Pensions: one of those grown-up things everyone needs understand. If you don't, please read this...

Martin's 13 Pension Boosters: tips, tricks & must-knows to maximise private and work pension savings

Including: can you find £10,000s of lost pensions?

I had far more questions for last week's ITV Pension Special than usual, thousands upon thousands. Most from older people, but you shouldn't leave thinking about your pension till, like me, your hair's greying at the edges (though not quite as much as our design team's photoshopping >). As most people put £100s or £1,000s in

pensions each year from age 22, it's something all should understand.

I had far more questions for last week's ITV Pension Special than usual, thousands upon thousands. Most from older people, but you shouldn't leave thinking about your pension till, like me, your hair's greying at the edges (though not quite as much as our design team's photoshopping >). As most people put £100s or £1,000s in

pensions each year from age 22, it's something all should understand.

For those saying: 'Ah, just live for the now'... Remember, we typically only work 45 to 50-ish years of our 85-year lifespan and that work income needs to cover all the fallow years, meaning saving for retirement is crucial (when we're little, our parents pay for us, but most then need do the same for our kids).

I'm focusing on private & workplace pension saving, not the State Pension, which depends on how many National Insurance years you've collected (do check your State Pension). Big areas include...

- 3 pension superpowers (tax relief, employer contributions, salary sacrifice)

- Tax relief for self-employed and private pensions

- How to get totally free 1-on-1 help

- Can you find £10,000s in lost pensions?

- Where to start a pension?

- Is it worth consolidating my pensions?

- Pensions and new Inheritance Tax rules

|

The two types of private pension: which are you on?

|

|

Defined Contributions (aka Money Purchase) pensions.

All private and most workplace pensions

Often called a pension pot, this is money you build up in investments, which can't usually be taken out until you're 55 (rising to 57 in 2028). But how you take it out matters (full help on that in next week's email). The amount you have in it depends on...

- How much you and/or your employer put in.

