Eight mortgage cost-cutting need-to-knows with interest rate rises on the cards

Mortgage rates have recently been at all-time lows – some can fix at just 0.89%. Yet that may be about to end, warns MoneySavingExpert.com founder Martin Lewis. A UK rate rise is on the cards and now may be the time to lock in cheap deals to save £1,000s. Here's our mortgage heads-up.

Update: 16 November 2021: This article was originally written by Martin and the MSE team for our weekly email on Wednesday 20 October. It has been regularly updated since then with the latest update taking place today.

Martin: "Back in April, there were no switchable mortgage deals below 1%, by June there were 10. Today there are 45 – with the cheapest fix being 0.89% (see Cheapest mortgage deals). Yet with hindsight, we may look back and say this was as good as it got.

"The signs of an interest rate rise are strong. The Bank of England's Governor recently said it 'will have to act' over rising inflation. For Andrew Bailey, that's as subtle as chucking a brick through a window, his way of telling people interest rate rises are likely coming. On the back of that, the market's strongly predicted (although it's not always right) rates will rise from today's 0.1% to 0.25% next month, then to 0.5% by February and 0.75% later next year.

"This is echoed too by the Office for Budget Responsibility, which predicted on the back of the Autumn Budget that if inflation keeps rising, then interest rates could rise strongly next year too. It also suggests mortgage rates will be boosted on the back of that.

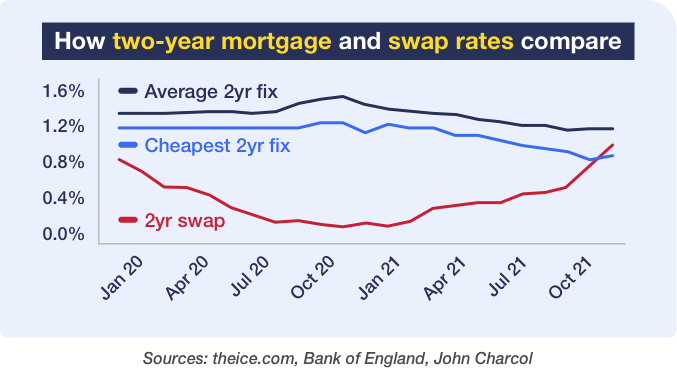

"Yet, when and how they'll rise is complex. Take a look at this graph...

"Normally the rate of the cheapest mortgage deals tends to follow similar City 'swap rates' – basically long-term interest rate predictions. Yet over the last year, unusually they've been somewhat de-linked. This is likely due to a combination of increased competition, and banks having a glut of cash due to quantitative easing (for instance, the Government sort of printing money), but that's due to end by January.

"Put this together with possible UK base rates rising and it's highly likely change is a comin' – and possible mortgage rates could go up steeply and swiftly. So EVERYONE with a mortgage should check now if your existing deal is as good as it can get – and that applies double if you're languishing on your lender's standard variable rate.

"To prove the point, Louise tweeted me:

'@MartinSLewis Our mortgage was £476 a month. We fixed for 5 years at 1.62% [and our] payments went down to £248 [saving £2,700/yr].'

"Now over to the team to talk you through the practicals of remortgaging (switching your deal without moving home)..."

1. Find your current mortgage details

Gathering the following info will make deciding a lot easier:

- What's the rate? Plus monthly payments & outstanding debt.- What type is it? Is it a fix, tracker, SVR? See fixes v variables.- When's the intro deal over? When does the 2yr fix end?- When must it all be repaid? In 10, 20, 25yrs?- Will you be penalised to switch deals? Does your fix or tracker have an early repayment charge? If so, it isn't usually worth switching, though it can be on rare occasions. See Ditch your fix?- What's the loan-to-value (LTV)? This is the proportion of the home's current value you borrow – for example, £270,000 borrowing on a home currently worth £300,000 is 90% LTV. Rates get cheaper the lower your LTV. See LTV help.

