Pension need-to-knows

Key points for retirement saving

Saving for retirement is crucial. Many of us typically only work about 45 years out of an 85(ish)-year lifespan - so that work income needs to cover those non-working years. Pensions also have two big superpowers – tax relief means the Government tops up your pension pot and, if you're employed, your employer often must do the same, resulting in a 'hidden payrise'. We talk through what you should know.

Prefer to listen? Martin discusses pensions

In his spin-off BBC Not The Martin Lewis Podcast, Martin takes on subjects with the help of specialists. Here, he looks at pensions over two separate podcasts...

Listen to 'Pension need-knows' (July 2024) for free via... BBC Sounds | Apple | Spotify

Listen to 'How to take money from your pension' (July 2024) for free via...

BBC Sounds | Apple | Spotify

(transcripts available below)

Read a transcript of Martin's pension need-to-knows podcast

Martin Lewis: Hello, and welcome to the Not The Martin Lewis Podcast, which rather confusingly is an offshoot of my normal, The Martin Lewis Podcast, the difference? Well, there are some subjects that are outside my wheelhouse or I can't answer questions on due to regulations. So in this podcast, I'm joined by specialists, and I'm asking, not answering, the questions. Well, it's me, I might chip in with the odd note or two – and crucially, too, it's you who sets the agenda. It's all about getting answers to your questions.

And this week's part is all about starting and saving in a pension. And there's a lot of info for you, including how the pensions actually work, and what are they? Should you consolidate your pensions? How to start your first pension? How to get totally impartial free guidance. Stakeholder pensions versus nest versus SIPPs? How much to save in your pension? Can pension saving ever be too little? Or too late? And loads more? Just give it a listen. Play the theme tune.

Yes, welcome to this pensions podcast. What I really want to focus on today is private and company pensions. How'd you get one? What do you do when you when you've got one? And what decisions do you need to make? We will be doing another Not The Martin Lewis Podcast on how you take your pension money when at or near retirement. So this focus is all about building up your pension pot in whatever form.

Now I'm joined and delighted to be joined by Charlotte Jackson, who's head of guidance at the Money and Pensions Service, and Mihir Choughule, who's a wealth manager at Tideway Wealth. So, before we do anything else, you two have very different roles. And I think it's important that we understand them. Charlotte, you're all about guidance, Mihir. You're all about advice. What's guidance, Charlotte?

Charlotte: Guidance says we will tell you about the subject that you're interested in, we'll guide you through some of the things that you need to think about. But crucially, we won't tell you what to do. And we won't recommend products and services.

Martin:So you couldn't tell me you need to put your pension with X provider. But what you could tell me is the pros and cons of going with a stakeholder pension over a SIPP, or what the tax implications of putting money into your pension are. Everything to understand the bigger picture, but not the final decision. And the big advantage people have with you is you're free.

Charlotte: Yep we're free, independent, impartial. So when we don't hold any products or services, it's literally just about providing support to individuals as they're trying to think through those decisions.

Martin: So if you're listening, for me pensions is one of those lucky areas where you can get free one-on-one help if you don't know what you're doing. So see the podcast we're about to do as a good guide. But then it costs you absolutely nothing. You can call up the Money and Pensions Service. And you can get one-on-one pensions guidance. But there are some times especially if you're dealing with larger amounts of money that you actually want someone to help you through to the very end point of the process. And Mihir, that's where what you do comes into effect, isn't it?

Mihir: Yeah. So we will look at an individual circumstances, you know, personal and financial, as well as you know, what their objectives are, and what basically they want to do with that pot of money. And that's really where the advice part of it comes in, where, you know, we will sit down with you and talk you through all of the different options available to you.

Martin: And you'll talk products when you're saying this provider this amount of money, this type of investment.

Mihir: Yeah, yep. So we will give you a definitive not answer, but a more sort of more than sort of guidance. Ultimately, it's the individual decision at the end of the day, but we will sort of lead you to a particular direction.

Martin: And of course, you get paid for that. Well, listen, everybody at the Money and Pensions Service gets paid to but it's free to the to the user. Whereas if someone wants to come to you or come to an independent financial adviser specializing in pensions, that pay for it, how do they generally pay?

Mihir: It varies. So some sort of firms offer sort of an initial and ongoing fee. Some firms, like the one I work at, we offer just an ongoing fee. So I mean, the charging structure varies from firm to firm, but generally, you might have an initial or an ongoing fee.

Martin: How much money do people need to have for when they're starting to come into the independent financial adviser realm? Let's be really blunt about this. Because the truth is IFAs you've got to make a living, you're not going to deal with someone with a £5,000 pension pot.

Mihir: No. And honestly, like, if it's the £5,000 or a small sum like that, honestly, you don't need financial advice. It's about keeping it as cheap as possible and making sure that you're invested in the right funds.

Martin: And you can get the guidance from the Money and Pensions Service.

Mihir: Exactly.

Martin: So what type of level give us some rough guidance, give some rough advice kind of level.

Mihir: I would say if your pension or any other assets that are sort of valued at between £250,000 to £300,000 you should probably look at getting some sort of advice on those funds by.

Martin: That seems quite on the high side, I think there are certainly people out there who might be going at a lower level sort of £100,000. Charlotte, where are you?

Charlotte: Yeah. And, and it also depends on what type of products you have. Because if you have an older pension, so a defined benefit pension, then legislation requires you to take regulated financial advice. But people's lives can be quite complicated and messy, so pensions often don't sit in isolation. In our view, everybody would benefit from guidance on the topic and their significant percentage, also, going on to regulated financial advice is about helping equip people.

Martin: We are a bespoke podcast that tries to give people definitive. So I want some form of number from you of what type of level of pension funds you should be looking at. When you go for advice, give me something, I know you don't want to, but I'm pushing you.

Charlotte: I think if you are with somebody with a pot of say £150,000 or above, then you need to be really seriously thinking about it. But again, it depends on your individual circumstances, and what the types of products you're interested in. So people's lives are complicated. But the more you are looking at variation and flexibility, the more you should be considering taking advice.

Martin: So complex products, it might be even £75,000 pension fund and above, you might want to take a look at it.

Charlotte: Yeah.

Martin: Perfect. Right. So I'm going to do my little bit now before we come on to you doing the hard stuff, I just wanted to explain to everybody the basics of pensions, because there are lots of different categories. So the first big division is there's the state pension, and there's private and company pensions now with the state pension, generally, when you work, you build up National Insurance years, and each year that you work, you get more of those national insurance years that once you get to retirement age, you will get a payment from the state that goes into your pocket, depending on how many national insurance years you get. So, the current state pension age is 66. That's when you will start to get paid your state pension, but that number is going to go up to 67, and then up to 68. So it all depends on how old you are at the moment. But that's not what we're planning to talk about today.

Today is all about private and company pensions. Now these fall into two categories, defined benefits, and defined contributions. Let's do defined benefit first, which is more commonly termed a salary type scheme. So here you'll get a set percent of your final or average salary when you retire. And you'll earn that for each year of work. So you might get a 60th of your final salary for each year of work. So if you work at that place for 20 years, you would get a third of your final salary on retirement. Now, these are older types of schemes, they're few and far between now, they tended to used to be thought of as being absolutely gold-plated, the best out there. But there has been some breakdown in the way that they work. Why they're called defined benefits? Well, the amount that you get when you retire is what is defined, it is a percentage of your final salary.

Most people though, these days will be on defined contribution or money purchase pensions. This is where you save a pot of money. And that builds up and you use it when you retire. This applies to many workplace pensions now and all private pensions are money purchase. The pot size that you build up depends on the amount of money you put in it, and how much it grows. As simple as that. So for the vast majority of people deciding on a pension, you will be looking at money purchase a defined contribution, because it's the amount that you put in that you dictate the amount that you get out often depends on your investment returns. And that's where someone like Mihir comes in, because that he'll be telling you what to invest it in.