- The growth of and income from your chosen investments

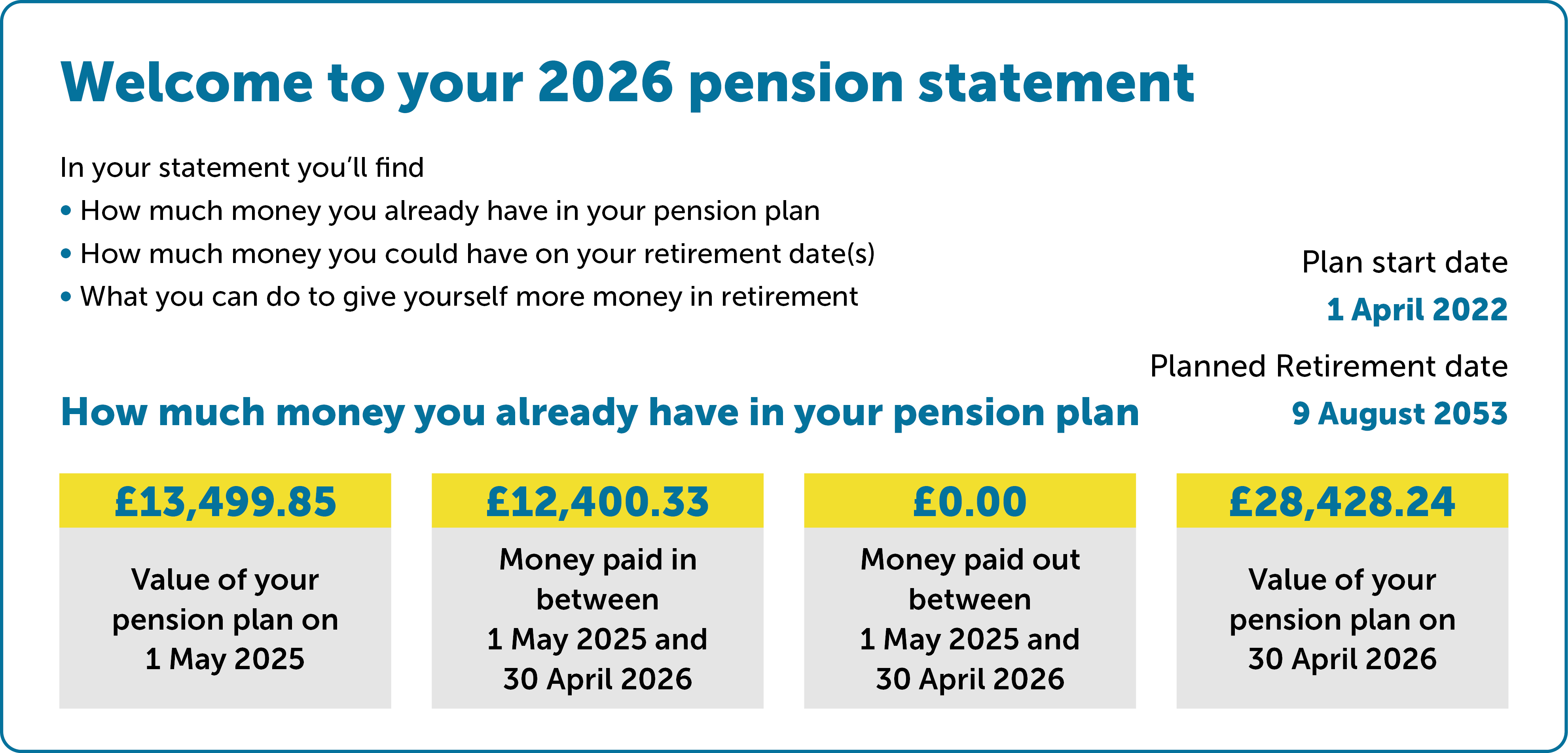

You'll know you've got one of these if, when you check your pension statement, it shows you an amount of money (like this one...).

Defined Benefits (aka Salary Scheme) pensions

Some workplace pensions

These used to be seen as the gold standard. It's where you get a set percentage of your 'final' or 'average' salary each year, eg, 1/60th. So work at a company for 20yrs and get 1/3 of your final salary (not all the tips below apply to Salary Schemes).

You'll know you've got one of these if, when you check your statement, it shows your current salary, how long you've been with the firm, and your predicted final annual income (as opposed to a total amount invested). If you're not sure, just ask the scheme.

Salary Scheme tip: Thinking of working less / going part-time in your final years at a firm? Check its terms first, as it may mean as you get a % of 'final salary', you're massively reducing your pension.

|

1. Don't accidentally leave your private or workplace pension to your ex! You can't usually leave pension savings in your will. If you die without taking it, or there's still money in your pension, the provider/trustees decide what to do with it.

Instead, when you sign up to a Money Purchase type scheme or similar you usually fill out an expression of wishes (aka a nomination form), which tells the trustees your preferences. They usually follow this but don't have too. Yet many people don't update these as life changes, so check & update your expression of wishes - it's important. I've had too many messages like this X post over the years...

"@MartinSLewis It's just happened to us! My mother-in-law died... only for her pension firm to want her ex's details... they split 20 years ago! She'd be spitting feathers if she knew!" Do check yours.

2. Deep breath... how much should you save in a pension? Here's a scary, old, famous, very rough rule of thumb for Money Purchase pensions...

Take the age when you start putting money in your pension, halve it, and that's the % of your salary to aim to put into your pension for the rest of your working life for a strong retirement income. So start at 20 and it's 10% (this includes employer's contributions); at 40 it's 20%.

Most people unfortunately won't get there. Yet the real message to take is that the earlier you start, the better, as you've longer for gains to compound. Plus my tip is: every time you get a pay rise, if possible, put a chunk of that into your pension before you get used to the increase. See our beginners' guide to pensions for more.

Pensions are an incredibly powerful investment vehicle with three superpowers. I explain them below, but you may find it easier to watch my video explainer from my ITV show last week or better the full show on ITVX.

