Turning 18? What to do with your Child Trust Fund

Child Trust Funds locked at least £250 away for most children born between September 2002 and January 2011 until they turned 18. With some finding they've now got £1,000+, that's a considerable birthday present. This short guide has everything you need to know about what happens now, and the best options for your cash.

We've three guides on Child Trust Funds:

What to do with Child Trust Funds: This guide shows you the options and helps you decide.

Top Child Trust Funds: How they work and how to get the best rates.

Not sure if you have a Child Trust Fund? Our guide helps you find lost Child Trust Funds.

How much could my Child Trust Fund be worth?

Child Trust Funds (CTFs) are tax-free savings accounts that were available for children born between 1 September 2002 and 2 January 2011.

Initially, children got free cash vouchers from the state of up to £250 (or £500 if their parents were on a low income) to be added to their CTF. Though a few of the youngest children born in the last six months of the scheme could have got as little as £50 from the state.

According to the latest figures from HM Revenue & Customs, the average balance of a CTF stands at £2,242 – but obviously you could have more or less than this. It'll depend on a couple of things...

The type of account the money was in.

Funds could be held as cash savings or investments. While cash savings were generally a safer option, investments tended to outperform them in the long-term, earning more along the way.

How much money was added along the way (if any).

The idea was to encourage parents to save for their child's future, with relatives and friends also able to add to the pot. Even if nothing else was added apart from the initial Government contribution, there could be £100 to £500 in each account.

What happens to my Child Trust Fund when I turn 18 if I do nothing?

Once you turn 18, the money is 'unlocked'. It legally belongs to you, and is yours to do with whatever you want.

If you do nothing, what happens will depend on where your CTF is currently held:

-

If it's in a cash CTF, it'll be converted to an adult cash ISA.

The only exception is if your provider isn't authorised to offer ISAs, in which case it'll transfer to an HMRC-protected account, which'll keep the tax-free status of the cash but won't let you contribute.

-

If it's in a stocks & shares (investment) CTF, it'll be converted to an adult stocks & shares ISA.

Again, if your provider isn't authorised to offer these, it'll transfer to an HMRC-protected account, which'll keep the tax-free status of the cash, though won't allow you to make additional contributions.

You can choose to leave your CTF in the account that it has been moved to, but don't assume that your provider's default option is going to be the best for your money.

Check with your provider about the account it'll transfer you in to, what the terms are and how you can access the cash if you decide you want to do that later.

Although there's no time limit to claim your CTF cash, you're likely to get more out of your money by making an active decision about what you want to do with it.

What should I do with the money?

The short answer is it's entirely up to you – if you've just turned 18, it's now your money. But this is MoneySavingExpert.com, so we want to help you make the most of your cash.

See How to start saving for full help, but here's a rundown of your main options. Do note that these are not mutually exclusive, you could spend some and save some, or save some and invest some. Just look what's out there and make the decision that works for you.

1. Move it to a top savings account or cash ISA

If you're not sure what to do with the money, at the very least you should make sure it's in a decent account so that in continues to grow while you decide.

-

If you want to be able to access it soon, or would rather not lock it away again, move it to a top easy-access account.

-

If you feel comfortable with the idea of locking it away for a set period, see top fixed-rate savings for higher rates.

Note: If you have a large balance on your CTF and it's earning you more than £1,000 in interest each year, you may want to keep the tax-free protection of a Cash ISA, otherwise you could pay tax on interest from normal savings. Here you'd need to ask the new cash ISA provider to do the transfer for you.

2. Put it towards a first home – and get a 25% boost

Owning a home might seem like a distant dream, but this could help. If you've never owned a home before and you're aged 18 to 39, you can open a top Lifetime ISA. This is a special tax-free savings account that gives you a 25% bonus on up to £4,000 saved a year (so a max £1,000/year bonus). You can then use this towards buying your first home valued up to £450,000.

This could give you a lot more free money, but there are some serious considerations to think about. If you decide not to buy, want to buy a first property that costs more than the £450,000 limit, or end up needing the money for something else, you won't get the 25% bonus and will have to pay a penalty to withdraw the cash. Do read our full Lifetime ISA guide to check it's right for you.

3. Invest it (or keep it invested)

First things first – investing is fundamentally risky. You're ultimately taking a gamble, as there's no guarantee you'll get all your money back. So while you could get lucky and make a big profit, you could also get unlucky and make a big loss. That said, there are ways to reduce the risk, and over the long run investing tends to beat saving comfortably – see our Investing for beginners guide.

If you do decide investing is right for you, or your matured Child Trust Fund balance is already invested, see our guide to Stocks & shares ISAs. It'll help you understand more about investments, and to find some of the cheaper platforms that let you do it.

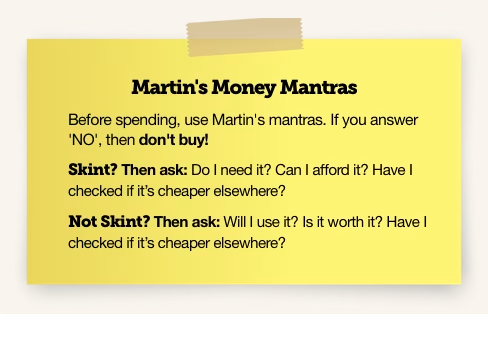

4. Spend it

If there's something you need – such as laptop for college or university, or a car to get to and from work – then this is exactly what savings are for.

We've just two questions to ask yourself before spending: Will I use it? and Is it worth it?

Just choose which option's right for you.

5. Use it to repay expensive debts

It's unlikely, as you just turned 18, but if you're quick off the mark (or have left it late to do anything with your CTF) and you have debts, like an overdraft or credit card, it may be worth paying those off instead of saving (see Repay debts or save?).

Share this guide?