Archive: MoneySavingExpert's Money Tips Email

|

|

|---|

|

DON'T believe the fake ads on Facebook |

|

|

|

|

|---|

|

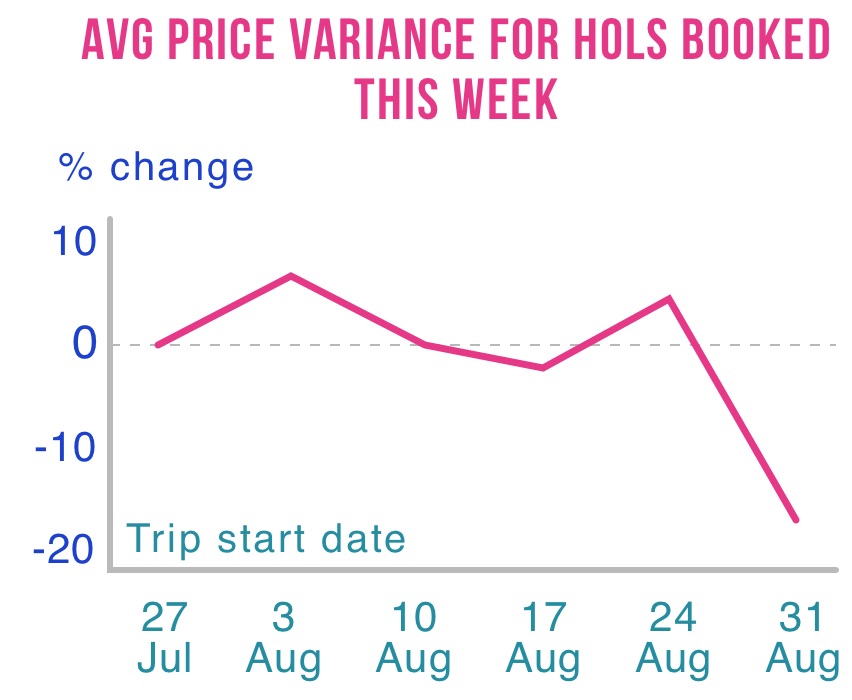

It's the summer holiday 'lates' period - now's the time to grab cheap getaways if you're flexible, eg, 7nts' self-catering in Malaga, £174pp

|

|

Ends Thu. Cheapest MEGA-fast broadband & line of 2019 - 100+Mb for '£18.75/mth' from Virgin. This 12mth deal for newbies is only avail via this Virgin Media link. Yet only 50% of the UK can get it - check your eligibility via the link. For more options see our Broadband Unbundled tool. Make 'em PAY YOU to show your boarding pass at airport shops. Martin's video explainer was hugely popular last week, despite being low down in that email. So to ensure you don't miss it we're putting it higher up this week - can you make 'em pay you to show it? 16 Center Parcs tricks, incl half-price Euro stays & how to bag an 'extra day' free. Whether you've booked, or plan to, we've these tips and more in 16 Center Parcs Tricks. Are you due an Ikea voucher, eg, £5 off £40? See this and 20+ Ikea hacks. Average equity-release rates lowest in a decade. Read Martin's 5-min 'Should you do it?' guide. Equity release is a way for over-55s to spend their home's value without selling up. And now, average rates are below 5% for the first time in at least 10yrs. That doesn't mean it's right for everyone, but it does mean it's a good time to read Martin's Equity Release guide. How to bag £35 of FREE drinks, incl 5 pints, G&Ts, cocktails & J2O. Claim free booze, soft drinks, tea and coffee via apps and sign-ups. Free drinks (pls be Drinkaware). |

|

|

|---|

|

Tesco cuts loan rates to join the cheapest at 2.9% There's big competition among a string of lenders right now. Usually just a couple fight to be cheapest but now Tesco Bank has dropped rates and there are five at the top of the best-buy tables for larger amounts - with their rates close to all-time lows. Intuitively, with more choice, you've more chance of being accepted, so long as you've a decent credit score and income, though that's impossible to validate. Use our Loans Eligibility Calculator to home in on the ones you're most likely to be accepted for, without damaging your credit score.

|

|

If an energy cold-caller says they're from MoneySavingExpert (or Martin) BEWARE. We've had a spate of reports from people telling us that cold-callers have been claiming to be from MSE. We NEVER cold-call. See cold-call warning. Driving to Europe this summer? Check if you need an emissions sticker to avoid a £60+ fine. Plus which docs you need, breakdown cover help and more. Driving in Europe Stay cool for less: 5 top tips to beat the heat & save cash - £1 sun cream, factors 15-50... or simply turn bottles around Earn a boosted £20 in M&S/Amazon vouchers doing quick online surveys. MSE Blagged. Popular site pays you to fill in surveys and do online searches. We've a link that gets newbies a £15 bonus when you net £5 worth of its points, which you can swap for vouchers - previous deals only gave a max £10 bonus. Swagbucks. £25 Ciaté lip gloss set (norm £75ish). MSE Blagged. Six full-size lip glosses with holographic/glitter effects. 2,000 avail. Ciaté PS: We're delighted to tell you that our Coupon Kid Jordon is back at MSE Towers fit, healthy and raring to save you a bucket-load of cash after a long-running battle with Crohn's disease - see his blog: Jordon 2 Crohn's 0 - the Coupon Kid is back. |

Tell your friends about usThey can get this email free every week

|

|

AT A GLANCE BEST BUYS

|

|

Cheap over-65s' travel insurance from £50/yr: solving an age-old problem The prohibitive insurance quotes some older travellers receive can leave many angrily overpaying, and others sadly stuck at home when they dreamed of heading off to party. Last week we looked at cheap cover for those with pre-existing conditions, previously we've done straight cheap travel insurance - this week we're focusing on age-based policies. Increased age does statistically mean increased risk, so you'll pay more than younger folk, but there are ways to cut costs. Full info in our Cheap Over-65s' Travel Insurance guide - here's a quick trip through the key info. (And of course, if you're travelling in the EU ensure you have a free EHIC that's still in date.)