3. Pension SuperPower I. You pay from pre-tax income, so you get more saving than it costs you. Imagine you're putting £100 into your pension pot from your salary, which is how many employees do it. Normally, for a basic 20% rate taxpayer, when they're paid that £100, they only actually receive £80 in their pocket after tax.

Yet many (not all) workplace pension contributions are made before tax is taken off, and you get the 'net pay' after (it's worth checking if you're unsure). That means you get to invest £100, but it only costs you £80 off your payslip due to the tax relief. And the gain is even bigger for those at higher levels of tax (I'll leave you to contemplate whether that's fair or not)...

With other savings, investments, or ISAs, you only contribute from what you get after tax has been taken off. That's a massive disadvantage.

See how this works for the self-employed or on NEST pensions below.

4. Pension SuperPower II. Employee? Don't throw away a hidden pay rise. If you save, your firm MUST contribute too. I was asked in the show whether someone should opt out of their workplace pension and use a private pension instead. All the specialists and I immediately said NO! While there may be a marginal improvement in the investment choice, it's likely throwing money

away as...

By law, employees aged 22 up to State Pension age, earning over £10,000/yr, are automatically enrolled into a pension (ie 'opted in' to contributing without being asked) and, crucially, if you're opted in, your employer MUST contribute too.

For a Money Purchase pension, the minimum contribution is 8% on earnings between £6,240 and £50,270, though many employers will do it for more. And of that, the employer must contribute a minimum 3% points of that (meaning you pay 4% and there's 1% tax relief), though again, some pay more.

This is a huge boon. It means it actually has to give you more money than just your salary (though, of course, your current disposable income is less due to your contribution). Per £100 in your pension, the employer adds £60, so that's £160 total going in, and with the tax relief too, this only costs you £80 as a basic rate taxpayer - meaning you get at least double invested compared to the cost to you...

Beware 'opting out' or even just dropping contributions. Opting out is usually a bad idea, as you're throwing away free cash. See my old don't give up a pay rise blog for the very few times it may be worth considering.

Even if you think 'I just want to lower my contributions' beware: lower it below the minimum 5%, then your firm doesn't need to contribute (many do, but they don't have to), so check before any action.

5. If you're offered a Salary Sacrifice pension it means you can get the National Insurance back too. Pension SuperPower III. This is only available if your employer offers a Salary Sacrifice scheme for your Money Purchase pension - they don't have to, so it's just a 'do they, don't they'.

Here, instead of you paying into your pension from your salary, your employer pays it for you and reduces your salary by that amount. So if you'd normally pay £200/mth, your salary drops by £200 and your employer puts £200 into your pension.

You still get the same result as tax relief, and the same employer contribution, so what goes in your pension is the same, but you don't pay National Insurance (NI) on the sacrificed salary (8% for basic-rate taxpayers, 2% for higher-rate). Per £100 contribution, a basic-rate taxpayer gets £160 in their pension at a cost of £80, plus their National Insurance cost is reduced by a further £8. As employers save on NI too, some pass some or all of that on to you too (some don't)...

|

Salary Sacrifice - The Kryptonite...

All superheroes can face a threat. And in the 2025 Budget, a plan was announced that from April 2029, the Salary Sacrifice Pensions gain would be weakened, so that only the first £2,000 of employee Pension saving via Salary Sacrifice will be free of employer and employee National Insurance contributions. All superheroes can face a threat. And in the 2025 Budget, a plan was announced that from April 2029, the Salary Sacrifice Pensions gain would be weakened, so that only the first £2,000 of employee Pension saving via Salary Sacrifice will be free of employer and employee National Insurance contributions.

At standard auto-enrolment levels, this means once you earn over £46,000/yr, some of your contributions will no longer get the NI boost, and if your firm gives you its NI gain, that'll drop too - which would be the biggest impact.

I've had some people ask me: 'Once this happens, does it mean work pensions are no longer worth it?'. Absolutely not! You'll still get tax relief and your employer contributions - which is all many employees get now - and it's still very lucrative. Sadly, you'll just lose some of the added National Insurance gain.

|

Salary sacrifice does actually change your salary - that's a boon and a risk. The lower salary on paper can be a boon for some:

- Student maintenance loans: If you earn below roughly £65,000 (Eng), dropping your salary could see your child getting a bigger loan.

