Aged 40 to 73? Urgently consider buying National Insurance years

You may be able to turn £923 into £6,800 in your State Pension

There is a potentially unbeatable opportunity everyone aged 40 to 73(ish) needs to consider. If you're missing national insurance credits, you can buy back up to six years. This can be prove very lucrative, as some are on course to make over £50,000 in boosts to their State Pension by following this guide.

-

Under 40? Go through the exercise anyway. While it is more marginal to check if it's worth topping up, you may find a partial year worth buying.

-

Aged between 72 and 75(ish)+? This is for men born after 5 April 1951 (currently aged up to 75) and women born after 5 April 1953 (currently up to 73). Born earlier? You're on the old State Pension, so this doesn't apply.

Why National Insurance years matter

The full 'new' State Pension is currently £241.30 a week – however, how much you receive depends on how many 'qualifying' full National Insurance (NI) years you have.

Think of NI years as a bit like a token you can earn each tax year. The more tokens you get, the bigger the proportion of the £241.30 you receive once you hit that age.

Over a typical tax year, you earn NI credits from working, looking after children, or while on certain benefits. Once you've got enough credit in the tax year, you've then qualified for that tax year's National Insurance (ie, you've got the year's token).

-

You need at least 10 qualifying NI years to get some State Pension.

-

After that, the more years, the bigger your State Pension payout.

-

To get the FULL State Pension, you need 35ish qualifying NI years, and I can't stress enough the 'ish' – it varies widely for complex reasons (we've seen examples of people needing 44+ years).

If you're not sure what this is about, see how the new State Pension works.

Yet many are missing past NI years, commonly due to years abroad, low incomes, career breaks, or not claiming credits.

However, there is a strict time limit on buying back years. You can only buy back up to six years.

This is big money. It's the most lucrative thing many under the age of 75 can do, and some gain £10,000s, like Martine...

After listening to Martin's podcast, I checked my NI contributions and found I had eight years missing! I've now paid six years and will pay the next two years when possible. This has made a difference of about £49 a week, which is considerable! I'd never have known without the podcast! Thank you.

- MoneySaver Martine

To put that in context, Martine paid up to £5,000 (it may've been far less) to increase her State Pension by £2,550 a year. If she lives for the typical 20 years after state pension age, that'd be a total uplift of around £51,000... and it's inflation-proofed.

So, for some, paying to plug NI gaps is a no-brainer that could massively boost your pension. Yet there are lots of 'ifs' and 'buts' that could mean it's not right for you, so below we'll take you through it step by step.

Beware: If you'll retire with no other pensions or sources of income, then boosting your State Pension might not be worth it

There is effectively a minimum-income guarantee for pensioners, called Pension Credit, though it has to be claimed. It tops up low-income pensioners' incomes to £238 a week (or more if you have caring responsibilities or a long-term health condition). Importantly, it's also a gateway to accessing other benefits, such as the Winter Fuel Payment and a free TV licence (if you're over 75).

When we talk about income here, we mean any income – from state or private pensions, work, or income from savings or investments (above £10,000). Many people in a position to buy extra NI years won't qualify for Pension Credit. However if the State Pension is likely to be your only income, it's worth thinking about.

If you're not on course to get the full amount of £241.30 a week, or you already claim Pension Credit but you're thinking about topping up, you could find that buying additional NI years could push you over the Pension Credit threshold – and that losing those 'extras' could actually leave you worse off.

It's not always easy to work out because the income thresholds for Pension Credit vary depending on your personal circumstances, as well as any partner's income (and there's no future guarantee that pension credit will still work in the same way or even exist when you come to retire). But if State Pension will be your only income, and you're thinking of topping up, you should consider getting additional bespoke guidance on this, for example from Citizens Advice.

Crucially, you WON’T get this guidance if you call the Future Pension Service.

Step 1: Check whether you're missing any NI years since 2020

The first two checks you need to do are simple:

CHECK 1: Check for unfilled years in your NI record...