So, let's get into these questions. The first one comes from Twitter. It's Laura Davis, and it's a big wide one. If you're 45 and have no pension, what do you do? Charlotte? Where do you start?

Charlotte: Don't panic. That's the first thing. There's never too old to start looking at a pension. But there's obviously a wider set of things that you might want to consider. Are you employed? Are you able to save a little bit or not? Is there a workplace pension where your employer is contributing? What's your wider financial situation like. So at 45, we'd be saying have a look at going through we call it a midlife review. Look at all of those questions around your finances more broadly.

The more you can save the better. It's never too late – little and often.

Martin: It's never too late but the earlier you start, the better.

Charlotte: Totally.

Martin: So let's do the thing that scares the pants off absolutely everybody when I say it, so you no one does this what I'm about to say you will not do so do not panic, but it is this old equation. It's not particularly accurate, but it gives you a good sense. Who's the younger of you two? Mihir? You're the younger, aren't you? So, I'll ask you. So, you take your age, when you start putting in your pension, how old are you?

Mihir: I'm 30.

Martin: You're 30, you halve it 15. So, the equation says that you want to put 15% of your income, and that includes employer contribution into your pension for the rest of your life to have a pretty strong retirement fund. Very, very few people manage that. But the real lesson from that is the earlier you start, the better, because the more time your money has to grow, when it's in your pension, so nobody do that equation, they go, 'Oh my God, I'm never gonna do anything'. It's not about that. It's just a way of indicating to you that early is better, and the more you can catch up later. So we'll go back now to Laura's question – 45, and no pension – we'll assume that she can contribute, where and we're going to say, first place, if you're in work, use your workplace pension

Charlotte: Yeah, because you're in work you will not have to pay any fees or charges in the same as if you set up a personal pension, and your employer should be contributing to it. So under automatic enrolment, the employer is required to put you into a pension, you can decide to opt out, but actually, you will get benefits by your employer paying in most employers will contribute towards it, and you will get tax relief on anything that you save in there. So it's a really, really good deal to save into workplace pension if you can.

Martin: So right, let's just do this for a second. Auto enrolment means you will save into your workplace pension by default. If you're age 22 to 66, and you earn £10,000 a year, you are automatically opted in. Now, the minimum total amount is 8%, of what you earn. And the employer must contribute 3% to that. So, let's just do this really simply, let's imagine you are putting in £100 a month of your income. As a base minimum (assuming it's within the right criteria) your employer would need to add £60 on top. So, you're putting in £100, you're getting £160 in your pension.

But it gets better than that everybody. Because one of the big things about pensions – one of the whole things about pensions – is their tax wrapper, you get to put the money in from your pre-tax salary. Now this happens, whether you're self-employed doing it yourself, or whether you're employed, but will stick within the auto-enrolment system.

So, imagine you've put £100 in now. Because that comes from your pre-tax salary, your gross salary. If you're a basic rate taxpayer, you only lose £80 from your pay packet. So think about this for a second, you put £100 in, it's cost you £80, the employer's added £60 on top, so for your £80 going from your pay packet, you now have £160 – double it – going into your pension, if you're a higher rate taxpayer 40% taxpayer earning over 50 grand a year, well, then for you to put in £100 only costs you £60, you only lose £60 from your pay packet. So now you've paid £60, but you've got £160 going into your pension. And that is unbeatable gobsmacking tight rates. That's why pensions are powerful. Yes, the money is locked away until you're older until you're at retirement, but as a form of saving the tax benefit plus the employer contribution is unbeatable. So auto-enrolment. Absolutely the first thing you should look. And, just a tiny quick note. It's worth me saying if you're not opted in, because let's say you're aged 16 to 22, or 66 to 74, you won't be opted in, or you're earning between £6,240 a year and £10,000 a year. In those circumstances, you can say to your employer, I want to opt in, and they must allow you to opt in and they must contribute to your pension giving you the same as they would if you'd been automatically enrolled. So, Charlotte absolutely step number one, check if you're employed, is your employer giving you a pension, well it has to it has to by law, I shouldn't say check, if you're employed, that you're within the criteria to get the pension.

But we're going to imagine for Laura here because I want to use her as an example. She's not, she's self-employed now. So where does she start?

Charlotte: Well, you can set up a personal pension and there's a range of different types of things that you can do. So you can you can ask around in terms of banks building societies, pension providers, you'll see them advertised all of the large names. Nest, you can look to start up your own pension.

Martin: What is Nest?

Charlotte: Nest is the National Employee Savings Trust.

Martin: It's basically the default pension that are used. It's the big national one.

Charlotte: And they are set up to provide low-cost pension savings for the bulk of people so they are a good first place to start. Have a look and see if what they can offer is what you want.

Martin: Now you see people what I'm going to do now is give you a perfect example of the difference between guidance and advice. Charlotte can explain how things work and talk people through the tax things but she doesn't do products, Mihir, you do products, Laura's self-employed, let's say she wants to contribute £150 a month to her pension. Where would you start her?

Mihir: Well, I mean, I think the easiest place to start is your big pension providers. I think most of them have to.

Martin: Give us some names we're talking about, Aviva?

Mihir: Not even Aviva. I was thinking something like AJ Bell, Hargreaves Lansdown, things of that nature. I mean Aviva is obviously one of them, L&G is one of them.

Martin: So but Hargreaves and AJ Bell, they're SIPPs, aren't they? Your self-invested personal pension. So let's just run through, let's just get some definitions of the different major types of pensions. We'll start with a stakeholder pension, which is?

Charlotte: Which is where you have a very basic set of options available to you. And you can save into it and a narrower range of investment choices that you can pay in, you can normally delay pay, you can pause, but you're looking at a fairly straightforward savings vehicle with tax relief.

Martin: A simple, straightforward savings vehicle with capped charges, so you can't be charged a certain amount. But it's a type of standard pension.

Charlotte: It is.

Martin: The difference between a stakeholder and a standard pension is standard pensions don't have the cap charges, basically. And then a self-invested personal pension, a SIPP, Mihir?

Mihir: It's also a personal pension. But where it differs from a stakeholder is that the range of choices they do get in terms of funds is a lot higher than a stakeholder. And the onus really is on you to get an investment strategy that is suitable for you and your pension. But the charges then will be higher as well as compared to the stakeholder.

Martin: So this is why I sort of in my view, and you two are the professionals, someone who's starting a pension at 45, putting £150 a month I would be slightly nervous about them doing a set my guess is (and this is maybe because I know the type of people who ask me questions) that someone asking that question would be the someone goes, I know nothing about this stuff. I don't know what I'm doing. And SIPPs aren't really for that type of person, are they?

Mihir: It depends upon obviously the knowledge of the person who's investing it, but what they want to do and how much work they want to do. But I would counter that, Martin by saying, you know, stakeholders, obviously, are you know, the cost is a lot lower than the SIPP for example. But in terms of the investment options, if the investments, you know, if they don't perform at the end of the day, then you know, you're kind of losing out on a significant amount of growth there between 45. And whenever the person decides to retire.

Martin: Charlotte stakeholder versus SIPP for someone starting out?

Charlotte: I'd go for a stakeholder, SIPPs require a lot of work, they are more exotic, oftentimes of their investment choices, which is where, you know, we talk about higher rates of return. But those higher rates of potential return on those investments come with a much higher, typically higher level of risk. So if you aren't familiar with that investment choice, for example, we've had people phoning us up talking about truffle farming. Do you know about truffle farming is that really a good investment choice for you, we would say you have to be hands on and know what you're doing. And you're choosing to invest your hard-earned money into something that a lot of work on it.