|

|

Lego sets 20-30% off, incl Harry Potter & Star Wars. Lego discounts are rare, though stock and choice is limited this time - so hurry if you're interested. Lego deals HUGE £7,000 COUNCIL TAX REBANDING SUCCESS OF THE WEEK: |

|

THIS WEEK'S POLL What should be means-tested? Free bus passes, the NHS, student loans? Which allowances and entitlements do you think should be means-tested based on your income/wealth (in other words, the richest don't get it or they get less)? And which should everyone get regardless? What should be means-tested? Younger MoneySavers are more likely to keep quiet about being scammed. Last week we asked if you've been scammed and if so, whether or not you told anyone. Thankfully the majority of the more than 2,000 MoneySavers who responded haven't been scammed. Of those who have, 17% of those aged under 40 didn't tell anyone about it, compared with 13% of those aged 40-60 and 9% of those aged 60+. See full poll results. |

|

MONEY MORAL DILEMMA Should I tell my employer my annual leave wasn't deducted? I completed my employer's annual leave request form to take six days off and took the leave, but those days haven't been taken off my entitlement. Do I tell my employer or say nothing and keep the extra leave? Enter the Money Moral Maze: Should I tell my employer my annual leave wasn't deducted? | Suggest an MMD | View past MMDs THE QUICKIES - Debt-Free Wannabe chat of the week: Stopping spending |

|

|

MARTIN'S APPEARANCES (WED 24 JUL ONWARDS) Thu 25 Jul - Good Morning Britain, ITV, 7.35am MSE TEAM APPEARANCES (SUBJECTS TBC) Fri 26 Jul - Good Morning with Joe Lemer, BBC South West stations, from 5am |

|

QUESTION OF THE WEEK Q: Can I switch bank account if I use the overdraft facility every month? Shirley, via email.

If you're overdrawn when you switch and the new bank accepts you but won't match your existing overdraft limit, it's worth bearing in mind you'll have to repay what you owe to your old bank - so weigh that up before switching. For more help and the best banks to switch to, see Best Bank Accounts. Please suggest a question of the week (we can't reply to individual emails). |

|

TO RECLINE OR NOT TO RECLINE? That's it for this week, but before we go... many are jetting off on holiday in the next few weeks, but one question has prompted massive debate among MoneySavers - is it bad plane etiquette to recline your seat? One spoke for many, arguing that reclining is "selfish and shows no consideration for others". Another was unapologetic: "My money, my seat. Once the meals are finished my seat will be going back." Or is it, as one traveller argued, "bad etiquette to design and build the seats so close together"? Let us know where you sit on the subject in our Recline your seat? Facebook post. We hope you save some money, |

Important. Please read how MoneySavingExpert.com worksWe think it's important you understand the strengths and limitations of this email and the site. We're a journalistic website, and aim to provide the best MoneySaving guides, tips, tools and techniques - but can't promise to be perfect, so do note you use the information at your own risk and we can't accept liability if things go wrong. What you need to know This info does not constitute financial advice, always do your own research on top to ensure it's right for your specific circumstances - and remember we focus on rates not service. We don't as a general policy investigate the solvency of companies mentioned, how likely they are to go bust, but there is a risk any company can struggle and it's rarely made public until it's too late (see the Section 75 guide for protection tips). We often link to other websites, but can't be responsible for their content. Always remember anyone can post on the MSE forums, so it can be very different from our opinion. Please read the Full Terms & Conditions, Privacy Policy, How This Site is Financed and Editorial Code. Martin Lewis is a registered trade mark belonging to Martin S Lewis. More about MoneySavingExpert and Martin LewisWhat is MoneySavingExpert.com? Who is Martin Lewis? What do the links with an * mean?Any links with an * by them are affiliated, which means get a product via this link and a contribution may be made to MoneySavingExpert.com, which helps it stay free to use. You shouldn't notice any difference; the links don't impact the products at all and the editorial line (the things we write) isn't changed due to them. If it isn't possible to get an affiliate link for the best product, it's still included in the same way. More info: See How This Site is Financed. As we believe transparency is important, we're including the following 'un-affiliated' web-addresses for content too: Unaffiliated web-addresses for links in this email aquacard.co.uk, trivago.co.uk, kayak.co.uk, travelsupermarket.com, skyscanner.net, momondo.co.uk, tripadvisor.co.uk. admiral.com, johnlewisfinance.com, bank.marksandspencer.com, tescobank.com, zopa.com, sainsburysbank.co.uk,, ybonline.co.uk, cbonline.co.uk, paybyfinance.co.uk, ikano.co.uk, virginmoney.com, moneysupermarket.com, confused.com, comparethemarket.com, gocompare.com, aviva.co.uk, directline.com, leisureguardtravelinsurance.com, ageco.co.uk, nationwide.co.uk, Financial Conduct Authority (FCA) Note MoneySupermarket.com Financial Group Limited is authorised and regulated by the Financial Conduct Authority (FRN: 303190). MoneySavingExpert.com Ltd is a company registered in England and Wales. Company Registration Number: 8021764. Registered office: One Dean Street, London, W1D 3RB. MoneySavingExpert.com Limited is an appointed representative of MoneySupermarket.com Financial Group Limited. To change your email or stop receiving the weekly tips (unsubscribe): Go to: www.moneysavingexpert.com/tips. |

Latest weekly email

Latest weekly email

Clever ways to calculate your finances