Here you need to:

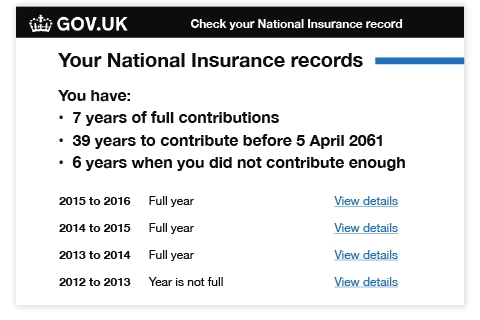

Check your National Insurance record

This shows your full National Insurance record. And for each year since you were 16, it will either say 'Full year' or 'Year is not full'. The 'View details' link will give you more information.

If you have 'non-full' years since 2020, it could be worth paying to plug these to get a higher State Pension. The rest of this guide deals with whether you should and how to do that.

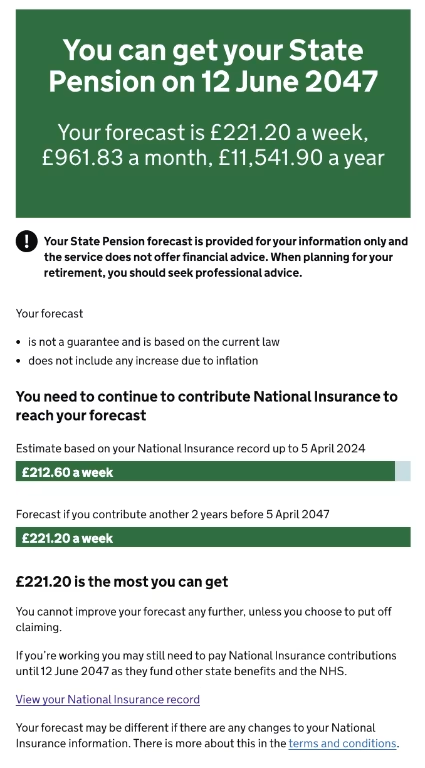

CHECK 2: If you have missing years, then get your State Pension forecast...

You need to use the Government's:

State Pension forecast calculator

This will give you some key information:

Your weekly forecast amount, as well as the 'most you can get' listed further down your forecast.

Whether you need to continue to contribute National Insurance to reach that amount.

How many years you still need to contribute National Insurance to reach that amount. If you don't yet have the minimum of 10 years' contributions to get any state pension, your forecast will tell you how many years you currently have on your record.

If your forecast ISN'T for the full £241.30 a week, and you have gaps in your NI record, you may be able to boost years to get to the full amount.

In some cases your forecast will be for more than the new state pension amount £241.30. This is because you're eligible for a 'protected payment', for contributions you made to the additional state pension or SERPs on the old state pension before 2016.

There's a link in your forecast to do this, or you can use the link in the box above. Once you've checked your NI record, go to step 3.

In most cases, if you're projected to get a full state pension – even if you're currently missing some years – buying extra years won't boost the amount you'll get. That's because you can't get more than the full state pension (and if you do end up missing future years, you can always buy them then).

BUT the forecast will assume that you're going to continue working in the UK until you hit state pension age. If you're not planning to do that – maybe because you want to take an early retirement or live abroad for some years – you'll need to factor that in, even if your forecast says you're on track for the full amount. If this applies to you and you're unsure what it means for your state pension, your best bet is to speak to the the Future Pension Centre.

Step 2: If you have gaps in your record, see if you can plug 'em for FREE with NI credits

It's not only work that earns you NI years. A range of scenarios see you build up NI entitlement automatically. (There are a few issues currently with adding NI years if you're claiming Universal Credit.) Yet some credits need to be claimed manually to fill gaps – see if any of these scenarios fit:

-

Caring for a child in the family: As long as you are/were between 16 and State Pension age. If it is your child, only one parent can claim the credits via Child Benefit, but you can transfer the credit from one parent to the other – see our Child Benefit guide. If the family member is/was under 12 and not your child, see our Grandparents' Childcare Credit guide for more info.

-

On Statutory Sick Pay: You are/were on it and not earning enough for a qualifying year.