- Child benefit: If the highest earning parent earns £60,000+ the Higher Income Child Benefit Charge means net Child Benefit is reduced; by £80,000 you don't get anything. So lowering your Salary can mean you get more.

Similar applies for those earning around £100,000 with various childcare help, and the Personal Allowance reduction.

The flip side of that is that a lower income can also have negative knock-on effects, eg, it could affect how much you could borrow for a mortgage, or it could mean you no longer earn enough to qualify for statutory maternity pay. See salary sacrifice help for more.

6. Age 16 to 21? Age 66 to 74? Or earn under £10,000?FORCE your employer to contribute to your pension. If you're in one of these groups, you are not auto-opted in to a work pension. Yet in some cases, if you choose to opt in, then you get at least an 8% contribution (of which the employer must pay a min 3%). So you can push it to give you that SuperPower too...

|

Auto-enrolment is based on age & annual earnings

|

|

Earn £6,241- £10,000 |

Earn £10,001+ |

| Age 22-66 |

Right to opt in |

Auto-opted in |

Age 16-21 & 67-74

|

Right to opt in |

So if you're young, living at home, and have a bit of spare cash, it's a great time to put money in your pension because you're employer's going to match it. Same too if you're still working after State Pension age.

7. Self-employed? Private pension? Or Nest pension? The tax relief's the same, but the process is different. Save in a private pension, which is the only choice for the self-employed, and you get the same Pension SuperPower I tax-relief as above. Though it works a different way...

- 20% tax relief is automatic. In other words, put £80 in a pension, and magically it'll show a £100 investment - without you doing anything. This continues up to the limit you can contribute. See how much can I put in my pension?

- Higher (40%) or top (45%) rate taxpayer? As well as the 20% automatic relief, you can claim the rest of the tax back from HMRC - often via your annual self-assessment tax return. It isn't added to your pension, but reduces your tax bill on other income instead, so you may want to put in more to your pension to cover the gain you've made on your Income Tax bill. See Don't miss out on £1,000s pension tax relief.

PS: There are different tax thresholds in Scotland. If you're paying over 20% tax there, you can reclaim the extra too.

To confuse things, those whose workplace pension use 'relief at source', including the huge Nest system, will only automatically get 20% tax relief when you pay into it. So again, if you are a higher or top-rate taxpayer, you will need to reclaim the rest.

8. How much can you put in your pension? And you can still gain with no income (so children can have pensions)? The most you can usually personally pay into a pension and get tax relief is limited to...

- Your annual UK earnings up to £60,000.

- This is reduced for some higher earners.

- This may also be reduced to £10,000 if, age 55+, you have accessed taxable money from your pension.

- If you've spare income and unused prior years' allowances, you may be able to

carry forward to contribute more.

Even with no income, until you're age 75, you can get tax relief, on up to £3,600 gross a year in a pension. That means you pay in £2,880 and the rest is added automatically. So children can have pensions too.

Some grandparents open them, liking the thought it'll trigger a memory of them in 50 years' time. And because the earlier you start, the longer the money has to grow, starting super young can be powerful once your ickle ones are old 'uns like me.

No surprise, over the years, more than a couple of kids of parents in MSE Towers have pensions. But I'd usually sort your own finances first, then look at

top children's savings and fill a

junior ISA, as those are shorter-term priorities. If you're lucky enough to have enough to do all that, a

pension for children can be a great addition.

9. The one thing to remember if you forget all else.

With pensions, FREE ONE-ON-ONE impartial help and guidance is available. You should use it. |

|

Unlike many other financial areas, with pensions, totally FREE guidance is available online, via chat, or on the phone, funded by a levy on the finance industry. I get great feedback on it.

- Over 50 with a Money Purchase pension? You can speak to Pension Wise. You can get a free 45min to 1hr appointment.

- Under 50? You can speak to MoneyHelper.

You find both at www.moneyhelper.org.uk or call 0800 011 3797 (opening times: Mon to Fri, 9am to 5pm).