Martin: For me, that is the difference. I think if you don't know what you're doing, you're scared and you just want capped charges, a relatively simple form of stakeholder a standard pension is probably for you. If you want to take control of your money, you want wide investment choice, you're going to follow the different investment options out there, you're going to get advice – so, you've got someone who could guide you through it – you probably want to go through a SIPP. So, we're here, just before we finish up on where self-employed people should be looking for their pension. Give us the names of a couple of stakeholders or easy places for those who don't want SIPPs to go for.

Mihir: Sure. I mean, two of the biggest ones are probably Aviva and L&G, I would say on the market. If you're looking for something more automated, then Wealthify as well.

Martin: It's not a stakeholder, but it's an easy form, isn't it? Correct?

Mihir: Yeah. So I would probably say these three, probably should be your first port of call for a stakeholder pension.

Martin: Brilliant. Thank you very much.

I'm going to move on to I think the biggest single pension question that we have had, and doesn't surprise me because I get it all the time. It's all about consolidation. So let's read a couple of them out. Would you say it's more beneficial to keep all of my different work pensions separate, or collate them into one pension pot to be managed together? That's from 'hustlingfun' on Twitter. And Rob O'Brien on Facebook says, I have about five workplace pensions, and my best putting them all together. So that to consolidate or not to consolidate.

Charlotte: With my slight OCD tendency, having things neat and tidy in one place is really attractive, but there is a big cautionary button there.

Martin: What's your big but there Charlotte?

Charlotte: The big but is have you need you need to know you're not giving anything up. And there are some really good reasons as to why you might not want to consolidate everything. So don't automatically jump in to say, I'm going to be neat and tidy and put it all in one pot. Ask some questions, keeping some separate is helpful sometimes.

Martin: So we can start by saying there's nothing wrong with being biased towards consolidating because it makes your life easier. What are the questions people should be asking before they do it?

Charlotte: The big ones, so going back to some of our early conversations about defined benefit, there are some types of pensions that have really valuable special features to them. And it might mean that you don't have very much money in it. But actually, it will bring you lots of other benefits. So things like, if you die, it would protect your spouse, for example, there may be special conditions, and that's often down in the devils in the detail. The other big but on there is, you may want to just have a final, you might want to have a little separate pots of money, because in the future, you might want to treat them differently. So again, when we come to thinking about what you do in retirement, having a couple of separate pots will enable you to maybe make a range of different options and treat them differently. And that can be really useful for tax purposes.

Martin: So some consolidation good – too much not. Now, just while we're on this. So you've given us things people should look at, but it sounds quite technical in the small print. Pension Wise, would they be able to identify those in different providers? Or is that something you need to go to advice for?

Charlotte: No, you can do both in Pension Wise, the Pension Wise appointments cover special features, although they're often in defined benefits schemes. So that's not the main purpose for Pension Wise appointment, that's obviously defined contribution, but our pension guidance services under money helper do and they specialize very much in looking at those technical details to be able to provide support to ask the right questions.

Martin: So somebody would be able to come and make an appointment and say, here are the five different places I have my pensions to I've set up myself and three of workplace pensions, and I'm considering consolidating them. Can you tell me for each of those schemes, whether it is a good idea or not to consolidate?

Charlotte: Because we don't give advice? We'd be very careful not to say.

Martin: OK I'll rephrase, can you tell me the pros and cons and consolidating for each of those schemes? And they would have scheme level knowledge?

Charlotte: Yes, more often than not. So the people that we employ are all industry experts, they've typically worked 10 plus years within the industry, so they know what to look for. And that's their job to make it easier for you because we know it's difficult. In some circumstances, what we'll say is, you need to ask your pension provider and they will help you articulate what it is you're asking them.

Martin: Yeah, Mihir. Where are you on consolidation?

Mihir: I think I'm broadly in agreement with Charlotte and things you have to consider. I think one of the things that wasn't mentioned is it really depends on what stage of your life that you're in. If you're accumulating any, let's say you're in your 20s, or your 30s, chances are the pension assets that you have, are probably not going to be too complicated. And esoteric, I would imagine. So consolidation probably makes sense – probably being the key word.

Martin: Yeah, we all know we're generalizing, you can't do it without knowing the details absolutely. So the younger you are, the simpler it is, the easier it is to consolidate.

Mihir: Yes. Whereas if you're in your 40s, 50s, 60s, and you're approaching or thinking about retirement, and the focus is on preservation, not just accumulation, then it probably might make sense to have two separate two, three, or however many separate pots that you want. So that each pot does separate things, essentially.

Martin: And is some of that age difference, because pensions have changed over the years, so there's complexity in older style pensions, but there won't be for some of those in their 30s – they're just not going to have that different complexity.

Mihir: Yeah, like, like the benefits that Charlotte mentioned, you know, some of these are protected and the individual to the scheme. So these were prevalent in the 70s and 80s, which, you know, people in their 20s, and 30s, just weren't around for them. So they just won't have access to them. So you know, 20 people in their 20s and 30s likely have much simpler arrangements.

Martin: You said, keeping a couple as you're getting their retirement. This is because what you may want to do with that money will change. And I actually know because we're going to do a programme with you, too, on how you take your money for retirement. We've got questions on that. So if that's coming into your head, do listen to the other Not The Martin Lewis Podcast programme on taking your pension. Well, we'll go through that in more detail. Next question is from Craig1983 from Twitter. It's about investments. He says my pensions tumbled in the past two years, when are they likely to return to their previous high and what factors impact them. So the first thing to say is nobody knows the answer to that. We don't. But what should you be looking at how it almost how do we think about our pension money because one of the problems if you track it every day, it's gonna give you a heart attack going up and down all the time. You have to look over the longer period don't you.

Mihir: Yeah, I think obviously, I mean, I won't go into the details of why it's gone down over two years, I'm sure people are aware of the general macroeconomic factors and things like that. But I think the key here is to make sure that you have a medium to long term investment strategy there. One that you're comfortable with, one that works for your objectives, and one that works for your circumstances, and one that you would be comfortable remaining in even withstanding market volatility. I think that is the key.

Martin: So this is something people find very difficult, let's just imagine you put, we'll call it £10,000, plucking a number out of the air, you put £10,000 in an investment, that investment – and a pension is just a tax wrapper, you're choosing investments to put inside it – it's just a good way to do that with tax, that investments dropped to £8,000. Now people tend to think there's a law of return, 'I will wait until it goes up to £10,000, until I'm going to, to deal with it. Whereas actually, philosophically, should people be more thinking I have £8,000, what I had before whether it's £6,000, before £10,000 is irrelevant. I have £8,000. Is this the best place for my £8,000? Not, I wait? Is a better way to go, isn't it?

Mihir: Yeah, I think so. I think firstly, the strategy should be outlined at the outset, taken into account, if you need that money at some point, and then the risk would be altered depending on whether you need access to that money in the next one or two years versus if you're happy to leave it there for the next five to 10 years. Those are two significantly different strategies. And I think, you know, depending on which sort of stage you're in, if it's sort of medium to longer term, I appreciate seeing sort of red on your investment portfolio is not pleasant, it's not pleasant for anyone. But if you know that you have 5/10 years to let that money recover before you need access to it, you really shouldn't panic and take a decision, which then impacts you over that period.

Martin: No, my view was less that you panic, because it's dropped to move it out. It's more that whatever amount of money you have whatever has happened in the past, the amount of money that's in your account is what you've got. And you should always just say, 'Is this the best place for that money?' Yeah, but look, we are terrible in this country with investing, we have no understanding. Generally,(many individuals do) of risk. You know, you contrast it to the states where everybody instantly tries to put far more money in stocks and shares rather than savings. I mean, some people blame me for this because I only ever talk about savings. I don't talk investing because investing is not my bag, I'll probably do Not The Martin Lewis Podcast on this at some point, because it's something that I need specialists in to talk about, but you're going to put your pension almost invariably is going to be an investment, it's going to go up at times it's going to go down at times. Think of it like a sine wave, if you remember it from school, the real question is, is the overall direction over a long period of time going upwards? That's what you want. The fact it's dropped over the last six months, doesn't necessarily matter. If it's dropped down over the last 10 years, that's a problem. But over six months, things will go up and down. So you just have to understand pensions are for the long term, not the short term. That's what it's all about, isn't it?