-

Unemployed and actively looking for work: You needn't have been claiming Jobseeker's Allowance, but will need to prove you were looking for employment.

-

On Employment and Support Allowance: Eligible for it, but not claiming it.

-

Caring for a sick/disabled person: If it is/was for at least 20 hours a week. See our separate Carer's Credit guide on this for more details.

-

On jury service: You are/were on it and aren't/weren't self-employed.

-

Wrongly imprisoned: As long as your conviction has since been quashed.

-

A foster carer (kinship carer in Scotland): Since 6 April 2010.

-

On Statutory Maternity, Paternity or Adoption Pay: You are/were on it and didn't/won't earn enough for a qualifying NI year (Additional Statutory Paternity Pay also counts).

-

Spouse of a member of the armed forces: You're married to, or are a civil partner of, a member of the armed forces and went with them on an overseas posting (additional eligibility rules apply here).

-

On a Government-approved training course: You are/were on one, are over 18, and weren't sent on the course by Jobcentre Plus.

Full information on how to manually apply for any NI credits you're due is on the Government's National Insurance credits page. Most will have already got any NI credits they're due. But if you haven't, make sure you claim them and then start this process again.

Step 3: Work out if you should pay to boost your State Pension

If a shortfall in State Pension is likely and you've NI gaps in the past six years, you need to decide whether to top up. Some help...

-

Those at or near State Pension age will find it relatively easy to see if topping up may help.

If your State Pension is, or is forecast to be, less than £241.30 a week, and you won't be able to plug gaps by any other means, topping up could be a no-brainer.

-

For those older than 40 but still some way off State Pension age it's more of a toss-up, as you may still fill the gaps naturally. The younger you are, the more time you have to earn enough qualifying years before you reach State Pension age.

-

For most under the age of 40, it probably won't make sense to pay for full NI years, but it might be worth checking if you can upgrade partial years on the cheap. If you've gaps in your NI record that you're certain you won't make up (for example, if you've moved overseas), or if you're really worried about not being on track and want some extra peace of mind, it might be worth checking if you have any partial years in your record, as these can sometimes be upgraded to full years for as little as £16 – we've more details below.

It worked for Caroline, who emailed:

I am absolutely delighted... I was only one week short of a full year. I've paid a one-off payment of £15.40 [voluntary class 3 National Insurance 2021/22 rate] to get an extra £127.92 per year on my State Pension. So once again a success!

- MoneySaver Caroline

State pension forecast says you were contracted out?

We’ve had many questions on this, so wanted to add some detail. You might have discovered from looking at your State Pension forecast that you've been in a 'contracted-out' pension scheme. That's because you may have chosen to ‘contract out’ your State Pension into a private pension (before 2012) or your employer may have done it for you (until 2016)

All this happened before the ‘new’ State Pension was introduced in 2016. Contracting out was a way to use funds that would’ve been paid towards your state pension to instead build up a private pension. It means you opted out of making additional payments which could have meant you got an extra amount of money on top of your State Pension (known as Additional State Pension or SERPs).

This will likely mean you will need more that the normal 35 years-ish of contributions to get the full State Pension, for some it could be in the forties worth of years.

Can I top up the years I was contracted out?

-

You can't top up your National Insurance for full years when you were contracted out. Even if you paid a lesser amount of National Insurance, it was still the correct amount under the contracting-out rules, so it'll appear as a 'full year' on your record.

-

You can top up any partial years, for example if you were only contracted out for part of the year. Whether it's worthwhile will depend on your personal circumstances, including how many years you're missing. In this case its very important you get one-on-one phone help to work it out, see the how to get individual help section below.

If you were contracted out, you may have done well out of it

Remember that money was paid somewhere, and its possible it has had good investment growth. If you're not sure what happened to your money, you can search for Lost Pensions, using these steps (If you’re not sure whether it was you or your employer that chose to contract out your pension, it’s worth going through both steps):

If you chose to be contracted out

Look for any paperwork to find the names of providers.

