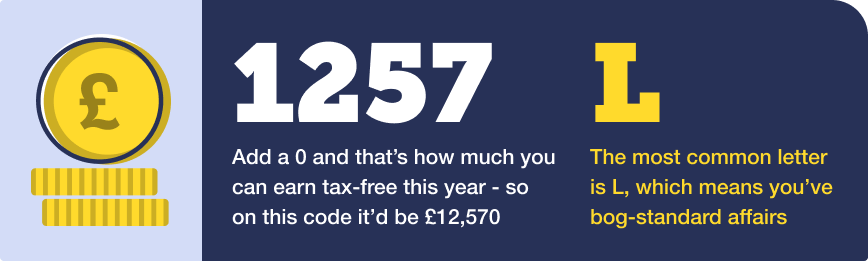

MoneySavingExpert's Money Tips Email

|

|||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

DON'T believe the fake 'Martin Lewis' or 'MSE' ads |

|

|

|

|

|---|

|

The Car Insurance Phoenix: After 2yrs of falls, sadly prices may rise again, so... Car insurance price changes can dictate the right tactics for getting the best deal at speed. And things may be about to shift. After three years of heavy rises (up 68%), we've seen average costs drop over the last couple of years - down 9% in the past year alone (source: MoneySupermarket). Yet now analyst Defaqto says we're starting to see average prices creep up again, driven by rising inflation due to the Middle East conflict. So... With average prices still down on a year ago, if you've not claimed or had an incident, aim for a price at least 10% less than last year.

|

|

A YEAR'S 2for1 at 360+ UK gardens (eg, Leeds Castle, Haddon Hall, many National Trust) in £10 mag. Always popular - just one visit often more than saves the cover price. Gardeners' World Are solar panels worth it? We've crunched the latest numbers to see how the maths stack up. If they're right for you, we've a way to get £550 off if you request a quote before 14 April. Solar panels Get £25 Amazon voucher just for opening (not switching to) a new bank account. New & existing Santander customers who open a new current account via the links below and spend five times on the debit card within 30 days will be emailed a link to claim a £25 Amazon voucher from 10 July 2026 (if not, check your spam). Full info's in our Santander review, but we'd focus on these accounts... The Everyday* is its bog-standard fee-free account, so your best bet if you just want to grab the voucher. The Edge* account costs £3/mth but pays 1% cashback (max £10/mth) on household bills paid by Direct Debit (or look at the Edge Up* if you've bigger bills, as it pays a max £15/mth cashback on bills for a £5/mth fee). Did you miss? Car finance mass redress scheme CONFIRMED - are you due a typical £830 back? A reminder of Martin's hugely popular car finance briefing on how you can get redress quicker, easier and with more certainty. Sticking on the energy Price Cap? Save £120+/yr with BOOSTED tracker tariffs. There are two decent deals for those who aren't looking to fix right now (most cheap fixes have been pulled in recent weeks due to the Middle East conflict). Both have small £25/fuel early exit penalties, so it's cheap to leave if fixes do return... Better for higher users: E.on Next's Pledge tariff now discounts Price Cap unit rates by £50/fuel (was £25), so you get £100/yr off the Price Cap, plus via our link in Cheap Energy Club we've £40 boosted dual-fuel cashback (£20 elec-only). Better for lower users & Smart Prepay: EDF's Simply Tracker reduces Standing Charges by £25/fuel, so you get £50/yr off the Price Cap - plus, till Thu, we've £70 boosted dual-fuel cashback (£35 elec-only; no cashback if you're on Prepay, but this is still cheaper than staying on the Cap) via our Cheap Energy Club. FREE Ideal Home Show tickets (norm £15) including a chance to see Martin live. From this weekend until 19 April at London Olympia. 10,000 available. Full info in Free Ideal Home Show tickets. Ends Thu. 150Mb Sky broadband '£20/mth'. Switchers in 70% of UK homes can get this 150Mb Sky fibre & line deal for £23/mth, plus you'll be emailed an £80 prepaid Mastercard or shopping voucher within 4mths (check your spam folder). Factor that in and it's equivalent to £19.67/mth over the 2yr contract. Want other options? Use our full broadband comparison. 50% off Gousto recipe boxes code, eg, five meals for two £23. MSE Blagged. 5,000 available, for new users. 50% off your first month, 25% off your second. Gousto. News. Student loan interest rates capped at 6% for Plan 2 & postgrad loans. See Student loan interest cap. Teacher? Get 35% off Ocado, 20% off Disney+, 10% off Morrisons & more. See 40+ teacher discounts. 'I'm saving a huge £850/yr just by switching Sims.' Success of the Week. MoneySaver Janet emailed: "I was paying £79/mth to EE on mobile Sims for myself and two grown-up grandchildren (it was their birthday gift). Last month I followed your mobile cost-cutting tips and switched to Lebara. I now pay £8/mth for all three [a saving of £852/yr]. Plus, with EE there was no free roaming. My grandson's in the army, so we avoided calls while he was overseas. But now I can contact him in Europe free. Many thanks. What a huge saving." If we've helped you save (on this or anything else), please tell us about it. |

|

|

|---|

|

This is all about one credit card, the American Express (Amex) Preferred Rewards Gold (links via our eligibility calc so you can check acceptance odds and apply if they're good). It's done a big temporary boost to its newbie bonus, which means play your card right and you can now grab £500+ worth of freebies at no cost. Not everyone can take advantage though - if you've had a personal Amex card within the past two years, you won't get the bonus. Here's how the offers stack up...