Charlotte: It is.

Martin: So we've got a caller on the line. Now it's Emma Torrance from Nottingham. Hello, Emma, what can we do for you? What's your question?

Emma: Hi, Martin, I've got some money that is invested on a platform in a SIPP. I used to have a financial adviser, and then I withdrew most of my money, mainly to pay off my mortgage when all the rates changed. But my SIPP was left on the platform. And very nicely, the adviser isn't charging me for any fees, but I can't put more in, take bits out I can either take all of it out or not. But I'm just wondering, should I move it into somewhere, you know, either into a pension? Or am I able to move it into a normal pension rather than a SIPP?

Martin: So Emma, I'm assuming you're over 55 At this point, if you've taken money out of your pension.

Emma: Yep. Yeah I'm 55.

Martin: So you're able to take the money out of your pension? Charlotte, let's come to you.

Charlotte: The first thing is, is looking at you saying that the adviser hasn't been charging you but obviously that's going to be a key question around taking your money out. So transferring it. So you shouldn't be able to look at transferring it into another form of pension but have a look at what's suitable for you. What are the options for you going forward in terms of the types of things you're going to want, in the future.

Martin: What are you going to want in the future? Let's try and dig into that. What should you be looking at?

Charlotte: So that's things around really thinking about what do you want your retirement to look like? How are you going to want to access that money because if you transfer your money into a different type of pension product, you want to make sure you've got the full range of options that are of interest to you before you move your money over. So have a little bit of a look, shop around. We would say take up a Pension Wise appointment to talk through what those different types of pension products might look like. But a key thing will be looking at the costs and looking at what you want.

Martin: So your biggest problem is the money seems to be trapped. You can't add to it. You can't deal with it. It's just frozen in this SIPP. Is that right?

Emma: Yes, that's right. So Mihir any idea of where she should go to unfreeze it? Let's melt it for her.

Mihir: I think, Emma, thanks for your question. Firstly, I think the first port of call is probably to understand why that money is frozen on that platform. Because even if you do not have an adviser attached to it, as you stated, you should still be able to access the pension and transfer it away. So if there's a reason it's frozen in there and you can't move it.

Martin: Do you know, Emma, what is the reason it's frozen?

Emma: No, I can take it out and transfer it I just can't add to it or take bits of it is my understanding. So it was on a platform that was that adviser had access to but because I'm no longer using the adviser.

Martin: I'm guessing you've got an advisory only platform one that the public can't use themselves. So then the issue him Mihir is you want to move it to a more public facing platform, like the two you mentioned earlier, AJ Bell or Hargreaves Lansdown, is that right?

Mihir: Correct, I would say that the first port of call is to probably move away to, like AJ Bell. or Hargreaves Lansdown on one of those sort of more reputed pension providers, just so you know that your pension is safe, first of all, and then you can access it. And then the question, obviously, is what Charlotte mentioned earlier, you need to have a look at the costs of the various sort of pensions available, as well as the access options. So not all of them offer flexible options, all of them. So that really needs to be the two things that you need to consider when moving away, or transferring away.

Martin: Summarising the information: step one is probably move it towards a much easier to operate, consumer facing SIPP provider. Once you've done that, then make an appointment with Pension Wise to start talking about what you want to do with the money for your retirement and making an appointment with Pension Wise is good information for anybody listening to this in any pension circumstance. It's always a good stopping to call it. I'm sure Mihir even as an independent financial adviser, you'd support that type of call?

Mihir: Absolutely. Yeah, I think the first point, of course, should always be a guidance session with Pension Wise or all of these other services out there. And then and only then if your circumstances are more sort of esoteric and complicated, then consider approaching an adviser.

Martin: Emma, does that answer your question?

Emma: Yeah, I think so. Both that last bit, but also the first person had said that he can go into other forms of pensions, which was helpful, doesn't just have to remain an asset.

Martin: No, but it doesn't. I mean, you could do it in one stage, you may want the Pension Wise call first. But if you want to keep it in a SIPP for flexibility, just moving it to one that's available to the general public is the right way to go through. It's what I'm hearing from our two specialists here. And thanks so much for calling.

So next set of questions is all about, are there ever any times it's just not worth putting money into a pension, Muncie saying, 'Well, is it ever too late to start saving into a pension?' And Annie is asking me 'with how pensions can be counted as income against welfare or care home funding, is it worth boosting a tiny private pension into a slightly larger private pension? I worry, it can be a lot of struggle and strife to save up, only to get excluded from the possible positives of a micro income'. Now, there is some logic in here because there is a top up to the state pension called pension credit for people who have no other forms of pension. And therefore, it could be slightly self-defeating, if you're near retirement to put a small amount in a pension, because you'd lose the pension top up, so you wouldn't necessarily have gained of saving. But that's an extreme case, isn't it, Charlotte?

Charlotte: It is, you start getting into the realms of how much how whether you're accessing the money, so if you're not accessing it, and it's sitting there, if it's below a certain level, then actually, that's not doing any harm. There are means-tested benefits, the way you go into that space, particularly if you're looking at going into a care home that you need to take into consideration, but each of them are a balancing act, in terms of what you need to pay, what you're accessing at the moment. And the point at which it comes into scope for assessment against means-tested benefits.

Martin: So help us through that, because that's the question. When is it too late? And how small is too small? I know, I know; I'm pushing you I can hear. But look, someone who's 45 wanting to save £100 a month it's going to be a benefit to them. Someone who's 65 looking to save £10 a month, it probably isn't fair. If they haven't got any other any other assets or income.

Charlotte: If they haven't got any other assets or income, then it comes down to what their outgoings are and yes, you have to ask the question about what would be the value, in what circumstances would it benefit them.

Martin: I understand that this is difficult because it absolutely varies. I'm trying to push you on scales of magnitude. So let's stick with that, you know, £65/£10 a month is going to be questionable. £45/£100 a month is probably not going to be questionable. Yeah. Mihir you have anything to add on this to help show that out and being mean?

Mihir: No, I think to broadly summarize, it's never too late to add to your pension firstly. But if you are 45, and you are proposing just to use that example, £100 a month, that, you know, over, let's say, 15 to 20 years by the time you get to retirement, given compounding, and you know, given the contributions that you'll make over that period, it's really about your time horizon. Do you have enough time left until you access that pension for it to grow?

Martin: You might be talking £40,000 to £50,000 on that amount, might you if you've done very well.

Mihir: Yeah, absolutely. I mean, it completely boils down to the investments that you have.

Martin: This is a dilemma people face, it's certainly on the pension credit. But it is only when you're talking very smaller amounts later in life that this is going to be an issue.

Charlotte: It is, so you're looking at anything less than £16,000, your money safe net, it's not really going to be counted against you. The other key consideration that a lot of people have is, is that pensions are a way of passing on wealth to your dependents, so your spouse or your children. So what we're seeing more of now is, is people saving in even in later years, and not accessing that pot, because it comes with tax relief, and you can pass that on. And that's a really big consideration.

Martin: What's the tax relief, the inheritance tax?

Charlotte: So you don't pay tax, you don't pay tax on it at all. So if you don't access that pension pot.

Martin: At any age?

Charlotte: And you were then to die, that pension pot gets passed to your spouse or your children after you.

Martin: So if you've never touched your pension, it can be passed down without tax, without capital gains tax.

Charlotte: Yes.