This could be old letters or annual statements from pension providers.

Use a Pension Tracing Service such as Gretel. Gretel is a free catch-all service you can use to find pensions or other lost assets. Gretel will then do a 'soft search' on your credit report to check your identity and match you with previous addresses where you may have accounts registered. Not all financial institutions are signed up to Gretel, so you may not get a match straightaway – but it will continue to search and will let you know if your details match a lost pension in the future.

If your employer contracted you out

First, check your payslips from before 6 April 2016.

If you have any with the category letters D,E,L,N, or O this means you were contracted out.

Use the Government's Pension Tracing Service. You can use the Pension Tracing Service to find out the name of the scheme your employer (or ex-employer) was signed up to. It won’t tell you whether you have a pension or not, but it will tell you the details of the workplace pension scheme your company uses.

Once you’ve know where you might have a pension pot the next step is to contact the providers directly. Once you locate your lost pensions and have discussed your options with your provider, you can choose what to do with. It'll be a good idea to seek independent financial advice, especially if there's anything you're not sure about or you've stumbled across a large sum of money.

Step 4: Use our calculator to see what topping up could be worth

The rate you pay depends on which year you're buying. If you're buying the previous two tax years, you'll pay the original rate for those years. But, if you're buying earlier years, you'll pay the current (2026/27) rate. The rates are as follows:

Tax year | Rate |

|---|---|

2026/27 | £956.80 (£18.40/week) |

2025/26 | £923 (£17.75/week) |

2024/25 | £907.40 (£17.45/week) |

2023/24 | £956.80 (£18.40/week) |

2022/23 | £956.80 (£18.40/week) |

2021/22 | £956.80 (£18.40/week) |

2020/21 | £956.80 (£18.40/week) |

It can cost less that this if you're self-employed or you're topping up a partial year.

Use our calculator below to see how much buying NI years could be worth, then look at our life expectancy tables to work out if you'll likely live long enough to benefit.

How much could it be worth?

Say you buy an NI year that costs you £923 and adds up to £358 each year to your pre-tax State Pension, it's worth it as long as you live at least three years after getting your pension (or three years after you top up, if you're already getting it).

Note that you can't pay to increase your State Pension beyond the maximum of £241.30 a week, so if you're projected to get £200 a week or more, topping up is less good value for money.

Our calculator gives an indication of the maximum amount buying different numbers of NI years could be worth in today's money, but it's important to note that the figures it gives you are before tax.

So if your only source of income is likely to be your state pension (and you won't have any other income from private pensions, work or other sources etc), you'll likely be under the taxable threshold (though close to the 20% basic-rate).

The more other income you have, the more likely you are to push up through the tax brackets – and you'll have to factor in any tax you're due to pay into the gains listed in our ready reckoner below.

How long are you likely to live?

The potential gains to be made from buying voluntary NI contributions are huge. But one of the factors it depends on is if you'll live long enough to gain. Consider your health and use our life expectancy tables below to see if you're LIKELY to benefit.

Using data from the Office for National Statistics' life expectancy calculator, the tables show how many more years people in different age groups can expect to live on average...

Women | ||

Current age |

| Average life expectancy |

|---|---|---|

40 | 68 | 87 |

45 | 67 | 87 |

50 | 67 | 87 |

55 | 67 | 87 |

60 | 67 | 87 |

65 | 67 | 88 |

70 | You were eligible at 62 | 88 |

75 | You were eligible at 60 | 89 |

80 | You were eligible at 60 | 90 |

Men | ||

Current Age | Age at which you qualify for the State Pension | Average life expectancy |

40 | 68 | 84 |

45 | 67 | 84 |

50 | 67 | 84 |

55 | 67 | 84 |

60 | 67 | 84 |

65 | 67 | 85 |

70 | You were eligible at 65 | 86 |

75 | You were eligible at 65 | 87 |

80 | You were eligible at 65 | 89 |

Life expectancy data provided by the Office for National Statistics.

Could this all be a waste of money if the pension system is changed?

