch, loan-to-value (LTV) ratios of over 100% were possible (borrowing more than your home's value) and competitive rates were available at 95% LTV. Now to get a decent deal, you need borrow less than 75% of your home's worth and this cuts huge swathes of existing mortgage holders out.

-

House price decline. The 'value' bit of LTVs means current house price values, so where prices have plummeted, people's LTVs have worsened. Many once in that competitive sub-75% zone may aren't any more.

Yet even with so many on these standard rates, look what’s happened to them (table provided by Moneyfacts):

The average gap over base rate used to be around 2 percentage points, and when rates were first slashed government pressure to keep it there was partially successful, yet now the gap's a mammoth 4 percentage points, even though the bank's cost of borrowing's reduced since.Ticking timebomb

The paradox is that while mortgage rates have been relatively unresponsive to falling base rates, it's likely they'll be over-stimulated when they rise. Millions are locked into standard rates or high-margin trackers, or due to be when their current deal ends. When rates finally turn and start to rise, it'll be like a smash and grab brick through windows. Imagine base rate return to last year's historically still quite low 5%, someone with a £200,000 interest-only mortgage tracker would see their payment explode from £500 to £1,330-a-month. For many on top of the recession-led financial freeze, that's castastrophically unaffordable. Rising bills don't simply flick back into place like elastic. The pain of increased costs out-balance the joy from when they fell, as people have rejigged their finances around new lower rates and locked into other commitments. So waiting to administer treatment when rates rise will be too late. This mortgage margin timebomb's growing now; so we need Government pressure's on the banks we own at least, to defuse it now.

If not, prepare for the potential knock-on effect of even harder income squeezes. DIY help

You can't bet on any government laying a golden mortgage egg anytime soon: your best bet is to crack it yourself.

-

Bagsie a cheap fix for insurance. Many with deals ending ask if it's worth fixing now to future proof against rate rises, even at a higher cost than their standard variable rate. A half way house is use the little known option of paying a fee to book a current fix to start 3-6 months ahead. Then if rates or future fix prices rise you can use this, if not, simply don't use it and lose the fee.

-

Repay your mortgage with savings. Reducing outstanding debt means you're less at mercy from mortgage rate rises, and helps lower your LTV, possibly meaning access to more competitive deals.

The financial mathematics to decide if it's worth it are simple (assuming there are no overpayment penalties)... if your after-tax savings rate's lower than your mortgage rate, pay it off. For example, if you used £1,000 of savings currently earning a decent 2% after-tax to repay a 5% mortgage you're £30 a year up.

Though if you've other more expensive debts, pay those off first. Plus keep an emergency fund, as with most mortgages, overpayments can't be borrowed back, so ensure you've money to keep paying all bills and future mortgage commitments. For more and a special calc see the Should I repay my mortgage?guide.

-

Build a war chest. If you're on a super-cheap rate now and haven't got savings, put money aside in case rates rise. This way, you'll avoid mortgage payment default.

-

Get a mortgage broker. Once they salivated for your business, now lenders today hawk their hands over deals like schoolkids preventing their neighbour copying. So have a mortgage broker on call to speedily grab short lived deals, preferably one who's 'whole-of-market', meaning it must look at all the mortgages available to it. See the mortgage broker guide.

-

Check FSA best-buy tables. Some lenders deliberately pump out 'direct only' deals which can't be accessed by brokers. They should appear on www.fsa.gov.uk/tables though, so check that and if it looks good ask your broker to crunch the numbers.

-

Should you ditch your fix? It's a common question from those on high fixes gawping at lucky neighbours' dirt-cheap trackers. Yet for most, exit penalties added to high current new mortgage rates mean you're UNLIKELY to save any cash – plus you lose the fix's security.

Though if you do want to do the numbers, see the Ditch my fix? calculator.

Further reading/Key Links

Mortgage cost-cutting guides: The Remortgage guide, Mortgage haggling, Cheap mortgage finding, Ditch my fix?

Share this guide?

Latest weekly email

Latest weekly email

Clever ways to calculate your finances