Mastercard vs Visa for using abroad – which wins?

Update August 2016: This news story was written in May 2015, though we've done further analysis on the Mastercard and Visa rates since then, and the logic is still the same – Mastercard still usually comes out the winner. We will do a full update of this article soon...

The closer we get to summer, the more people are thinking of holidays. And while it's much less interesting to think of holiday money than it is to think of sunny climes and getting away from it all, getting it wrong could cost you £100s extra over the course of your trip.

With the launch of our new travel guides last week, some analysis we did got us thinking: we know that specialist overseas credit cards give you the best deal when you're spending abroad, but are they all the same? Which really is the best card to take on holiday with you?

We noticed in a quick calculation last week that cards branded with the Mastercard logo seemed to have a better exchange rate than those with a Visa logo. But one observation isn't enough. So, during the week we've been working on a more in-depth analysis to find out whether that's always the case.

What are specialist overseas credit cards?

A bit of background to this first. Debit and credit cards can be used wherever you see the Mastercard or Visa symbol, depending on what your card is branded. But, when you use it overseas, your card issuer has to translate your purchase into pounds sterling – the base currency of your card. There are two factors that have an effect:

-

The card issuer's exchange rate. If you look at any credit card, it'll have a Mastercard or Visa logo. This is the card issuer, and both set their own exchange rates, which is the rate your bank gets when you use a card overseas. You can check Mastercard's and Visa's here.

-

The non-sterling transaction fee. This is set by your card provider. For example, HSBC charges a 2.75% 'commission' if you use its standard debit card to spend abroad.

So, when you spend overseas, your bank or credit card provider first uses the wholesale rate set by Mastercard or Visa on the day you make the purchase to make the exchange. Then it adds its commission, typically between 2.5% and 3% (you'll see the charge broken out on your statement). You may also see other fees for cash withdrawals, and a few even charge a fee for spending.

But this isn't our focus for this article. Some specialist overseas credit cards, such as our top pick, Halifax Clarity, don't charge this fee. We know collectively these cards are the best way to spend abroad. But are all these cards equal? Does it matter which one you pick? We wanted to know, and for this, because there are no other fees, it's a straight Mastercard versus Visa comparison.

Note: we haven't included American Express in this comparison, as while a quick survey showed its rates are comparable with Mastercard's and Visa's, the cards it issues have a 2.99% non-sterling transaction fee attached.

Mastercard vs Visa – is one cheaper than the other?

Doing back-of-an-envelope calculations last week, we worked out that spending was cheapest on the specialist overseas credit cards using Mastercard as their issuer, owing to the Mastercard exchange rate being higher that day than Visa's.

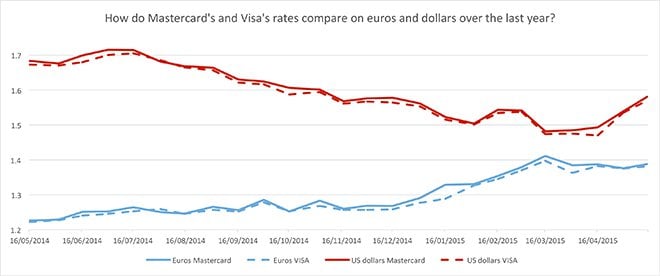

But does Mastercard always offer better rates than Visa? Is this true for the euro and US dollar only (the main currency we use for calculations), or is Mastercard better across the board?

To find out, we took the published exchange rates for Mastercard's wholesale rate and Visa's wholesale rate for euros and dollars at two different dates in each month for the last year to give us a decent number of data points to compare...

As you can see, at almost every data point, Mastercard's rates are either the same as Visa's or above. There are only a couple of points where the reverse is true. Breaking it down for euros and dollars, we had 48 different data points. Of these:

Mastercard win | Visa win | |

|---|---|---|

Euros | 22 | 2 |

US dollars | 23 | 1 |

Most of the time, the differences are small – not something you'd notice when spending $10 a time. But sometimes these differences can be quite large.

For example, in the middle of January 2015, for the euro, there was a variance of €0.04, which is a huge gap for one euro being exchanged. Scale that up and you could have got €132.88 spending £100 worth on a Mastercard, compared with €128.89 on the Visa – a big €4 difference, given the low values involved.