It is almost certain that those who have the full number of years on their National Insurance record will get more pension than those who don't, and that is unlikely to change. But when you're considering paying for something now that might not give you a return for many years to come, it can come with known and unknown risks.

Step 5: WARNING – don't pay until you're confident that it's right for you

We've given you a general idea of how this works. But there are many complexities, so the only way to know for sure if this is likely to benefit you is to get personalised information.

The Government has set up a new online service that will show some people how much their State Pension could increase by and the NI years needed to achieve this.

You'll then be able to pay for these missing years securely online without having to speak to anyone. You should only do this if you're happy it's the right course of action though – it is possible to pay to plug a gap and see no gain. If you have questions or don't understand the process, you can still speak to someone – contact details are below.

The new online service isn't available to everyone at the moment. You won't be able to use it if...

You're already at State Pension age.

You're within four months and eight days of State Pension age.

You're filling gaps from when you were self-employed.

You're filling gaps from when you were working abroad.

You hold a Married Women's Reduced Rate Election certificate.

You're eligible for Home Responsibilities Protection.

If any of those apply, you'll need to call up to be able to do this.

Need to speak to someone?

If you're currently unable to use the new online tool or need personalised information, you can still call up to find out more about your NI record and to pay for missing years. The service you use will depend on your age:

-

If you're not yet at State Pension age, contact the Future Pension Centre on 0800 731 0175.

-

If you're already at State Pension age, contact the Pension Service on 0800 731 0469.

Both the Future Pension Centre and the Pension Service are open between 8am and 6pm, Monday to Friday, and provide specific information about your current National Insurance record. They'll tell you whether doing so will actually result in any increase to your (eventual) State Pension. It is possible to pay to plug a gap and see no gain, which is why this step is so important.

Step 6: Not everyone will be better off if they buy more NI years

The Government's online service, and the Future Pension Centre or the Pension Service can tell you if paying for extra National Insurance (NI) years will increase your State Pension entitlement. But you need to think about the bigger picture (the Government helplines won't help with that). Think about:

-

If you're likely to have a low income and will only rely on the State Pension, then Pension Credit might cover the gap. Pension Credit is a top-up for people of State Pension age who don't have a certain basic level of income. So there's a risk you can get the same amount of cash with Pension Credit without paying to top up. Being in receipt of Pension Credit also entitles you to other benefits, such as the Winter Fuel Payment and a free TV licence (if you're over 75).

Though it's worth us saying, there's no guarantee that Pension Credit will still exist, be at the same level or have the same eligibility criteria when you retire. More info in Pension Credit. -

The gains from buying extra years may be reduced if it pushes you into a higher tax bracket. If you were to be near the threshold of either paying tax or hitting the 40% tax bracket once your State Pension and other income is combined, you will pay (more) tax on your pension income if that income is higher.

This will mean it takes longer for you to breakeven on any voluntary NI contributions you make – though it's likely to still be worth doing, even with this. Check out the latest tax rates and try our Income Tax Calculator to see if this might affect you.

Martin Lewis: We've covered the known risks, but what about the unknown ones?

"So far in this guide, the team and I have covered all the known pros and cons, so you can evaluate if it's right for you. And for many people, buying extra years will be extremely lucrative.

However, when you’re talking about making a payment now for a return that will take decades to accrue, it’s worth briefly contemplating whether there are other political risks too – and two come to mind.

More likely: State Pension age changes. It's possible, and maybe even probable, the age at which you're eligible to get the State Pension will be increased again. If so, you'll have fewer years on the State Pension, which could reduce the expected return.

Less likely: State Pension could be means-tested or even scrapped. With the eyes of someone in 2024 I think this is unlikely, yet who knows where we’ll be in the high tech world of AI, flying skateboards, and talking toasters of 2040.

And of course these are known risks; there are also unknown risks too, as with everything – the ones people haven’t thought of yet.

I don’t write this to put you off. I think if it’s right for you, topping up your State Pension is likely to be hugely lucrative for many. It’s more to make sure you’re aware that even if you do all the checks, go through the bespoke state 1-on-1 advice, there are no perfect checks, everything involves an element of faith.

