Settle student loans at half-price? Martin says most should say no

Some university leavers who started studying between 1990 and 1998 have received letters and texts from Erudio – the company which manages their student loans – offering them the chance to settle their loan by partially paying it off.

MoneySavingExpert.com can reveal Erudio has been writing to borrowers who don't currently earn enough to have to repay their loans, telling them that if they pay off half their balance their "liability" for the rest of the loan will end. The letters only give a short deadline to take up the offer.

If you get one of these letters though, you should be extremely wary of accepting. It's important to understand that the loan may be wiped before you fully repay it, and partially settling your debt could affect your ability to get credit in future – Erudio has warned you won't ever be able to get another student loan from the Student Loans Company (SLC).

Student loans from pre-1998 – known as 'mortgage-style' loans – don't work like modern ones. They're payable over a fixed number of instalments once you start earning over a threshold – currently £30,737 a year. Once over this threshold, the amount you pay doesn't fluctuate based on what you earn – but the threshold itself is higher than with today's loans.

All student loans are eventually written off – worth bearing in mind before you repay. See Martin's blog: When will your student loan be written off? for full info.

Martin: 'Erudio is trying a fast one on most people'

MoneySavingExpert founder and chair Martin Lewis said: "The vast majority of people who get these letters should treat it like it's dirty, hold it by the edge and toss it straight away in the bin. Erudio is trying a fast one on most people.

"If you've still got one of these loans, it means you haven't paid it off in at least 20 years. So in most cases it's unlikely you'll ever pay any of it back, and even more unlikely you'll pay it off in full. While it may seem tempting to pay a lower figure than the outstanding balance, the loan will eventually wipe.

"Only those who are temporarily deferring and have a reasonable chance of earning over the £30,737 threshold should consider Erudio's offer. In that case, you should only do it if you're likely to pay off more than the settlement figure.

"To make this type of offer without fully explaining to people the pros and cons does not seem responsible to me for an organisation that has taken over Government-backed finances.

"This should not be treated like a Wild West. This is one of the reasons why we have campaigned that if there is a sell-off of any future student loans, the terms and conditions and the entire operating practices of the system should not be changed by the sell-off."

What do the letters say?

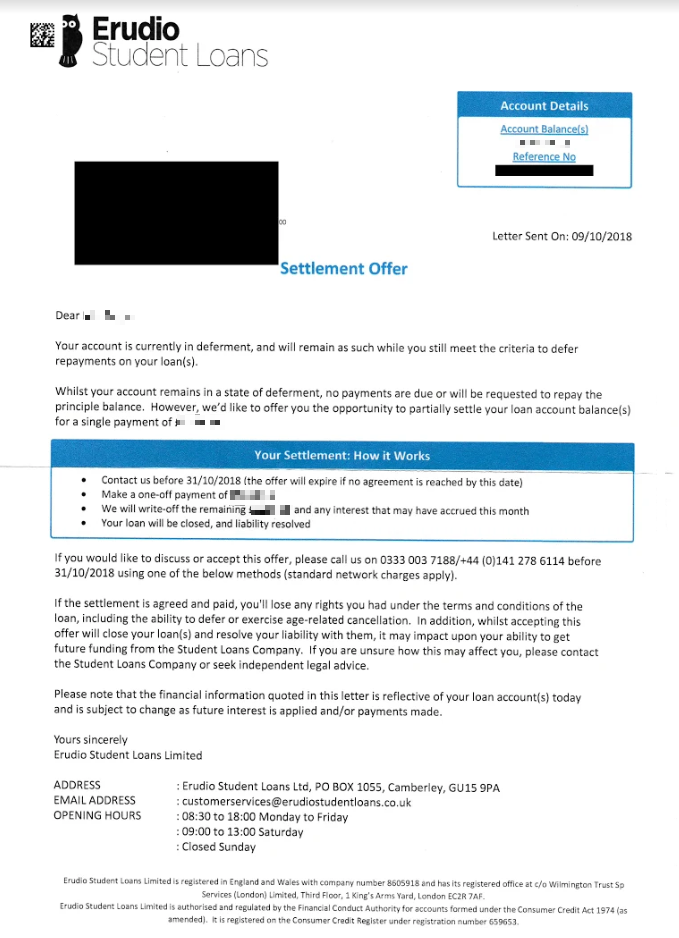

We've seen reports from at least a dozen university leavers who've received a letter from Erudio. The letters we've seen offer the borrower the chance to "partially settle" the loan for a one-off payment equivalent to half the amount outstanding. Erudio then says it will write off the remainder of the loan and the loan "will be closed".