Our free PDF booklets take you through it step by step

- Our FREE 64-page Remortgage Guide 2021

- Our FREE 55-page First-Time Buyers' Guide 2021

2. Find your existing lender's cheapest rate

Contact your existing lender to check what new deal it'll offer you – this is called a 'product transfer'. It didn't used to be a great option, but these days as your existing lender is allowed to forgo affordability checks if you're not borrowing more, it may work out well for some. Plus there may be lower fees and paperwork. Don't stop here though...

3. Now speedily compare it to the market's cheapest deal to see whether big savings are possible

Spend a couple of minutes on our mortgage comparison tool to see if it's likely you can save more by going to another lender. Do note that low-rate deals can mean higher fees – so our tool factors these into the 'MSE total cost' to make comparing easier.

The biggest factor affecting your rate is your LTV. Mortgages start at 95% LTV, but you'll get a cheaper deal at 90% LTV. It's cheaper again at 80%, 75%, and then bottoms out at 60% of a home's value. There can also be minor gains at each 5% in between.

Type (1) | Intro rate + arrangement fees | Annual cost (2) |

|---|---|---|

Typical SVR | 4% | £9,500 |

0.89% + £995 | £7,277 | |

1.33% + £1,019 | £7,501 | |

1.73% + £2,019 | £8,341 | |

1.34% + £999 | £7,258 | |

2.38% + £2,019 | £8,372 | |

0.82% + £1,525 | £7,205 |

1) All links go via our Mortgage Best Buys comparison. (2) Based on monthly payment & including the fees spread across the deal (hence why a 5yr rate can look cheaper than 2yrs) on a 25yr term.

Should you fix? The more you value certainty and being able to stick to a budget, the more you should hedge for a fix, and fix longer. If you're worried about interest rates rising, which as Martin notes above is a real concern right now, then fixing is a bit like an insurance policy against this.

Trackers may be a smidgeon cheaper, and if today's rate is your prime concern and you can ride out moves, you may want to go for it. See our full fixes vs trackers analysis for more.

4. Use our range of calculators to make it easy to compare deals

To simplify the process, plug your numbers in here...

5. Sadly, it's not about what's the best mortgage, it's about what's the best mortgage you'll be accepted for

There are two key financial checks the lender will do on you when you remortgage. Unfortunately each lender is different, so there's little point trying to second-guess it all, but there are ways you can improve your prospects.

Are you creditworthy? A poor credit history can torpedo a remortgage application, or at least mean you don't qualify for the cheapest deals. So check your credit file (for free) to ensure there are no errors, then minimise other credit applications, and pay down debts if you can. See 37 tips to boost your creditworthiness.

Can you afford it? Lenders must also do strict checks to see if you can afford mortgage repayments, not just at current rates, but stress-testing how you'd cope if they rocketed. They want evidence of income, bills, expenses and sometimes even eating out.

Likely to be close to the wire? Being frugal in the months leading up to application can help. For more tips, see 18 ways to boost mortgage acceptance.

TOP TIP: Try to go £100 beyond any LTV threshold.

If you've worked hard to get enough together to reach the next LTV band, for instance, 90% or 75%, try to push to £100 beyond that. It means it no longer looks to mortgage underwriters like you're scraping to get to the limit, and can ease acceptance.

6. A good broker can be worth their weight in gold – they can match you with lenders more likely to accept you

Lenders are loosening some mortgage acceptance criteria – for example, some will now include bonuses and commission in your income assessment, which wasn't the case during the pandemic.

Yet getting the right mortgage is still complex, and even if all else looks good, acceptance is more difficult if one or more of these apply...

-

You're self-employed.

-

You claimed financial help from the state during the pandemic.

-

You've a non-standard property.

In these cases, we strongly suggest you use a mortgage broker. They will do the 'finding a deal' work for you and they have details of most lenders' acceptance criteria, which aren't easily obtainable by the public, plus many deals, even some product transfers that can only be accessed via brokers.