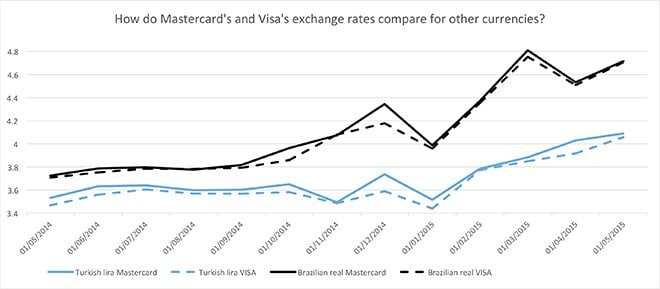

So, Mastercard wins for the main currencies, but what happens when we look at slightly lesser-used currencies?

We looked at two currencies, the Turkish lira and the Brazilian real; and the same holds true. Although we looked at only one data point per month for these currencies, we still see that the majority of the time, Mastercard holds the exchange rate crown.

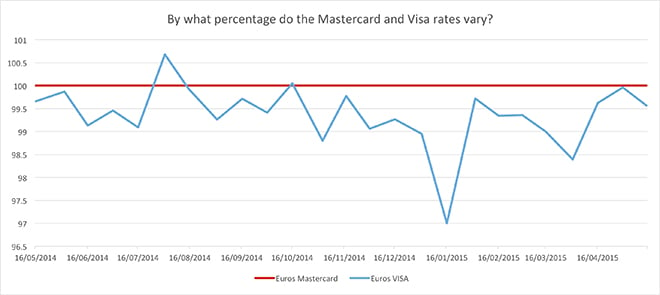

How much better is the Mastercard rate than the Visa rate?

The charts above show you that Mastercard plastic, barring a few anomalies, gives you a better rate than Visa cards for comparable spending. But, how much better is the Mastercard rate?

We've analysed the spread by 'indexing' the Mastercard rate for euros over a year (meaning it's always 100 on this graph) and then allowing the Visa euro exchange rate to vary around it.

It's close – closer than the graph makes it look, as we've given a small variance on the vertical axis to highlight the divergence. But it does show that for the points we picked, Mastercard is the winner for all but two.

On average, from the euro and dollar data sets we looked at, Mastercard's exchange rates were 0.6% higher than Visa's. While we haven't checked every day and every currency, it's likely that the data we do have shows a pattern that would be replicated.

What does this mean in practice?

In practice, it's meant that we've slightly shuffled around our recommendations of the best cards to take with you to spend abroad, ensuring that we tell you that cards using Mastercard tend to give you ever so slightly more bang for your buck.

If you don't have a specialist overseas card already, then this reshuffle might mean you pick a Mastercard. However, if you do already have an overseas card and it's a Visa and you're happy with it, then it's probably not worth changing unless you spend a lot overseas each year.

For this research, we've pointed out and emphasised the differences between the two rates. But the fact remains that an average 0.6% gap between the two exchange rates will for most, going away only once, generally amount to a euro or a dollar or two difference.

If you do want to get a new card, or change the card that you have, then our top picks – reshuffled in light of this research – can be seen in the Cheap Travel Credit Cards guide. A brief summary is here:

The top travel credit cards – all have a zero 'non-sterling transaction fee'

| Card issuer | ATM fee | Cash w/d interest (fully repaid) | |

|---|---|---|---|

| Halifax Clarity | Mastercard | None | 12.9%-21.9% |

| Aqua Reward | Mastercard | £3 or 3% | 39.9%-59.9% |

| Post Office | Mastercard | £3 or 2.5% | 27.9% |

| Aqua Advance | Mastercard | £3 or 3% | 39.9%-59.9% |

| Saga (1) | Visa | £2 or 2% | None |

| Nationwide (2) | Visa | £3 or 2.5% | 27.9% |

| Norwich & Peterborough (debit) | Visa | None | None |

| Santander Zero (3) | Mastercard | None | 27.9% |

| (1) Over 50s only – you may not be accepted if you've four or more credit/store cards. (2) For its current account customers only. (3) Not accepting new applications. £10 dormancy fee, never been charged. | |||

Are there any other differences between Mastercard and Visa cards?

In the UK, you won't really notice any difference. Your card's issued in pounds and you spend in pounds, so exchange rates don't affect you. You may find a few retailers accepting one and not the other, but this is the exception rather than the rule in this country.

However, if you use the cards on holiday, you might see more than an exchange rate difference. Both Mastercard and Visa are accepted at more than 36 million retailers worldwide. But it may be that retailers overseas accept one but not the other – it's unlikely that the cards have exactly the same coverage. Do let us know in the forum if you've found countries or cities where you couldn't use a Mastercard or Visa but the other worked.

Additional reporting by Amelia Jane Murray

Share this guide?

Latest weekly email

Latest weekly email

Clever ways to calculate your finances