Martin: They'll still pay income tax on even if they...

Charlotte: Yeah, yeah.

Martin: But the lump sum was passed across as long as they've not touched it.

Charlotte: So if you can afford to save something, then what we're seeing more people do now is looking at that as a way of passing it on without inheritance tax. And a lot of people want to be able to do something for their families afterwards.

Martin: Brilliant.

We have a caller on the line, now Mihir, this is one for you, I think. Ben, where are you, Ben?

Ben: I'm in West London, Ealing.

Martin: OK, so Ben from Ealing? What's your question?

Ben: So I've just opened up a SIPP, and I'm 47 years old. And is it better to pay in regular small amounts? Or shall I take some of my savings and pay a large amount in one goes into the SIPP?

Martin: So should you spread it over time your contributions going in? Or should you just dunk it in? They call it pound cost averaging? Correct?

Mihir: It's called pound cost averaging Ben, thanks for your question. And to be honest, if possible, then regular investing is, in most circumstances preferable to doing a lump sum. And the reason for that is basically the market will go up and the market will go down. So if you have a regular amount going in at, you know, let's say on a monthly basis, then you take advantage of those dips in market performance. Whereas if you put in a lump sum, the market could fall sort of 5% to 10%, the very next day, and then you're kind of playing a bit of catch up. So the question comes down to market timing, no one can market time regardless of what they tell you. So in order to mitigate that as much as possible, putting in regular amounts on a monthly basis also, is probably your best choice there.

Martin: So we're talking about smoothing the risk, aren't we, if you put it in every month, then you're getting a generalized price. If you put it all in in one go, then you might be very lucky and bought at the bottom, you might be very unlucky, and bought at the top, either way, you're amplifying the risk. So putting in regular amounts over time rather than lump sums is a way of smoothing that risk out. Ben, what do you think about that?

Ben: That's great. That's, I kind of thought that just for clarification.

Martin: How old are you sir? if I may ask, you sound very young on the phone.

Ben: 47.

Martin: It's when your eyesight starts to go, you realize you're not that far from retirement, don't you?

Ben: Yeah, absolutely.

Martin: 45 my eyes went. It's when I had to start wearing glasses. I still haven't accepted it at 52. Thanks, Ben. Thanks for calling.

Ben: Thanks, Cheers, bye.

And I think that is probably a good place to leave it now. We've covered a lot. I have loads more questions, but I think people are probably exhausted with listening to this. We go back again to where I started. If you need help on pensions, start point is to call Pension Wise, get yourself an answer. It's totally free. It's independent guidance. But if you want more bespoke help you want someone to pick products for you, and you got a decent pension pot, it's worth getting yourself independent financial advice as well. So thank you very much to everybody who's called thank you so much to Charlotte Jackson, head of guidance at the Money and Pensions Service and Mihir Choghule is wealth manager at Tideway Wealth.

And that's it for this episode of the Not The Martin Lewis Podcast. Although there was actually quite a lot of me in there wasn't there. I hope I asked some questions that were interesting for you. If you've enjoyed it, please do listen to others in the Not The Martin Lewis Podcast series, the full episode lists some of them may not be out yet, depending on when you're listening to this, are renters rights, inheritance tax and probate, general tax questions and taking your money out of your pension. Do spread the word about the Not The Martin Lewis Podcast and the Martin Lewis Podcast series. I'll stop now; I'm getting myself confused.

Read a transcript of Martin's how to take money from your pension podcast

Martin Lewis: Hello, and welcome to the ‘Not the Martin Lewis podcast’, which rather, confusingly is an offshoot of my normal, ‘The Martin Lewis podcast’, the difference? Well, there are some subjects that are outside my wheelhouse or I can't answer questions on due to regulations. So in this podcast, I'm joined by specialists. And I'm asking not answering the questions. Well, it's me, I might chip in with the odd note or two, and crucially too it's you who sets the agenda, it's all about getting answers to your questions.

And this podcast is all about how you take your money out of your pension, the best way, we'll be talking about when is the right time to do it, how the 25% tax free lump sum really works, and how to avoid the huge pension withdrawal tax trap. Then a key primer on pension drawdown and annuities, crucial tools that you may need when taking money out of your pension. And should you take your tax free lump sum to clear the mortgage that and lots more, play the theme tune...

So joining me today to talk about how you take your work or private pension when you're near retirement or after retirement, in fact, is Charlotte Jackson, Head of guidance at the Money and Pension Service and Mihir Choughule, who's a wealth manager at Tideway wealth. Now we talked in detail when we did the program on how to build up your pension about the difference between guidance and advice. But I think that would be useful just as a very short one to start again, Charlotte, you and your organization do guidance and you do it for free. Anyone can call you up partly to talk about pensions

Charlotte: They can. We're a government that's organization we provide free independent and impartial guidance. That means that we'll talk to you about the things that you need to be thinking about, we'll give you some signposts around what you should be considering about doing next. But what we won't do is we won't tell you what to do, and we won't tell you what products or services you should be buying.

Martin: So look, this is an absolute Martin must rule. If you are thinking of taking your money out of your pension, do not do it without calling pension wise first. It is a complete mistake, it's totally free. You know, even if you know it all already, you may as well have it confirmed with someone before you take a decision that could very substantially affect your income for the rest of your life. We can then take it a step further, once you start to get into advice. Now my advice is regulated. And you Mihir you're an advisor when it comes to this. You can give actual bespoke information and what products people should be looking at.

Mihir: Yep, correct. So we will look at a person's specific personal and financial circumstances what their objectives are. And we will give you a bespoke detailed specific product and provider recommendations.

Martin: Now you're only advisory. But I mean, let's just pretend so people understand: you'll say you should put 50,000 pounds in this and you should put 60,000 pounds in this and that is our advice. It's up to the individual, whether they choose to take it or not. But that's how you'd work. And the difference, of course, you get paid. How do you get paid when someone taking the money out of the pension?

Mihir: I mean, it depends which firm you're with, you know, some firms charge you at the point of access of your pension. Other firms don't some firms charge sort of ongoing management of the overall pension and other assets that you have. Some of them charge sort of initial fees. So it varies depending on which firm you're with.

Martin: Yeah, but I mean, you are a proper professional service, and you will be paid a professional fee for doing the work that you do. Hopefully, if the advice is good overall, that will benefit people in the long run, because they will have done exactly the right thing for their pension. And you tend to focus independent advice tend to be for those with bigger pension pots for those smaller pension pots, then the guidance should be able to help them through what they need to do, because there won't be that many differences. Perfect.

Let's do some questions, shall we? I've got Leslie Hunter who says ‘my pension payments are ending soon. Recent correspondence confirms 25% of my pension can be received tax free. But I have multiple individual pensions. So would it be 25% of each or just one? One pension provider says they don't then manage part pensions and I should move it. I don't quite understand, what should I do?’ So let's just talk about how the 25% works when you've got multiple pensions.

Charlotte: So the 25% is across all of your savings. So this is where we need to be careful that if you access it on one pot and 25% that you need to think that actually you can't then take 25% from another pension pot. It's about what you are allowed to take tax free. So it's typically 25 percents you need to look at the whole. So in pension wise, we ask people to come to us, ideally, knowing what pension pots they have, so that you can look at what's the best solution in the round.

Martin: Yeah, so you want to be very careful what you take your 25% out of it, because you're taking it out of the thing that would have given you really good benefits. If you'd kept it in there for later in life might, have had an enhanced annuity rate or something like that. Come on to those two in a moment.

Charlotte: Exactly

Mihir: So the 25% is across your total pension assets. If you want to keep it really simple, then, you know, you can take 25% of each of your pension pots. And that way you will have used up your 25% entitlement. But like Charlotte said, there's also considerations regarding you want to take it from the best possible place, and you don't want to unknowingly jeopardise any sort of benefits or things that you may have.