Certainly the nearer you are to State Pension age the more solid doing this looks. Yet for those in their 40s the structural changes that happen in society over many decades leave a lot of room for uncertainty, so a little more care needs taking before shelling out too much.

Even so as, you need at most only a few years of taking the State Pension to break even, the risks of losing money if you live to a typical age, are pretty slim. And even if the most likely of these risks, that of an increased State Pension age happened, it would only mean what is an extremely lucrative purchase for many right now, drops to being just very lucrative."

Step 7: How to pay voluntary NI contributions

There are two ways to do this, online or on the phone...

Online

If you've spoken to the Future Pension Centre or the Pension Service and want to buy additional NI years online, or are happy to just go via the Govt's online service, here's how to do it:

-

Access the service through 'Check your State Pension forecast' page on Gov.uk. It's also available through the HMRC app, which you can download free on the Apple App Store and Google Play Store.

You'll need to log in using your Personal Tax Account login details (this is your 'Government Gateway ID' and password). If you don't already have an online HMRC account or Government Gateway ID, you can register at Gov.uk. -

Decide how many NI years to buy. You'll then be shown your full and partial NI years, and how much your State Pension could increase if you choose to fill the gaps. You'll be able to pay for these missing years securely online, without having to call up separately. You need to pay for these in full via bank transfer or through 'Open Banking' – you can't pay in instalments.

Warning! It is possible to pay to plug a gap and see no gain, so always speak to someone if you're unsure.

On the phone

If you've spoken to the Future Pension Centre or the Pension Service, but can't or don't want to use the online service to top-up, here's how to do it:

-

Decide how many NI years to buy. Do note that you don't need to buy all the NI years you want in one go.

-

Contact HMRC to get an 18-digit reference number. To find the precise cost of the years you want to buy, and get the reference you need – this is important so they're added to the right NI record and tax years. You'll need to contact HM Revenue & Customs (HMRC). It can give you the number over the phone, via its webchat service, or by post.

-

Send the money to HMRC. Once you have the 18-digit reference number, you can purchase years by through online or app banking or by sending money through your bank or building society account to this HMRC bank account. You can also pay by cheque, though HMRC says this takes longer to process.

-

Wait for the extra NI years to be credited to your record. If you're not yet claiming State Pension, the payment can take up to 60 working days to process, after which you should see your NI record change.

If you are claiming State Pension, HMRC will prompt the DWP to carry out a 'benefit review', so your payments won't increase straightaway. However, the DWP will backdate the increase to the date you made the payment (NOT to the date you started claiming State Pension).

FAQs

What if I'm self-employed?

If you're self-employed and have profits over £12,570 a year, you have to pay two types of National Insurance (NI): class 2 and class 4. Class 2 NI goes towards your State Pension.

If your annual profit is between £7,105 and £12,570, you automatically build up entitlement to benefits (including State Pension). If you earn less than £7,105, you don't, so you may want to consider paying voluntary contributions to top up.

Be aware that examiners and moderators are also treated as self-employed earners (visit Gov.uk for more info), so if you've done things like exam invigilating in the past, you could potentially save a lot of money on your NI contributions.

That's because Class 2 NI is currently £3.65 a week – which is a much lower rate than employees' NI. So it would cost you about £189.80 to buy one year's worth of class 2 NI contributions.

As with class 3 contributions, one qualifying year of NI adds about £358 a year (or £6.70 a week) to your State Pension. So topping up is likely to be a no-brainer for many – paying less than £190 now to buy one year of NI gives you £358 a year back in state pension for the rest of your life.

Bear in mind that once you reach State Pension age, you'll have to pay the higher rate for voluntary contributions (currently £956.80 for one year), so if you're eligible to buy class 2 contributions, it's worth checking NOW if making voluntary contributions is beneficial for you. But make sure you contact the Future Pension Centre first to get tailored advice.

Making class 2 voluntary contributions

If you file a self-assessment tax return, and your profits are less than £7,105, you'll be able to pay voluntary class 2 contributions as part of your next tax return.

