The MoneySavingIdiot checked his credit score – and this is what he found

Did you miss the first two sure-to-be-award-winning MoneySavingIdiot blogs (on train delays and travelling abroad)? If so, then here's the idea. Although working at MSE means I help people save money, I suck at doing the same for myself. So I'm attempting to improve my cash-related competence and help inspire other non-natural MoneySavers. This week: credit scores.

As it happens, I signed up for MoneySavingExpert's Credit Club before I was actually an MSEer. It's a tool that lets you see your credit score for free and explains how likely you are to be accepted for credit in real life. (There are several other sites out there which let you check your credit score, including Clearscore and Noddle – see our our How to check your credit report guide for full info.)

I joined Credit Club because my personal finances had been somewhat mismanaged over the previous couple of years (for reasons I hope to cover in a later instalment).

In true MoneySavingIdiot-style however, I wasn't overly keen on learning the unvarnished truth about my financial state. So, after briefly logging in, I clicked away quicker than you can say "definitely not too big to fail". Now I'm on the road to monetary recovery, I decided it was time to open a beer, steel myself and rejoin. This is what I found...

1) My credit score wasn't quite the disaster I was anticipating

Your credit score is basically a rating of your credit history. Lenders don't see the actual score, but they use what's on your file to get an idea of what your future financial behaviour will be like, based on what you've done before. Given not so long ago I went the best part of a year without even looking at a credit card bill, let alone ensuring I was paying them, I was anticipating apocalypse.

Turned out that was a little over-dramatic. I mean, if the credit score spectrum was the Premier League, my credit score wouldn't be Manchester City, or even Arsenal. But considering I was expecting a horror show and ended up in the middle of the pack, things could have been worse – let's call it Newcastle United.

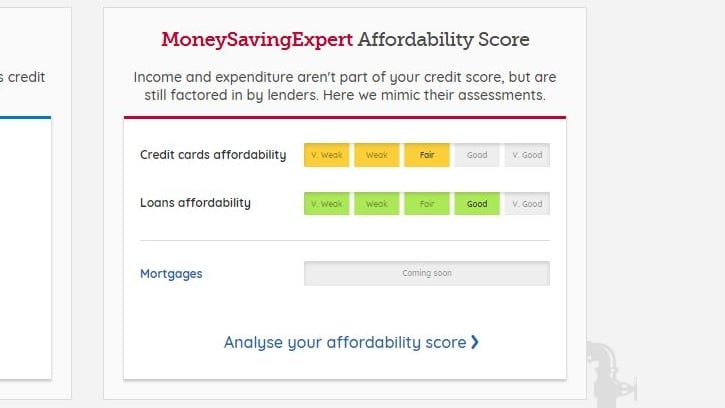

2) Lenders also look at what you earn and what you spend

It turns out that how much you earn and how much you spend doesn't actually influence your credit score, which seems a bit odd (although as I said above, lenders don't actually see your score). Yet what you earn and what you spend IS still taken into account by lenders, and has a big say in whether you're offered credit cards, loans etc, which makes sense.

Credit Club replicates that, so you can see what they think you'll be able to afford to pay back. As you can see, my credit card affordability tallies up with my credit score, but my loans affordability ain't too shabby. (Though that means I now have to resist the urge to borrow three grand to convert the garden shed into a pub. Swings and roundabouts.)

3) My credit hit rate is pretty pony – but that doesn't mean I'm up the spout when it comes to getting cards and loans

As I (we?) have already discovered, it's your credit history plus what you earn and spend that dictates what lenders will offer you. Credit Club uses these to generate your Credit Hit Rate, which shows you how many top cards or loans you're likely to be accepted for. And as you can see from the very red dial on the left, I've only got a decent shot at getting 30% of them...

...yet it's not all bad news. The bit on right shows I've still a good chance of getting several different types of credit card, and those I'm most likely to get aren't quite the dregs you might expect. For example, when I clicked through I found I've a 95% chance of landing a balance transfer card that offers up to 20 months at 0% with no fee (the current longest 0% card without a fee is 22 months).

On the flip side, if I did borrow £3,000 for my shed-pub and paid it back over three years, the only loan firm very likely to accept my application would charge me 9.9% APR, meaning I'd pay over £450 in interest, whereas if my hit rate were high enough for me to get the current cheapest loan for £3,000-£4,999, I'd pay around £300.

4) I can improve my credit profile by laying off applying for credit

The '8 things you need to know about your credit profile...' section of the Credit Club dashboard breaks down what's good and bad about it using happy and not-so-happy faces – a format so simple even a MoneySavingIdiot can understand it.

For perhaps the first time in my life, I got more happy than not-so-happy faces. But it's the not-so-happys that indicate what you can do to improve your profile, so let's look at them:

Taking them in reverse order...

-

Residential status. I'm a lodger and the chances of that changing anytime soon are slim to infinite nothingness, given that I'm as likely to be Adele's next beau as I am to become a homeowner. (Totes up for being a house husband if you're reading though, Ms Adkins.)

-

Account stability. Also a tricky one – given I'm a lodger I don't have utilities under my name, and the lot of the lodger/renter is moving relatively regularly, meaning even if I did have such accounts under my name, keeping them 'stable' for over six years is unlikely.

-

Credit applications. I can definitely reduce these. I've blasted through a few in the last six months as I've been shifting existing credit card debt to 0% interest cards (another topic I hope to cover in future), so it should be simple to lay off now and see what effect that has.

5) It wasn't quite as horrendous as I was expecting – give it a whirl

If you've made it this far, I'm sure by now you've got a good idea of what I was expecting to find when I rejoined Credit Club – a well-done slab of financial Armageddon with a generous side of Things I Don't Understand.

But it genuinely wasn't as spirit-shattering as I expected (no little victory), my credit options aren't quite as non-existent as I thought they would be, and it wasn't the incomprehensible brain-numbing torture garden I feared.

So if like me you're something of a formless entity when it comes to money matters but you fancy giving it a try, you can join Credit Club in minutes with just a few details. Bon chance.

For full info on this sort of thing from non-MoneySavingIdiots, see our guides on Credit Scores, Building Your Credit History and How To Check Your Credit Report.

Share this guide?

Latest weekly email

Latest weekly email