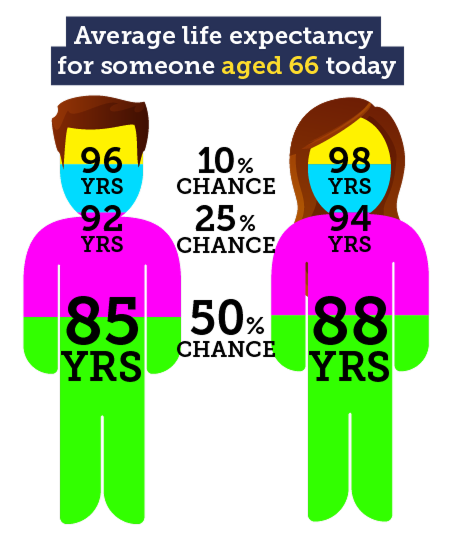

Martin: Now, when it comes to taking your pension, one of the big things that you need to consider is how long will you live? I know it sounds strange, but it absolutely is worth thinking about. Pension freedom starts at the age of 55. That's when you can take your money out of your pension, although that is going to move up to age 57 from 2028. So you think you've got that pot of money to last you for the rest of your life, you don't want to splurge it too soon, because you won't have anything left when you're older. Nor do you want to be overcautious, so that you're living an overly frugal life when you've saved up your money to enjoy it. Of course, most people at age 55 will still be working. So you won't want to take the money or use the income then you'll actually want to be continuing to save in your pension. It's all about finding a balance. But don't underestimate your longevity. For somebody who is aged 65: on average, a man will live another 20 years, a woman will live another 22 years. But you have a 10% chance as a man of living to 96, and a 10% chance as a woman of living to 98, and it's worth factoring that in. Admittedly your health, your genetics, whether you smoke and your current age or impact your lifespan. But it is worth getting into the zone, there isn't some calculators online that will try and give you a rough prediction of how long you'll live based on the very basic factors - nobody knows - of thinking how long the money is going to last. Now, the big thing to understand when it comes to taking your money out of your pension. And we're not talking here, defined benefit schemes where you're getting 20% of your salary for the rest of your life, we're talking when you've got a pot of money built up. A lot of what's worth thinking about is tax. So, pension freedom meant you can keep your money in your pension if you like think of it a bit like a bank account, and you can take your money out when you do. Now many people will know you generally get 25% of the money you take from your pension tax free, and the rest is taxed. But what counts and when it's taxed, that's where it gets complicated. So I want all of you now to imagine, picture it nice and tasty, a giant swiss roll. You have your giant swiss roll. Now most of your giant spread swiss roll is of course sponge, and you've got the luxury jam bit in the middle while the sponge is the taxable part of your pension and the jam running through the middle, that's your tax free amount. Now, if you take your money out of your pension using it like a bank account, you get a slice of the swiss roll. And that swiss roll contains whatever amount you've taken from your pension - 25% of it is tax free, and 75% of it is taxed at your marginal rate, whatever the income tax rate you are paying at the top. So you might be 20%, you might be a 40% rate taxpayer. But if you do what's called a drawdown or an annuity, and we're definitely going to talk about that more in the program, then you can just take the jam, you can take 25% of your pension totally tax free, and you'll pay the rest via the drawdown or the annuity later when you take it. So let's think about this. You decide you want to take that tax free lump sum early. You're a 20% rate taxpayer. Well, if you just take the money out, 75% of the money that you take out will be taxed at 20%, it might even push you into the higher tax bracket. But when you use a drawdown, you can take all the jam out the 25% tax free when you want it and the rest of the sponges left for you to take out of the drawdown or the annuity later on when you choose to use it. And this enables you to control when you're paying the tax on your pension pot. If you were to take a 25% lump sum now, and then later on in your life, as your income drops, you become a non taxpayer and take the rest out when you're a non taxpayer, you'll get a 25% lump sum now, and you take the rest of the money out, even though it's taxable, you won't be taxed because you're a non taxpayer, and that would be better for you. So that's what you're going to have to think about. That's the big picture of taking your money out. When is the money going to be taxed? And what portion of it is going to be taxed?

I think it's probably worth at this point, just going through those two options, drawdown and annuity Mihir, why don't you do drawdown?

Mihir: Sure. So drawdown essentially gives you complete freedom to choose the level of income that you want to take. And it can be a regular income, it can be a one off income. And you know, you get complete freedom to choose the amount of money that you want.

Martin: So just really, really spelling this out for people. So with drawdown, you'll have your pension pot, and we'll take a certain amount of it. Let's call it 100,000 pounds for ease. And we'll put it in what's called a drawdown product. It's a specific product to drawdown, isn't it?

Mihir: Yeah.

Martin: And then you have that money that drawdown is invested in you know, whatever your advisor has told you to invest it in a whole different range of things. And then when you want the money, you can take the money out of it. And is it really easy to take the money out? Are there any terms and notice periods that you need to get?

Mihir: No, most providers that I've worked with, they'll let you take money sort of instantly. There might be a form or so to fill out, but there's really shouldn't be any major paperwork needed to access that money.

Martin: So drawdown effectively, it's an investment vehicle that you have easy access to, to use savings terminology when you want it. But of course, as we've already discussed, when you take that money out, assuming you've taken your 25% lump sum, you will pay income tax on it at your highest marginal rate. In other words, if you're a 20% tax payer, you'd pay 20% on it, if you're a 40% tax payer, you'll pay 40% on it. So if you waited until later on, you had less income and were a lower tax payer, then you'd pay less tax on it. Annuities, Charlotte?

Charlotte: An annuity is when you are choosing to have a regular predictable level of income and to reduce risks. So where you make that decision, take 25% or not, and then you buy an annuity, and that annuity will give you a regular sum of money every year for the rest of your life. So you know exactly where you stand. You don't have to worry about your money running out, you know, what you've got coming in every month.

Martin Lewis: The summary the difference between the drawdown, a drawdown, the amount of money you have depends on the investment performance. With an annuity, you get a guaranteed amount that might be rising, guaranteed, rising with inflation or something on that basis, but it's a guaranteed amount. Now, interestingly, annuities used to be the way everybody basically had to take the pension pots, and they got a terrible reputation, primarily because the annuity rates were pants. And so you'd spend 100,000 pounds and you get, you know, 1500 quid a year from an annuity. But annuity rates are back up, aren't they?

Charlotte: They are. And I think they're coming back into favor because there's a lot to be said for knowing how much money you've got, particularly to your starting point, which is, you might live well into your 80s and 90s. And it's knowing that you've got might not look like a huge sum of money, but actually combine it with other savings, there's a lot to be said for that

Martin: And it pays you out each year until you die. And listen, and annuity is a genius product that if it had just been invented, everyone would be raving about it. The problem with annuities has been the rate is that it was very expensive to buy a small amount. Just some quick tips from me, if you are going to get an annuity, do not just get an annuity with your pension provider. There can be really big differences in annuity rates. And once you sign up to your annuity, that's it for the rest of your life. So if you're getting 10% less than you could have done, that's 10% less than you could have done for the rest of your life could be 10s of 1000s of pounds. Make sure you've checked whether you can get an enhanced annuity because you have poor health and definitely get least as a minimum, get guidance before you're getting an annuity. Make sure you're checking through everything right. But yeah, annuities and drawdown are the two big choices that many people face. Are you tending to see more people go for annuities than they used to Mihir?

Mihir: I mean, surprisingly, where we're not It depends, obviously on your you know, like Charlotte said, you know, the benefits are they do get a guaranteed income for your lifetime. But there's also cons to an annuity and the big con is that you can pass it on to future generations, the income ends with you know, if you've selected a spouse's pension after you pass away, then it will end up on the spouse's death and then that's it. You can't pass on anything further to your children. And we see a lot of clients who are kind of reluctant to make that decision not knowing what circumstances, the situation, they're going to be in 2030 years down the line. Whether there will need that level of income, for example, it is a really good option for some people.