|

|

Ends Thu. Free £50 Amazon voucher just for signing up to a credit card (you can then cancel). Accepted newbies opening the fee-free Amazon Barclaycard credit card before 11.59pm on Thu get a £40 Amazon voucher, then another £10 voucher for activating the card in the app. So that's a quick £50 with no spend whatsoever - after that, you could just cancel. It does give a decent 1yr 0.5% cashback on most spending (1% at Amazon), though that's beatable by the top cashback cards. If you do use it, ensure you pay off IN FULL each month, preferably by Direct Debit, otherwise the interest dwarfs the cashback. Will it impact my credit score? One application may have a short-term minor impact. It's not usually an issue, but best avoided if you've a key credit application (eg, a mortgage) coming up. A month's 'tailored' dog food £3.80 (normally £38) via 90% off code. MSE Blagged. A fraction of what most pay for off-the-shelf tins in a supermarket. You can cancel after the month if you want. Newbies only. Bone appétit Eurostar £70 returns flash sale? This time last year, for three days only, it offered cheap Apr-Jul fares, and we strongly suspect it'll do so again soon - possibly even by the time you read this... Keep your eyes peeled on Eurostar deals. Easter holidays kids' freebies: Museums, farms & activities. See free/cheap ways to entertain kids. New. Track deals from your favourite retailers in the MSE App. Get alerts when we spot new deals from the places you love to shop. We've squished several bugs too - update or download for free on iOS | Android. |

Tell your friends about usThey can get this email free every week

|

|

AT A GLANCE BEST BUYS

|

|

MONEY MORAL DILEMMA Should I bail out my son who wants nothing to do with me? My adult son lives in the USA and took out student loans in 2016, which my American friend agreed to co-sign for. She recently contacted me to say she is being chased for a payment of $27,000 [£20,000], or they'll deduct $1,100 [£800] every month from her pension. My son's nowhere to be found, has no assets, no job and refuses to speak to us. It's not fair to let my friend suffer this stress, but I resent my son for hiding from his debts. Enter the Money Moral Maze: Should I bail out my son who wants nothing to do with me? | Suggest a Money Moral Dilemma (MMD) | View past MMDs |

|

|

MARTIN'S APPEARANCES (WED 8 APR ONWARDS) Tue 14 Apr - This Morning, ITV1, 10.20am |

Important. Please read how MoneySavingExpert.com worksWe think it's important you understand the strengths and limitations of this email and the site. We're a journalistic website, and aim to provide the best MoneySaving guides, tips, tools and techniques - but can't promise to be perfect, so do note you use the information at your own risk and we can't accept liability if things go wrong. What you need to know This info does not constitute financial advice, always do your own research on top to ensure it's right for your specific circumstances - and remember we focus on rates not service. We don't as a general policy investigate the solvency of companies mentioned, how likely they are to go bust, but there is a risk any company can struggle and it's rarely made public until it's too late (see the Section 75 guide for protection tips). We often link to other websites, but can't be responsible for their content. Always remember anyone can post on the MSE forums, so it can be very different from our opinion. Please read the Full Terms & Conditions, Privacy Policy, How This Site is Financed and Editorial Code. Martin Lewis is a registered trade mark belonging to Martin S Lewis. More about MoneySavingExpert and Martin LewisWhat is MoneySavingExpert.com? Who is Martin Lewis? What do the links with an * mean?Any links with an * by them are affiliated, which means get a product via this link and a contribution may be made to MoneySavingExpert.com, which helps it stay free to use. You shouldn't notice any difference; the links don't impact the products at all and the editorial line (the things we write) isn't changed due to them. If it isn't possible to get an affiliate link for the best product, it's still included in the same way. More info: See How This Site is Financed. As we believe transparency is important, we're including the following 'un-affiliated' web-addresses for content too: Unaffiliated web-addresses for links in this email trading212.com, chase.co.uk, saga.co.uk, vidabank.co.uk, investengine.com, admiral.com, lv.com, diamond.co.uk, elephant.co.uk, axa.co.uk, santander.co.uk Financial Conduct Authority (FCA) Note MONY Group Financial Limited is authorised and regulated by the Financial Conduct Authority (FCA FRN: 303190). MoneySavingExpert.com Ltd is a company registered in England and Wales. Company Registration Number: 8021764. Registered office: One Dean Street, London, W1D 3RB. MoneySavingExpert.com Limited is an appointed representative of MONY Group Financial Limited. To change your email or stop receiving the weekly tips (unsubscribe): Go to: www.moneysavingexpert.com/tips. |

Latest weekly email

Latest weekly email

Clever ways to calculate your finances