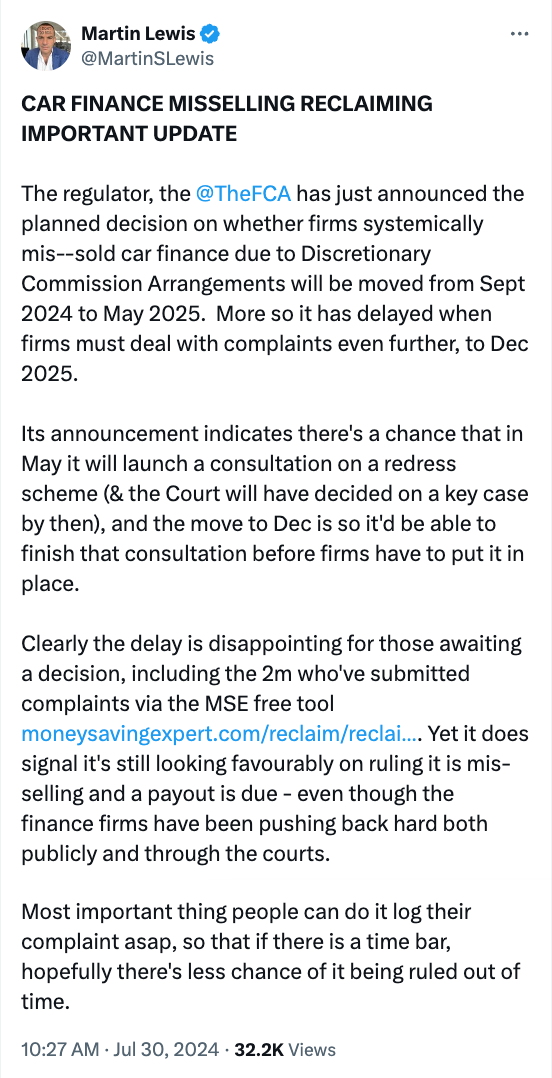

Martin Lewis: Car finance mis-selling update – complaint decisions delayed but redress payments now "more likely"

The outcome of a major investigation into hidden, unfair car finance commission will be pushed back from September 2024 to May 2025, it's been announced. But the regulator behind the probe has told MoneySavingExpert.com founder Martin Lewis that payouts to drivers are now "more likely". Check if you could be due £1,000s back using our FREE car finance reclaim guide and tool.

The regulator, the Financial Conduct Authority (FCA), said the delay would give it time to "analyse the data collected from firms". It'll also assess the outcome of a legal challenge brought by Barclays after the Financial Ombudsman Service ruled that the lender had treated customers unfairly over their car finance agreements.

Martin Lewis: 'The delay is disappointing – but could be a good signal'

MoneySavingExpert.com (MSE) founder Martin Lewis shared his view of the delay and what it means for those affected on X (formerly Twitter):

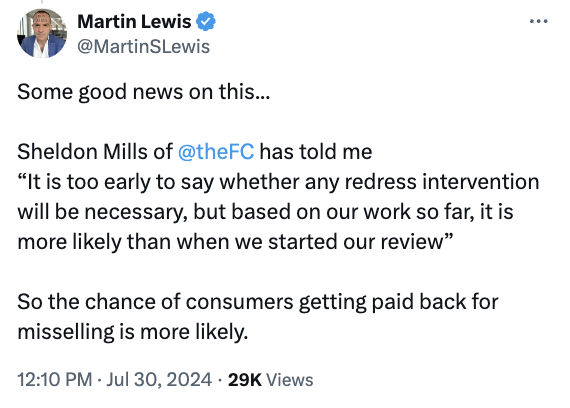

Payouts are now "more likely", regulator tells Martin

In a follow-up post, Martin shared that one of the FCA's executive directors had confirmed redress payments are now "more likely":

A timeline of the FCA's car finance mis-selling investigation

In January 2021, the FCA banned 'discretionary commission agreements' (DCA). This stopped lenders allowing brokers, including car dealers, to increase interest rates on car finance in order to get more commission.

On 11 January 2024, the FCA launched a major investigation into the practice. It also paused the eight-week deadline that firms usually have to provide a response to complaints about DCAs. It was set to report its findings on 25 September 2024, but as Martin explains above, this deadline has now been extended. The FCA has given two reasons for this:

-

Many firms have struggled to provide the data needed in the requested time. Reasons for this included firms not keeping older data, and data being stored on multiple systems or being spread between lenders and brokers, the FCA said.

-

Barclays Partner Finance has brought a legal challenge after the Financial Ombudsman Service ruled that the lender had treated customers unfairly over DCAs. The FCA said the outcome of this case, which is expected to take place in the autumn, could influence the next steps in its investigation.

As a result, the FCA now plans to set out its findings by the end of May 2025 – so that's when we should find out whether those who've made complaints are due any money back.

Firms have also now been given until at least 4 December 2025 to give you a final response if you've made or make a complaint. The FCA says this allows time for it to confirm how firms will start providing redress to customers if it decides they need to. However, if the regulator decides that firms don't need to pay out, it could ask firms to start dealing with complaints again as normal.

What you need to know about car finance commission mis-selling

You can find all the relevant info in our Car finance reclaim guide, but here's what's happening at a glance:

-

This is for people who bought a car, van, camper van or motorbike using Personal Contract Purchase or Higher Purchase deals (not leasing) for primarily personal use between April 2007 and 28 January 2021.

-

Martin believes it is unlikely the FCA would've launched such a huge public investigation unless it had strong evidence of systemic mis-selling.

Yet he says until the FCA reports its findings, nothing is certain. However, as one big risk is that there is a time bar placed on complaints, it's important to log your complaint as soon as possible, to avoid the risk of being timed out.

-

There is no need to use a no-win, no-fee claims firm.

With the free MSE tool, you just answer a few questions on your car finance agreement (answers aren't recorded, so as not to inadvertently data-mine) and then the tool builds an email to request information on whether you had a DCA, then logs a complaint.

Share this guide?

Latest weekly email

Latest weekly email

Clever ways to calculate your finances