Martin: I tell you what I find fascinating when I listen to the two of you, you can see the differences in your client bases. Right? So Mihir, you will tend to have more affluent people who are coming to you. So they may have enough money to live off, and therefore passing on money to their dependents is really important to them. Charlotte, you are the everyman service for want of a better phrase. So you're often people trying to eke out every penny that they've got to give them a subsistence standard of living for the rest of your life, which is I think, and it's worth people understanding that that is where the attitudes and the information that you're coming out with tends to differ. I don't think it is a philosophical difference between the two of you, I think it's a client base difference. And it's worth people understanding that in terms of where we think. I'm going to move on, I'm fascinated by that.

Gazza on Twitter, ‘When I draw down from my pension pot 25% is tax free. If I take 10% initially, and the rest of the fund increases or decreases in value, is my remaining 15% tax free, 15% of the new fund value, whether it's going up or down, or 15% of the original value when I took the 10%?’ Charlotte, what's the answer to that one. So

Charlotte It's that the point in time at which you're looking at taking it so there'll be a new calculation. So it's not going back to the time that you originally accessed it. It's what it is at the point in which you're looking at accessing that cash again.

Martin: So it is 15 percentage points of your 85 percentage points. So you are able to take 17.6% of the funds value, because that's the proportion that 15 is of 85 17.6% of the funds value when you Next take the money is how it works through. So in the answer to your question. It's the new fund value.

Next question. Andrea Stafford. ‘Hi, I look forward to hearing this podcast.’ - Me too. Andrea - ‘I have a question. Is it always best to take the 25% tax free lump sum, any circumstances where it might be best not to take this option?’ where you'd always want to take it tax free when you take it. So I think the question must be more about when do I take it? Do I take it at the point of retirement? Do I leave it?

Charlotte: Yeah and that's the bit about do you really need to access that 25%. Because the longer you leave that invested, obviously that’s still more money in there that can that can potentially grow. So if you don't need to access 25% At the point at which you're looking at retiring, leave it in there a bit longer, you can come back to it.

Martin: But I suppose you could take that 25% off to pay off your mortgage or to pay off any other form of high debts, which is often a good use of the money. Mihir is there any time it's worth, if you don't need to take the 25% it's worth taking it because you could put it somewhere else that it might be better.

Mihir: Like Charlotte said, it's always better to leave that 25% in if you don't need it, not all the time, but in most cases, because you know, investment growth means that it's you may potentially get a higher value in the future. If let's say for example, you're not worried about inheritance tax. So you know, pension benefits aren't really leaving them to the future generations isn't a major consideration, then maybe you can take the tax free cash and then put it into ISAs, for example, cash ISAs, the last few years have had quite good rates.

Martin: I was about to give everybody the rate of the best one today, which is Plum 5.17%. But we don't know when we're putting the podcast out. But you getting about 5% in the top cash ISA right now.

Mihir: Yeah, yeah. So I think there's options there, obviously, you have to be careful about sort of pension recycling rules and things like that.

Martin: So my thought was, for example, someone who doesn't need the money might decide they want to take 25% out in order to buy a property to rent out, which is not something you could do within your pension, you can invest in property in your pension, but it has to be in a pension fund. So the might be the occasional reason that there's an alternative form of investment, that you could use it for that way. Now, one of the issues is if you take money out of your pension, you can reduce the annual allowance, the amount that you're allowed to continue to contribute to your pension in future. How does that work? Is that with a 25% lump sum, or is it only with income?

Mihir: Yeah so, so if you take just the 25% lump sum, and you take zero income

Martin: that's the tax free amount.

Mihir: That's the tax free amount, then there'll be no impact to your annual allowance. If you start taking income on top of the tax free cash from your pension.

Martin: So that could be drawdown or an annuity.

Mihir: Yeah, well, whichever, whichever method, then your annual allowance will drop down yes to 10,000 pounds from from what the maximum is 60,000 at the moment.

Martin: but it's about your earnings that dictate how much

Mihir: Yeah, yeah

Martin: So that's really worth being aware of if you're going to start taking income out of your pension, but you might want to contribute to your pension in future. That's when you have that's the big nodal point where you've changed the status of your pension and you reduce the amount that you can contribute. Gotcha.

We got a caller on the line, we have Paul in Nottingham. Hello, Paul.

Paul: Hello.

Martin: Hello, what is your question for our pension specialists.

Paul: I have an outstanding mortgage, which currently is at 33,000. That's what's left on the mortgage. And I'm have a rate that it's a tracker mortgage, and I have a rate of 7.14% on it.

Martin: So that's quite a high mortgage rate.

Paul: Yeah that's right. And it's because it's only got actually three and a half years left to go. So it's getting right at the end of it. So we decided not to necessarily move it will transfer it but I agreed it's.

Martin: Well 33000 pounds with only three years to go, it wouldn't wouldn't be that easy to remortgage it with that relatively low sum and not long left. Yeah.

Paul: Yeah, this is what we thought. And this is part of the question, really. So we've looked into it, and that is, there's no obviously no charges if we were to pay off early, and we would get about 5000 pounds back if we paid off early. The key question here is, and I've got I've just turned 55. And I've got...

Martin: You look younger, sir.

Paul: Thank you, I sound younger as well.

Martin: On the phone

Paul: I've got a private sorry, I've got my own pension, which at the moment, it's performing around between 5 and 8%. I've been told. So the question I have is it would it be logical to take my drawdown option, pay off the mortgage with that, and then potentially put into savings? What I'm currently paying, which is about 1000 pounds a month into a savings account or into an ISA and some other account. Put a few reasons for doing it partly is peace of mind because then the mortgage is paid off. But also, obviously, then it means that I'm in control of what I'm what I'm paying out each month.

Martin: So let's just let's just let me simplify this for a second. You’ve got 33 grand left to pay on your mortgage, you've got 42 months left to pay. Should you be taking money out of your pension to pay off the mortgage? Now you call it a drawdown option. Have you taken anything out of your pension? Have you taken a tax free lump sum?

Paul: Nothing at all. No, it's not been touched yet.

Martin: Let me reframe this for you if you don't mind. Yeah, first, let's ask our specialists probably Mihir on this one. If Paul wants to take the money to pay off his mortgage, we'll come to whether we should in a moment, if he wants to take the money. What is the best way for him to do it to achieve that purpose?

Mihir: Best way and probably the most logical way, Paul is probably would be to take your tax free lump sum and use that to but take it up to the mortgage that you want to pay off. So 33,000 pounds on this instance.

Martin: So if you're what you're saying is if that wasn't 25%? If it was only 16%? Just take the 16%.

Mihir: Correct. Yeah, and leave the rest of the pension, and then use that to pay off your mortgage. And then the remaining tax free cash can, you know, hopefully grow with investments over the next few years.

Martin: But you’d do that in a drawdown if you just took it straight out of your pension, then you'd pay the tax and it wouldn't you.

Mihir: Correct, yeah. You'd say, yeah, you pay income tax at your marginal rate if you took it from drawdown

Martin: So to to do this, I'm just looking at you because it's your answer, not mine. You're going to move to a drawdown product, take the 25% tax free lump sum or less if you need to put the rest into drawdown.

Mihir: Yeah.

Martin: And anything to add to that, Charlotte?

Charlotte: No, you can do do that. I guess the question we don't know is how much money you've got saved into your pension. So you know what the 25% is.

Martin Lewis: Would the 25% be enough to cover the mortgage?