Significant funds? Consider paying for full independent financial advice. Guidance can talk you through rules, how tax works under different options, and it's a great place for everyone to start. What it won't do is give you a personal bespoke recommendation on best products or investment choice.

For that, you need to find a financial adviser. This is usually primarily for those with, or saving enough to get, bigger pension pots - let's say around £50,000 minimum - so the gain offsets the cost. While you do pay, getting it wrong on big amounts can cost more, so it's often worth it.

|

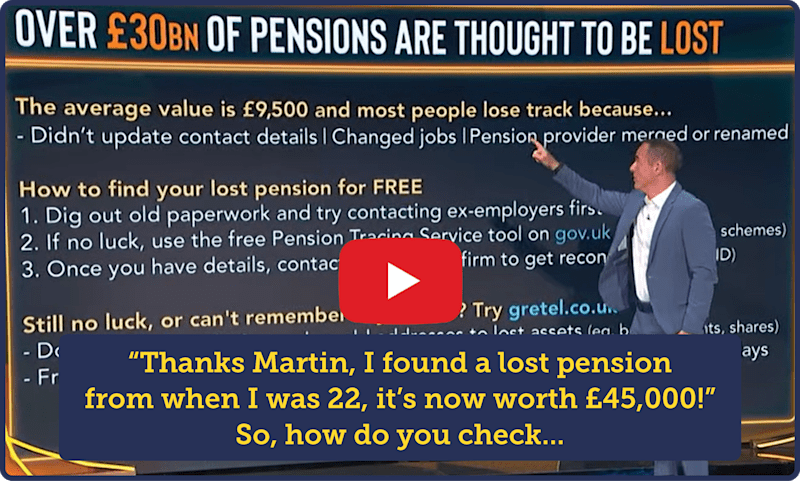

10. Can you find £10,000s lost pension? There's over £31 billion worth to be found. With people regularly moving job, and many automatically being opted into workplace pensions, it's easy to lose track. Ruth came on my show last week to say she'd found a £45,000 lost pension. So here's my one minute video explainer of how to track them down...

For more step-by-step and links to key tools go to our find lost pensions guide. As Paul emailed last week: "I started work for a company when I was 18, worked for them for 17 years. Then another company for around 23 years and forgot about the first pension as the company had long since closed down. Managed to trace who was still in control of my pension, while there was only £20,000 in the pot when I left, in the 23 years since my pension is now worth over £161,000. Glad I checked."

11. Want to start a pension? How to do it... If you're offered a workplace pension, that's usually where you start. If not (or you're at the maximum matching contributions), another pension provider may be an option for lower charges/better investment choice.

Recommending pensions is tricky for me, it's a regulated area and is about investing, so I can't give it my normal best buys treatment.

- Investment savvy and want maximum flexibility? A self-invested personal pension (SIPP) is a type of pension that works like an investment account within a pension wrapper. It's usually best for those who know what they're doing, as you choose the investments yourself.

You can typically pick from a wide range, including shares, funds, gilts, and corporate bonds from across the world. They're offered by the likes of AJ Bell*, Fidelity*, Hargreaves Lansdown*,

and Interactive Investor*.

I often hear 'pensions are useless, buy gold or property'. That misunderstands what a pension is. A pension is a tax wrapper. Within a SIPP, you can often invest in gold funds or property funds, and you still get pension tax relief on the money you pay in. So many of the investments you can buy outside a SIPP can be held inside one too. PS: See my new beginner's guide to investing for more on the basics of how it works.

- Want it simple and choices made for you? On my ITV show, financial planners Andrew Pye (Just Financial Planning) and Nick Hutchings (Rockwealth Reading Ltd) both said if you want to keep things as simple as possible, look for providers offering ready-made portfolios. Here you answer a few questions about your goals and attitude to risk, and you're matched to a portfolio that's then managed on your behalf. They highlighted..

- AJ Bell Ready-made Pension*: offers three options: 'cautious', 'pension builder', and 'adventurous'.