But the letters also warn accepting the offer "may impact" on the borrower's ability to borrow money from the SLC again, and suggests borrowers contact the SLC or seek independent legal advice for more info. Borrowers are asked to contact Erudio on 0333 999 7263 to discuss or accept the offer – a deadline is given to do this.

An image of one of the letters can be seen below:

The letters we've seen set the recipient a deadline to accept the offer of around three weeks from when the letter was sent, though some have said they've ended up with as little as five days after actually receiving the letter. Erudio has told us though that if you contact it after the deadline in your letter, you're still likely to be able to take up the offer.

Some MoneySavers have also told us they have had follow-up texts to the letters sent to them as well – here's an example:

'A bullying letter'

Those who have received the letters have generally given a negative reaction.

One graduate, Alex, who started university back in 1997, told us: "It's a very short window for me to accept and some strange Ts and Cs.

"I've never earned enough to do anything but defer [repaying my loan]. I am confused – even if I could pay it, why would I?"

Others posted their responses on Twitter:

How do pre-1998 loans work?

Student loans taken out between 1990 and 1998 were bought by Erudio.

The company has been repeatedly criticised by MSE founder Martin Lewis for numerous blunders – see our Erudio to contact graduates again over deferment deadline blunder and Student loan deferment forms missing MSE News stories for more info.

In brief, loans taken out in this period are paid directly to Erudio in a fixed number of instalments, and you must make repayments if you earn over £30,737 per year.

If you're earning less than this you can 'defer' payments – ie, pay later – though you'll have to apply to do so. See more info here.

Like other types of student loans, these loans are written off after a certain period of time – but exactly when depends on how old you were when you took out the loan:

-

Aged under 40 when your last agreement for a loan was made? (usually your last year of study)? It'll be wiped whichever is earlier of 25 years after your first payment of your last loan agreement (usually the start of your final year), or when you reach 50.

-

Aged 40+ when your last agreement for a loan was made (usually your last year of study)? It'll be wiped when you reach 60.

I've got one of the letters – what should I do?

Be very careful when deciding what to do, and don't be rushed into a decision. There are several key questions to consider when deciding whether to take the offer:

-

Will you ever pay back more than the amount Erudio is asking you to pay? Some of those who've received the letter are just a couple of years from their loans being written off anyway, and say they don't expect to earn over £30,737 a year any time soon, so can continue to defer.

If you're in this situation, bear in mind if you take the offer you might end up paying back money you otherwise would never repay.

-

Would you be better paying off other debts first? With the loan interest rates at 3.3%, it's likely any other debts – whether credit cards, loans or hire purchase – are costing you more, so always pay those off before even contemplating repaying your student loan.

If you're still considering taking the offer, it's also worth bearing in mind:

-

It could affect your ability to get credit, although Erudio says it won't for now. Normally when you partially settle a debt, there's a chance it could affect your future ability to get credit, such as a mortgage or credit card, as credit files can be marked with a 'partial settlement' note.

Erudio told us that at the moment it does not report information to credit reference agencies – but it's refused to speculate on whether this could change in the future.

-

You likely won't be able to get another student loan in the future. Erudio says you won't ever be able to get further student loan funding if they have any arrears relating to previous loans/funding, so accepting this offer could mean you won't get any funding for further study.

What does Erudio say?

A spokesperson for Erudio Student Loans said: "Historically, Erudio customers have always been able to settle their account – with a customer's individual circumstances taken into account.

"Following this reactive approach, a proactive settlement campaign was launched in August with letters issued to eligible customers.

"Initial response has been positive with a number of customers settling their accounts. Although the letters have an expiry date, we would like to reassure our customers that if they respond after this time, they can still take advantage of the offer.

"Erudio cannot provide specific advice or guidance to customers on the suitability of this offer – what we can do is provide customers with any additional information they require to help this decision become clearer. For example, we can inform the customer of when the account will be eligible for age-related write-off and provide specific account information."

What does the Student Loans Company say?

A Student Loans Company spokesperson told us: "Erudio has a duty of care to ensure that their customers are aware of the implications for future funding should they choose to take up an offer of a discounted settlement."

The Student Loans Company also told us Erudio has autonomy on the letters it sends out.

Share this guide?

Latest weekly email

Latest weekly email

Clever ways to calculate your finances