If you don't file a self-assessment tax return, but qualify for class 2 contributions, you can make them by:

- Setting up a monthly Direct Debit (note this is only available for the current tax year, not for plugging historic gaps).

- Approving a payment with your online or app banking.

- Sending a payment through your bank or building society online or at a branch (you'll need to get an 18-digit reference number from HM Revenue & Customs).

- Posting a cheque to HM Revenue & Customs (HMRC).

If you live abroad, you need to read and complete form CF83 (found at the end of leaflet NI83) and send it back to HMRC using the address on the form. If you're enquiring about gaps for past periods, you'll need to contact HMRC for more information.

If you're a director of a limited company, you're still classed as an employee

Directors of limited companies are considered employees, rather than self-employed, and are required to pay class 1 National Insurance on annual income from salary and bonuses over £12,570.

Contributions are worked out from their annual earnings rather than from what they earn in each pay period. Voluntary contributions are charged at the higher class 3 rate.

What if I've paid SOME National Insurance, just not enough for a 'full qualifying year'?

When you check your NI record, it'll show any gap years. For every gap year, there'll be a 'more details' header where you'll be able to see the size of your shortfall and how much it'll cost to fill. A gap year does not necessarily mean you're missing 52 weeks – in some cases, you might only have to buy one or two weeks' worth of contributions.

Why employees might need to pay for partial years

For a full qualifying year of NI contributions, you need to earn at least £6,708 a year from a single employer – however only weeks where you've earned at least £129 (the 'lower earnings limit') count towards this total. So employees could find they fall short of a qualifying year – sometimes by just one or two weeks – even though they might've earned more than £6,708 that year.

For example: Ben earns £200 a week for 31 weeks and then £100 per week for the remaining 21 weeks. In total, he's earned £8,300. However, when he subtracts the weeks where he didn't earn at least £129 a week, his qualifying earnings total £6,200. This is £508 short of the £6,708 threshold for a full qualifying year. The way that HMRC calculates Ben's shortfall means if he buys three weeks' worth of voluntary class 3 National Insurance he can turn this 'gap year' into a full qualifying year.

Why self-employed people might need to pay for partial years

If you're self-employed and your profits were less than the Small Profits Threshold (currently £7,105), you wouldn't automatically pay any NI contributions and typically you'd need to pay voluntarily for Class 2 contributions for every week you were self-employed for the year to become a 'qualifying year' for State Pension purposes.

However, you might've earned NI credits in other ways (see step 2 above), therefore would only need to pay for the weeks in shortfall. As mentioned above, when you check your NI record, the details of all credits earned and any shortfall for that year will be displayed.

How HMRC calculates partial years

HMRC subtracts what you've earnt over the year (but only in weeks above the £129 threshold) from the £6,708 threshold. Then it divides the difference by £129 (for example, one week's qualifying earnings) to give the number of weeks shortfall, which is then rounded up to a whole number of weeks (as you can't pay for partial weeks).

For example: Using the same example as above, Ben is £300 short of the £6,708 earnings threshold for a full qualifying year. So 300 is divided by 129 to get 2.3, which is rounded up to 3. Ben needs to buy three weeks of voluntary class 3 National Insurance contributions for his 'gap year' to become a full qualifying year.

I'm under 40, should I pay to plug gaps in my National Insurance record?

For most people, the answer is probably not, as you have plenty of time left to max your State Pension entitlement by earning qualifying years automatically. Any money you spend plugging NI gaps now could prove to be a waste if it turns out you'd have had enough qualifying years to get a full State Pension anyway.

However, you may decide it's worth the risk if you've lots of gaps in your NI record, particularly if they're partial gaps, as these can be very cheap to fill.

When you check your NI record, it'll show any gap years in chronological order. For every gap year, there'll be a 'more details' header where you'll be able to see the size of your shortfall and how much it'll cost to fill. In some cases, to get a full qualifying year you might only have to buy one or two weeks' worth of contributions, which would only cost between £18 and £36.