Nationwide 'fee-free' brokers (they earn via commission from lenders) include L&C Mortgages*, Habito and Trinity Financial* (it normally charges a fee, but not via this link), though some with more complex situations may want to pay. Full help in Top mortgage brokers.

'250,000 mortgage prisoners are trapped on often costly deals and the cladding scandal means more are likely to join them'

Martin Lewis, founder of MoneySavingExpert.com, said: "During the 2007 financial crash, the Government of the time rescued the banks. Yet many customers of firms that went under then had their mortgages sold on over the years as part of a 'debt-book' to financial companies that don't do mortgages – and they just saw it as a financial transaction.

"The nature of these mortgages meant many people couldn't get deals elsewhere, and were now stuck with rump mortgage managers who didn't have any other products. Little has been done to help them, there are still an estimated 250,000 of these mortgage prisoners who are having their finances eroded and lives destroyed because of it.

"To help, we've a new Mortgage prisoners guide, with a step-by-step list of what to try. Sadly it won't fix the issue for everyone, in fact it won't help the majority, but it is worth a go.

"This guide is part of MSE's and my personal continued campaign on this issue. Alongside it, and lobbying, I'm currently funding a second tranche of London School of Economics mortgage prisoner research to try and find solutions to put to the Government."

More mortgage prisoners due to the cladding scandal?

Martin added: "A whole new group of mortgage prisoners, mostly in leasehold flats, have now been created due to the cladding scandal.

"They are unable to get an EWS1 safety certificate needed to be able to move property or, in some cases, remortgage (do check via a broker). This is a scandal that needs fixing by Government. There is a little hope though that the recent cabinet reshuffle will see a renewed focus."

7. Still a while from your current deal ending?

Many lenders let you lock in a rate three months ahead, and a few even go to six months in advance, so it's wise to check within that window. However, locking in can incur a non-refundable booking fee of £100-£250.

If you're worried about rates rising and missing out on the cheap deals currently available, you could see this is a form of insurance policy. Bag the rate you need now, but if things get cheaper, forego it, lose the fee and go cheaper. Full info in long lock-in mortgage help.

8. Use any savings to bag a better mortgage deal

If you've savings, use them to get a cheaper mortgage. As mentioned above, rates tend to improve as you move down to 90%, 80%, 75% and 60% LTV, so when you remortgage, use savings so you need to borrow less for your mortgage. It can really pay off.

For example, if an extra £1,000 of savings got you to the 75% LTV band, the top 2yr fix here is 0.99%. This means you'd pay £560/month (on a £150,000 mortgage) as opposed to 1.33% at the 80% LTV band, which costs £590/mth.

What the * means above

If a link has an * by it, that means it is an affiliated link and therefore it helps MoneySavingExpert stay free to use, as it is tracked to us. If you go through it, it can sometimes result in a payment or benefit to the site. It's worth noting this means the third party used may be named on any credit agreements.

You shouldn't notice any difference and the link will never negatively impact the product. Plus the editorial line (the things we write) is NEVER impacted by these links. We aim to look at all available products. If it isn't possible to get an affiliate link for the top deal, it is still included in exactly the same way, just with a non-paying link. For more details, read How this site is financed.

Duplicate links of the * links above for the sake of transparency, but this version doesn't help MoneySavingExpert.com:

L&C Mortgages, Trinity Financial

MoneySupermarket.com Financial Group Limited is authorised and regulated by the Financial Conduct Authority (FRN: 303190). The registered office address of both MoneySupermarket.com Group PLC and MoneySupermarket.com Financial Group Limited (registered in England No. 3157344) is MONY House, St. David's Park, Ewloe, Chester, CH5 3UZ. MoneySavingExpert.com Limited is an appointed representative of MoneySupermarket.com Financial Group Limited.

Latest weekly email

Latest weekly email

Clever ways to calculate your finances