- Interactive Investor Managed Portfolios: you answer questions then you're matched to one of 10 managed portfolios.

- Vanguard Managed Personal Pension (SIPP): offers five risk levels from very cautious to very adventurous.

With these options, you won't need to pick individual investments. They're designed to be low-hassle, diversified, and professionally managed.

You can go a step further with robo-investment options. These are online services that ask a few questions about you, then build and manage a portfolio on your behalf, adjusting it over time.

Ultimately, what dictates your pension's growth is the investments you choose within it. When I hear someone say: 'Pensions are terrible, mine's performed badly', I'm reminded of my ancient one word that caused a pension crisis blog.

A pension isn't a product, it's a valuable tax wrapper that gives tax relief. If the investment isn't a good one, that doesn't mean pensions are bad. Yet it's worth being aware this is investing, it's volatile, things can go down as well as up – nothing is perfect. Yet on the balance of probability, a broad spread of of investments over a long period of time will hopefully see reasonable growth.

12. Should you consolidate your Pension pots? This is always one of the most-asked question when I do pension shows.

Clearly, having them all in one place eases the administrative burden, and can mean lower fees if you choose carefully which pension you're moving them all to. So it is a good aim, yet financial advisers I discuss it with raise the following things to check:

- Be very careful moving money out of Salary Schemes (if it's even possible), you could be giving up unbeatable benefits.

- Are there any perks or guarantees in your existing pension, such as guaranteed growth, annuity, or other rates, which you'd miss out if giving it up?

- Compare the charges and investment choices of your old pension(s) to the one you will consolidate them all in.

- Are there any exit penalties that apply to the schemes?

- How flexible are the options for taking retirement or death benefits?

- If you've £10,000 or less, you can use the 'small pots rule', letting you cash in up to three personal pensions once you're 55, without it impacting how much you can contribute in future. So leaving them untouched may be useful later.

- Don't close a pension your current employer is contributing to. If it's not a great scheme, you may instead be able to regularly sweep the money (known as partial transfers) into a pension you prefer.

- Alternatively, if your current employer's scheme is good, then often there's a form to move all your old ones into it.

If that's all gobbledygook to you, that's a very good reason to - as a bare minimum - get some free guidance or advice before consolidating anything, as get it wrong and it can cost you.

For more explanation, read our Should I consolidate my pension? guide. This should all get easier when the 'pensions dashboard' launches (exact date TBC, but currently looking like 2027).

13. Pensions will count towards Inheritance Tax (IHT), from April 2027. Currently, if you die with money left in a Money Purchase pension, it usually sits outside your estate, so there's no Inheritance Tax (IHT) to pay on it.

Yet from 6 April 2027, unused pension funds and many death benefits (eg, Money Purchase pensions, SIPPs & drawdown arrangements) WILL normally be included in your taxable estate. Though of course anything left to a spouse or civil partners is always IHT exempt.

Annuities or Defined Benefit pensions already paying out WON'T usually be included.

Plus, as now, whoever inherits your pension may also need to pay Income Tax when they take the money:

- Die under 75: they can usually take it free of Income Tax.

- Die 75 or over: withdrawals are taxed at their normal Income Tax rate.

So this will mean double taxation for some. Eg, die at 80 leaving a £100,000 pension above IHT threshold and the estate could pay 40% IHT (£40k). The remaining £60k, when withdrawn, may then be taxed as income for the recipient.

Yet remember, currently only 5% of estates actually pay IHT, and even with the changes it's predicted only 8% will. And there are more allowances, especially for married couples, than people think - watch my Inheritance Tax need-to-knows video for an easy explainer.

Thanks to Andrew Pye, Financial Planner from Just Financial Planning, Nick Hutchings, Chartered Financial Planner from Rockwealth Reading, Charlene Young from AJ Bell, and the Money & Pensions Service for reviewing this for me.

-------------------

Coming next week: How to take your pension... In next week's email, I'll write about how to take your pension and avoid the huge tax trap involved,. Plus more on how to do that in a way that helps mitigate the Inheritance Tax change.

Latest weekly email

Latest weekly email