Paul: It would, I’m happy to share that, actually. So at the moment, it's about 350,000. So exactly, but they are across several pensions, which have made complicated, there is one, there is one that has enough to cover 25%

Martin Lewis: Well, I'd be slightly careful. We heard earlier, Charlotte said, so I'm gonna repeat what she said different pensions can have different rules, and so may be more beneficial than others for keeping longer term. So I would suggest you go and speak to pension wise, you know, once you decide what to do, and go through each of those individual pensions to see which one is best to get the money from, rather than just go for the one that's easier to get the money from, you want to go for the one that's best to get the money from now. So we now know how to do it, you're gonna get a drawdown product, you're going to take the tax free cash, and you've got easily you wouldn't even need to take all your 25% You'd be taking that right. You'd be taking about 10% of it, wouldn't you. Less? That's right. Yeah. So should you do it? I have my own views on this. I mean, how I would frame this, and I'm looking at our specialists to see if they disagree. Paying off your mortgage is a risk free rate of reducing debt, you're going to have an absolute certain 7.14% a year gain. So it's like savings at 7.14%.

Paul: Right.

Martin: So you're contrasting saving that 7.14% with investing in your pension which you said to me is getting you five to 8%. Of course it could be better, or it could be worse. So really for me whether you do it or not, is an equation between the certainty of saving 7.14%. and the risk, that it may be worse, but the risk and risk in a positive way that it may be a lot better. So that's how I frame it. Mihir, this is probably one for you.

Mihir: Yeah, I completely agree, Martin, I think at the rate that you're you're you're paying the mortgage at, I think it makes a huge amount of sense to take the tax free cash, and then pay off the outstanding mortgage. Because like Martin said, you know, you're

Martin Lewis: Glad you said, because that was my view as well.

Mihir: Because, you know, your your pension sort of average five to 8%. You mentioned that in that range. And the tracker mortgage is, you know, 7%. So, like Martin said, it's the certainty of paying off that 7% mortgage versus the risk of the pension over the next few years. Is that 5% let's say. so, yeah, the trade off there, you know, it's probably in favour of paying off the mortgage.

Martin: Are you generally a risky, personal risk averse, Paul?

Paul: That's a good question. risk averse, yeah.

Martin: Well, the risk averse option is pay off the mortgage, clearly, the risk averse pay off the mortgage. Right, exactly. Just clicking me here the fee for taking out a drawdown I suppose you're gonna have to do at some point anyway, aren't you?

Mihir: Yeah, I mean, it varies depending on what provider you're with. To be honest, there shouldn't be a huge fee, to be honest.

Martin: Yeah. Charlotte?

Charlotte: Is one of those ones you need to shop around to see who it is you want. But just to add on, you mentioned, Paul, that you had a number of different pots. So the thing is to think about, you don't necessarily need to make a decision on all of those pension pots, you could leave potentially the rest of them where they are, if it gave you access, and then particularly if you've got workplace pension, you're still paying into it. You're reducing some of the cost that you're looking at paying, and then enabling yourself to continue, whilst you're still at work. So don't feel rushed into making a decision on it.

Paul: Right. Yes.

Martin: Hopefully that helps, Paul.

Paul: That's really helpful. Thank you, and lovely to speak to you, Martin. Thank you very much. Thanks for your advice.

Martin: Aw that’s very kind of you, thank you very much. You can call again. Thanks, cheers.

Cassandra, ‘I withdrew a partial payment from one of my pension pots. I've had a letter confirming I'm subject to the annual allowance limit. I think I know what that means. But I'm trying to find an answer in plain English and that's impossible. Please help.’ Charlotte this is you. Plain English annual allowance limit. Charlotte’s buttocks, or if you heard on the other program we talked about her 'big buts’ before, now her buttocks are being clenched on the chair. All in a nice way.

Charlotte: Right. And it depends...

Martin: Okay, so Cassandra, here's how we're going to do this. I'm going to answer it for you. And then I'm going to let our specialists come in with any ifs or buts, I'm going to give you a nice, as simple as I can answer. Provided you haven't taken any income out of your pension, you are allowed to put in a maximum of 60,000 pounds a year, that is your annual allowance into your pension pot. But you can't put in more than you earn. So if you earnt 40,000, you couldn't put in 60,000. The more complicated issue, though, is there are ways you can count this backwards for unused allowances in previous years. So the simple answer is you can put in as much as you earn, as long as it's not more than 60,000 pounds. But if you've missed in previous years, you may be able to add on top of it. Now I'm going to pass over because it's not my podcast. This is not the Martin Lewis podcast, I don't have to explain. How do we fill in the missing learn years, Charlotte?

Charlotte: It is about looking back over how what you've earned over the previous three years to see if you've maximised it. And, again, it's one of the things that comes up a lot in our pension wise appointments, because we'll talk through whether you are at a higher rate tax earner or lower and how much you've saved in and we can help talk you through what those gaps are and how to go about filling that in.

Mihir: So I think Martin, your description was was basically spot on. I think that's probably probably the easiest way of explaining annual allowance rules. The question was regarding the annual allowance limit. Yeah, that you say. I mean, you're limited to by up to what your earnings as to what you can add in a tax year. But you can use the previous three years of carry forward, we call it technical term, to utilize and add more if your earnings are of an appropriate level.

Martin: Here's an easy way to answer this. If you have are looking at absolutely maxing out your 60,000 pounds annual limit. And you're looking to count back on previous years. If we haven't basically answered your question by saying, Oh, well, I can easily put in whatever I want. Then you're probably in the realms where you should be getting independent financial advice, and you should be doing bespoke because if you're up that amount going in one go, you should be seeing an independent financial adviser. Alternatively, me saying you can put in up to what you earn and up to a maximum of 60,000 pounds, and you're going I was only going to put in 4000 pounds anyway, then we've answered your question. So hopefully, I've managed to wriggle our way out of my specialist base having slightly pained faces are quite how complicated that one gets said, and we can do the next question.

BrandSwan and I don't understand this one, maybe I'm missing something obvious. ‘I have a drawdown pension. But when I take money out, I lose 33% of it. Why is that when I'm on the basic tax rate, and my only income is a state pension?’

Mihir: The reason I suspect? I mean, the question doesn't provide the detail, but the reason might be because HMRC are applying what's called the emergency tax code. So basically,

Martin: Charlotte likes that one, Mihir gets a point.

Mihir: So basically, if you access your pension on an irregular basis, let's say once a year HMRC for whatever reason, they deem it as though you're going to take that one off lump sum for all the remainder of the tax year, and therefore they apply tax accordingly. So what that usually results in is an overpayment of tax. It usually gets automatically rectified, it can take a few months, the easiest way to get your money back is filling out what is called a P55 form and sending that off to HMRC, and then they should correct the mistake.

Martin: Brilliant answer. We’re not 100% sure, that's what it is, but that would be your best guess. Thank you for that.

And a good one to finish a nice generous one from Doug white on Twitter here. I have several pension pots running, can I gift some of these to my wife to take his income to better manage tax when I retire? I'm guessing not.

Charlotte: No, you can't gift your pension to anybody. But you might look at how you could access money or help support additional payments into a pension. You can even set up a pension for somebody else. But you can't gift your pension to them.

Martin: You can set up a payment for a child, even if they don't work they can contribute 3600. And they still get tax relief on it 3600 a year.

Charlotte: And as grandparents, it's a really nice way of doing it. But you have to think about setting it up for them. You can't take yours and pass it on to somebody

Martin: Can I take a horrible way of swinging this? Is the one way to give your pension to someone else to divorce them? and then it can be awarded in a in a fiduciary judgment, and you could then split the pension?

Charlotte: you absolutely could.

Martin: Don’t do it and Doug, it's not worth it, man.

Charlotte: It's a sharing order. So it is one of the ways in which you can assign that money to somebody else. Particularly if you've got an amicable divorce. That's some of the things that we see around how you might be able to balance that out.