If you can afford to do this – and as long as you understand that spending this money may not boost your State Pension entitlement beyond the max when you reach State Pension age – it may be something you want to consider for the extra peace of mind.

You're only able to plug gaps over the past 6 years. So, while we're in the 2026/27 tax year you can fill gaps as far back as 2020/21.

The example below shows when it might make sense for a young person to top up a partial year:

Hannah, 35, spent her 20s and early 30s studying and working abroad. After checking her NI record, she found she has no full qualifying years.

Last tax year, she earned £0 in the first week of the year and then took a job as a part-time tutor, earning £129 per week for the remaining 51 weeks of the year. For this to count as a full qualifying year, she needed to earn at least £6,708 a year, with only weeks where she earned at least £129 counting towards this total.

Her NI record shows that she needs to buy one week of voluntary class 3 National Insurance contributions for this year to become a 'full qualifying year'.

What if I live or work abroad?

You can choose to pay voluntary class 2 National Insurance (NI) contributions if you live and work abroad. The only requirement is that you worked in the UK immediately before leaving, and that you previously lived in the UK for at least three years in a row or paid at least three years of NI contributions. If you've retired abroad, you'll need to pay class 3 NI.

This may be useful if you want to have access to some benefits – including the State Pension – if you return to the UK. In fact, you can continue to receive your State Pension even if you don't return to the UK, as long as you have at least 10 qualifying years of NI.

Is there a maximum number of missing years I can buy?

Yes. If you reached or will reach State Pension age after 5 April 2016, you can only go back a maximum of six years to fill in gaps. So, while we're in the 2026/27 tax year you can only plug gaps as far back as 2020/21.

If you reached State Pension age on or before 5 April 2016, you can also only top up a maximum of six years. However, the actual amount of voluntary NI contributions you can make depends on your circumstances and is likely to be much less than the maximum. Contact the Future Pension Centre to find out how many years you can buy and what it will add to your State Pension. If you've already reached State Pension age, you'll need to contact the Pension Service.

Can I pay for voluntary National Insurance contributions by monthly instalments?

No. There's no option to pay for voluntary class 3 National Insurance (NI) contributions for previous years by direct debit. But if you're looking to buy several years of NI contributions, you don't need to pay it all in one go – you can pay for each year separately. Do note though that the deadline of 5 April 2027 applies if you're planning to fill a gap in the 2020/21 tax year.

I claim Universal Credit, but my National Insurance credits are not showing on my record

If you claim Universal Credit, you are entitled to automatic National Insurance credits for the duration of your claim. However, there have been many reports of MoneySavers telling us that when they check their National Insurance record, these automatic credits are missing.

We're aware of technical issues with the transfer of data between the Department for Work and Pensions (DWP) and HM Revenue & Customs (HMRC). And the DWP has assured us that the department is working on an improved process to add historic and future credits to claimants' records.

If you currently claim, or have claimed Universal Credit at any point, you need to check your National Insurance record on Gov.uk and see if you're missing any credits. If you are, don't panic.

The DWP says that once the issue is resolved, claimants' records will be corrected.

HMRC is advising claimants to wait until Universal Credit credits are showing on their record before making any voluntary payments needed to make that a qualifying year. If any payments are made unnecessarily, they can be refunded.

Will I get a refund if I buy extra years and then find out I didn't need to?

If you made voluntary contributions for tax years you later find out you didn't need to increase your state pension (for example, because of a backdated HRP award), you can request a refund.

Whether you'll get one is determined on a case-by-case basis, and there are no hard and fast rules on whether you'll be successful or not.

However, it's worth applying if you think you might've paid unnecessarily, especially due to an error outside of your control.

To apply for a refund, you'll need to write to HMRC at the following address:

HM Revenue and Customs

National Insurance Contributions and Employer Office

BX9 1AN

In your letter include your National Insurance number, the reason you want a refund, and the years you would like refunding.

Full information on how to apply for a refund can be found on Gov.uk. If you need help, HMRC has a National Insurance enquiries helpline you can call on: 0300 200 3500.

Share this guide?